Tax Loss Harvesting for US Stocks

Most investors focus on earning higher returns. However, after-tax returns matter just as much for long-term wealth creation.

Every profitable investment creates a tax liability. Over time, taxes can reduce the wealth you actually keep.

Fortunately, investors can legally reduce their tax burden through better tax planning. One widely used strategy is Tax Loss Harvesting.

Tax Loss Harvesting allows investors to use investment losses to reduce taxable capital gains. The goal is not to avoid taxes. Instead, it helps improve after-tax returns.

The strategy is especially useful for investors owning US stocks and ETFs. It becomes even more important when combined with the Wash Sale Rule, one of the most misunderstood tax rules.

This article explains how Tax Loss Harvesting works, when investors use it, and how the Wash Sale Rule affects tax planning. We'll also discuss why Indian investors currently enjoy greater flexibility than US taxpayers.

Understanding How US Stocks Are Taxed in India

Before discussing Tax Loss Harvesting, it's important to understand how US stock investments are taxed in India.

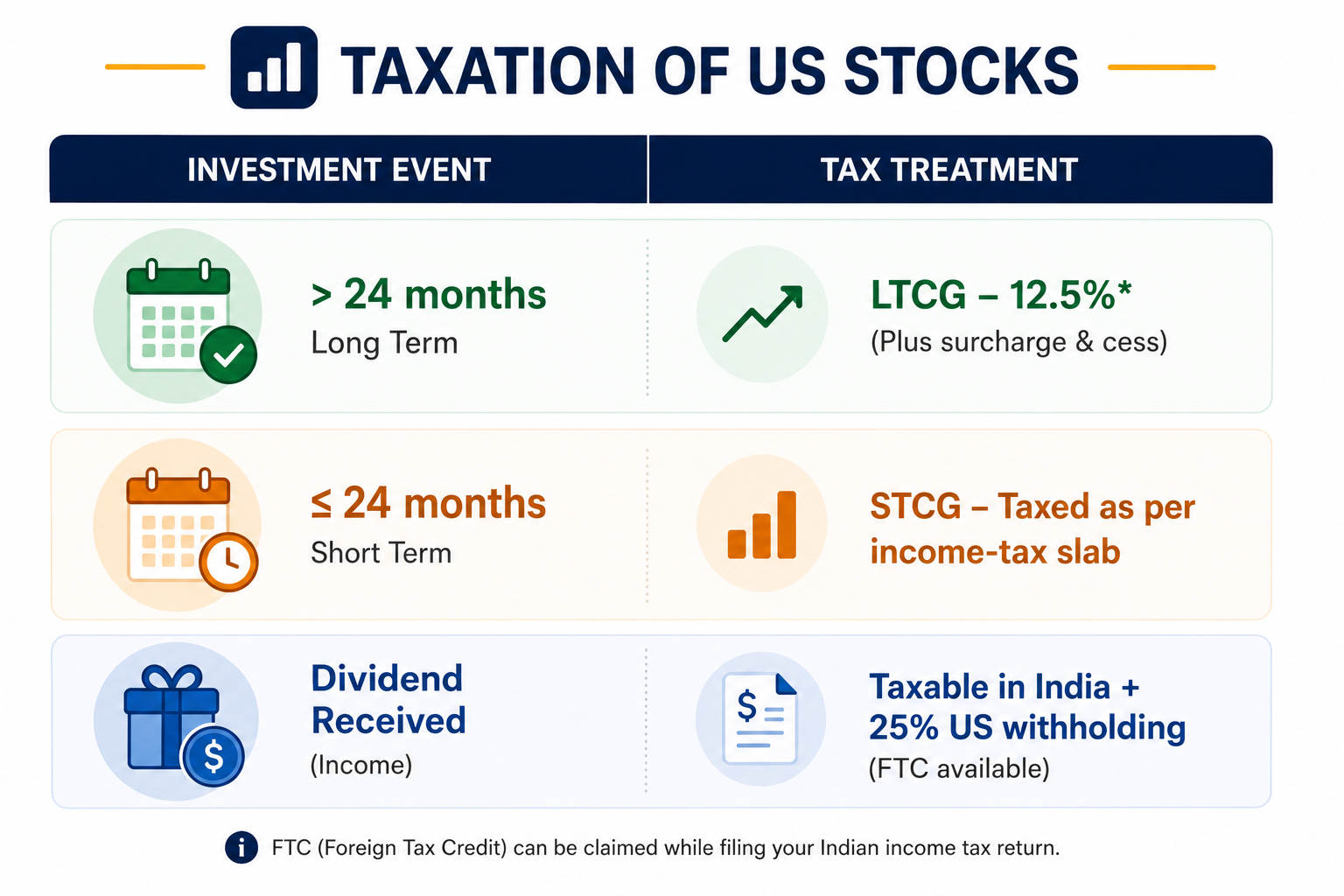

When you sell a US stock or ETF, any profit is treated as a capital gain. The tax depends mainly on your holding period.

Long-Term Capital Gains (LTCG)

If you hold a US stock or ETF for more than 24 months, the profit is generally treated as a Long-Term Capital Gain (LTCG).

These gains are currently taxed at 12.5%, plus applicable surcharge and cess.

Short-Term Capital Gains (STCG)

If you sell the investment within 24 months, the profit is generally treated as a Short-Term Capital Gain (STCG).

These gains are added to your taxable income. They are then taxed according to your applicable income-tax slab.

Dividend Taxation

Dividends from US companies are also taxable in India.

The United States generally withholds 25% tax before paying the dividend.

However, Indian investors can usually claim a Foreign Tax Credit (FTC) for this tax. To claim the credit, investors must file Form 67 with their income tax return.

Tax Loss Harvesting applies only to capital gains, not dividend income. Understanding both rules helps investors manage their overall tax liability.

What is Tax Loss Harvesting?

Tax Loss Harvesting is a legal strategy that uses investment losses to reduce taxable capital gains.

Here's how it works.

Suppose one investment has generated a profit. Another investment is trading at a loss.

By selling the loss-making investment, you realize a capital loss. That loss can then offset eligible capital gains.

As a result, tax is calculated on a lower net gain.

Tax Loss Harvesting does not increase your investment returns. Instead, it improves your after-tax returns.

Another important point is that only realized losses qualify.

A stock showing a paper loss provides no tax benefit. The loss becomes eligible only after you sell the investment.

Example -

Without Tax Loss Harvesting:

Total Capital Gain = ₹10,00,000

Tax is calculated on the full ₹10,00,000.

Now suppose you sell Tesla and realize the ₹3,00,000 loss.

Your taxable gain becomes:

₹10,00,000 − ₹3,00,000 = ₹7,00,000

Instead of paying tax on ₹10,00,000, you now pay tax on ₹7,00,000.

Your portfolio return remains the same. However, your taxable gain falls because the realized loss offsets part of your profit.

This is the core idea behind Tax Loss Harvesting.

Why Tax Loss Harvesting Matters?

Markets move in cycles. Even strong portfolios experience temporary declines.

Many investors simply wait for prices to recover. However, those losses can also reduce future tax liability.

Instead of ignoring loss-making investments, investors can use them to offset eligible capital gains.

This turns market volatility into a tax-planning opportunity.

Over time, lower taxes can improve your overall after-tax returns.

That doesn't mean investors should sell every stock trading at a loss.

Investment decisions should always support your long-term goals.

Tax Loss Harvesting simply helps you use losses more efficiently when selling already makes investment sense.

To understand the concept of taxation on US stocks and ETFs in detail, watch our youtube video below.

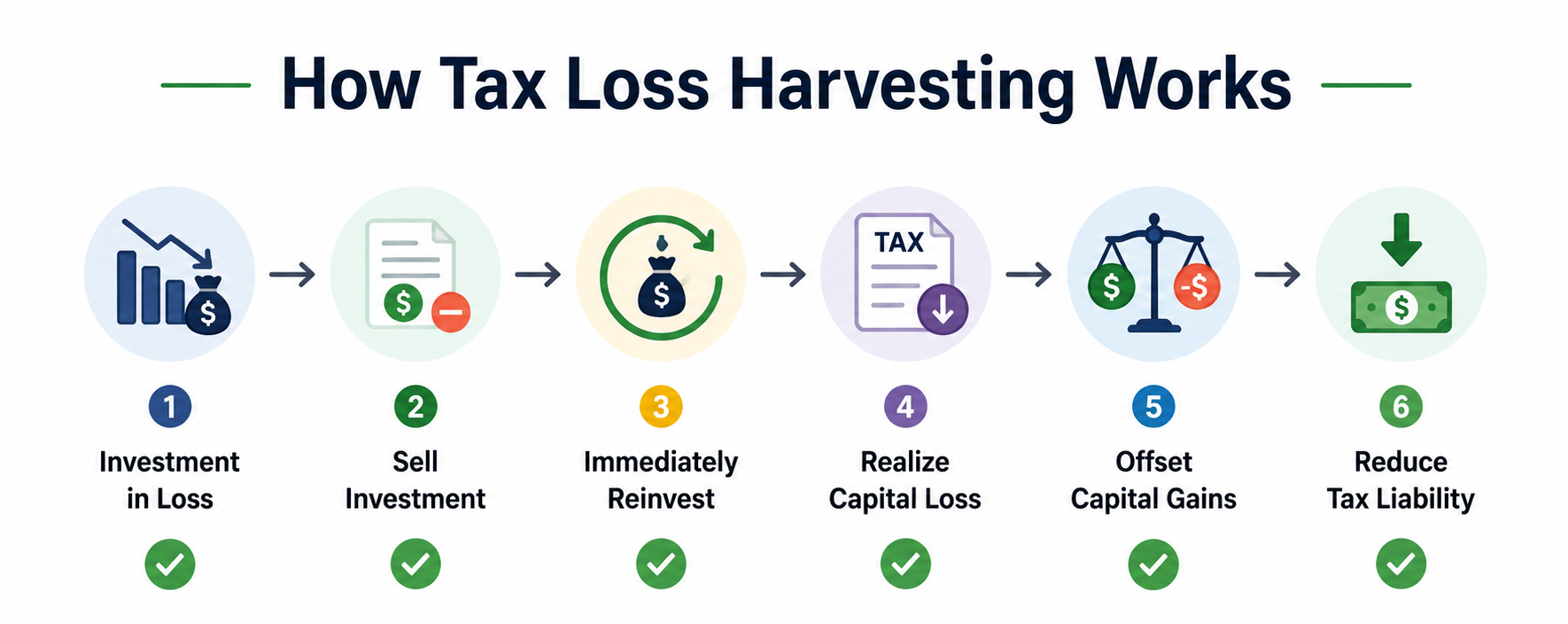

How Tax Loss Harvesting Works?

Tax Loss Harvesting follows a simple process. However, timing is important.

The strategy begins by identifying investments trading below your purchase price.

You then sell the investment and realize the capital loss.

That realized loss can offset eligible capital gains earned during the year.

If the loss exceeds your gains, the unused portion may be carried forward, subject to Indian tax rules.

Some investors also choose to reinvest the sale proceeds. This helps them stay invested while completing the tax strategy.

The exact reinvestment approach depends on the applicable tax rules.

Understanding the Wash Sale Rule

The Wash Sale Rule is one of the most important concepts in Tax Loss Harvesting.

Many investors assume they can sell a stock, book the loss, and buy it back immediately.

For US taxpayers, it usually doesn't work that way.

The US introduced the Wash Sale Rule to prevent artificial tax losses.

Without this rule, investors could create tax deductions without changing their investment position.

For example, imagine an investor owns Apple shares that have fallen in value.

The investor sells the shares and realizes a capital loss.

A few minutes later, the investor buys the same Apple shares again.

Economically, nothing has changed.

The investor still owns Apple.

Without the Wash Sale Rule, the investor could still claim the tax loss.

The US tax system generally prevents this.

What is the Wash Sale Rule?

The Wash Sale Rule applies when an investor buys the same or a substantially identical security within a 61-day window.

This window includes:

- 30 days before the sale

- The day of the sale

- 30 days after the sale

If this happens, the realized loss is generally disallowed for current tax purposes.

The loss is not permanently lost.

Instead, it is added to the purchase cost of the newly acquired shares.

This means the tax benefit is deferred until those shares are eventually sold.

Why Indian Investors Currently Have Greater Flexibility?

This is where Indian investors currently have an important advantage.

Unlike the US, India does not currently have an equivalent Wash Sale Rule for capital gains.

In practical terms, this means an Indian tax resident can generally:

- Sell a loss-making US stock and realize the capital loss.

- Use that loss to offset eligible capital gains, subject to applicable tax rules.

- Buy back the same stock immediately if they still believe in its long-term prospects.

As a result, investors can potentially reduce their tax liability without significantly changing their investment portfolio.

By contrast, US taxpayers are subject to the Wash Sale Rule. If they sell a stock at a loss and repurchase the same or a substantially identical security within the 61-day wash sale window (30 days before the sale, the day of the sale, and 30 days after the sale), the loss is generally disallowed for current tax purposes.

For Indian investors, this provides greater flexibility in managing taxes. They can harvest losses during market declines while continuing to maintain exposure to companies they believe in for the long term.

However, tax laws can change over time, and investors should always consider the latest regulations and consult a qualified tax professional before implementing any tax-loss harvesting strategy.

Best Practices for Tax Loss Harvesting

Tax Loss Harvesting can improve after-tax returns. However, it works best when combined with a disciplined investment strategy.

1. Focus on Your Investment Strategy First

Taxes should never be the primary reason to buy or sell an investment.

Review whether the investment still fits your long-term goals before realizing a loss.

2. Understand the Wash Sale Rule

If you're a US taxpayer, avoid repurchasing the same or substantially identical security within the 61-day window.

Indian investors currently do not have an equivalent Wash Sale Rule. However, tax laws can change over time.

3. Harvest Losses Throughout the Year

Many investors wait until year-end. However, market volatility can create tax-loss opportunities throughout the year.

Regular portfolio reviews may help identify these opportunities earlier.

4. Know How Capital Losses Can Be Used

Short-Term Capital Losses (STCL) can generally offset both short-term and long-term capital gains.

Long-Term Capital Losses (LTCL) can generally offset only long-term capital gains.

Unused eligible losses may be carried forward for up to 8 assessment years, subject to Indian tax rules.

5. Maintain Proper Records

Keep records of purchase prices, sale prices, brokerage statements, and realized gains or losses.

Good documentation makes tax filing easier and supports your calculations if required.

6. Seek Professional Advice

International taxation can be complex, especially when investing across multiple countries.

If you're unsure about the tax treatment, consult a qualified tax advisor before implementing any strategy.

Conclusion

Tax Loss Harvesting is one of the simplest ways to improve after-tax investment returns. It allows investors to use realized losses more efficiently while staying focused on long-term wealth creation.

For Indian investors in US stocks, understanding the broader tax framework is equally important. Holding periods, capital gains rules, and carry-forward provisions all influence the strategy's effectiveness.

The Wash Sale Rule is another key consideration. While it restricts US taxpayers from immediately claiming certain losses, Indian tax residents currently do not have an equivalent rule. This generally provides greater flexibility when harvesting losses, subject to applicable Indian tax laws.

Ultimately, Tax Loss Harvesting should support—not drive—your investment decisions. A strong portfolio, combined with disciplined tax planning, can help you keep more of your investment returns over the long run.