Diffusion Engineers: Forward PE Analysis and Growth Drivers Explained

Over the past five years, Diffusion Engineers has quietly delivered impressive financial growth.

Its revenue has grown at an annual rate of around 20–30%, while profits have compounded at nearly 30–40%. Despite this consistent growth, the stock currently trades at a P/E of around 30x, making it an interesting company to analyze.

However, evaluating a company solely based on its current P/E often provides only part of the picture.

A business is ultimately valued not just for what it has earned in the past, but for what it is capable of earning in the future. As companies expand capacity, launch new products, enter new markets, or improve profitability, their earnings can change significantly over time.

This is why investors often shift their focus from historical performance to future earnings potential.

For companies entering a new phase of growth, understanding future earnings becomes just as important as analyzing current financials.

Before evaluating whether Diffusion Engineers can sustain its growth trajectory, it's important to understand one of the most widely used valuation metrics for growth companies—the Forward P/E Ratio.

What is Forward P/E?

The Forward Price-to-Earnings (Forward P/E) Ratio measures a company's current stock price relative to the earnings it is expected to generate over the future.

Unlike the Trailing P/E, which uses earnings from the previous year, the Forward P/E focuses on future profitability.

In simple terms:

- Trailing P/E asks: How much are investors paying for the company's past earnings?

- Forward P/E asks: How much are investors paying for the company's expected future earnings?

For mature businesses with stable earnings, the difference between the two ratios may be relatively small.

However, for fast-growing companies, the difference can be significant. If earnings grow rapidly over the coming years, the valuation based on future profits can look very different from one based solely on historical earnings.

That's why investors often rely on the Forward P/E when evaluating companies with strong growth prospects.

In this article, we'll examine Diffusion Engineers' forward-looking P/E, analyze its key growth drivers, and assess whether the company's future earnings trajectory has the potential to support the market's expectations.

Forward P/E analysis

At first, we need to took the current P/E ratio which is 29.7 rounding off to 30.

Secondly, we need to take the current revenue and EBITDA numbers which are:

- Revenue - 407 Cr

- EBITDA - 57 Cr

Now, we will be try to analyse that at what rate could these numbers grow in the future and after 1 year with this growth, what should be the P/E ratio if the CMP did not increases.

Through this exercise we could analyse what could be the future valuation of the company and according to that future valuation is the current market price undervalued, justified or overvalued.

Now, what could be the revenue and EBITDA after 1 year in FY27 could be found in the company's May 2026 conferences call, where management for FY27 explicitly says that "“We expect revenue to grow by more than 20%” but for the same year does not gives any EBITDA margin or growth numbers. So for the same we are going to assume that in FY27 the EBITDA margin would be the average of last 5 years.

Now we get the numbers for our FPE FY27 calculation:

- Revenue: 488 Cr (Management mentions it'll grow more than 20% in FY27 but to be on a conservative side we took 20% as growth rate)

- EBITDA: 61 Cr (We assumed EBITDA margin to be average of last 5 years which comes to 12.6% rounding off to 12.5%)

Other Assumptions for FY27 :

- Current Interest and depreciation is 9 Cr we assume it to be same.

- Current other normal income is 17.59 Cr

- Tax rate is 25%.

Calculations for FY27:

1) Net Profit

- Net Profit = EBITDA - Interest and depreciation Expense - Tax (25%)

- Net Profit = 61 - 9 - Tax (25%)

- Net Profit = 39 Cr

2) EPS

- EPS = Net Profit/Number of equity shares

- EPS = 39/3.74

- EPS = 10.4

3) FPE

- FPE = Current Market Price/EPS

- FPE = 403/10.4

- FPE = 38.75

Conclusion of FPE analysis

- Current PE = 30

- FPE = 38.75

- Current PE < FPE

In context of 1 year from now i.e. Fy2027, Diffusion Energies is currently overvalued because the PE ratio of the company is going to be more than it is today if the current market price remains the same, which makes this stock a bit overvalued currently.

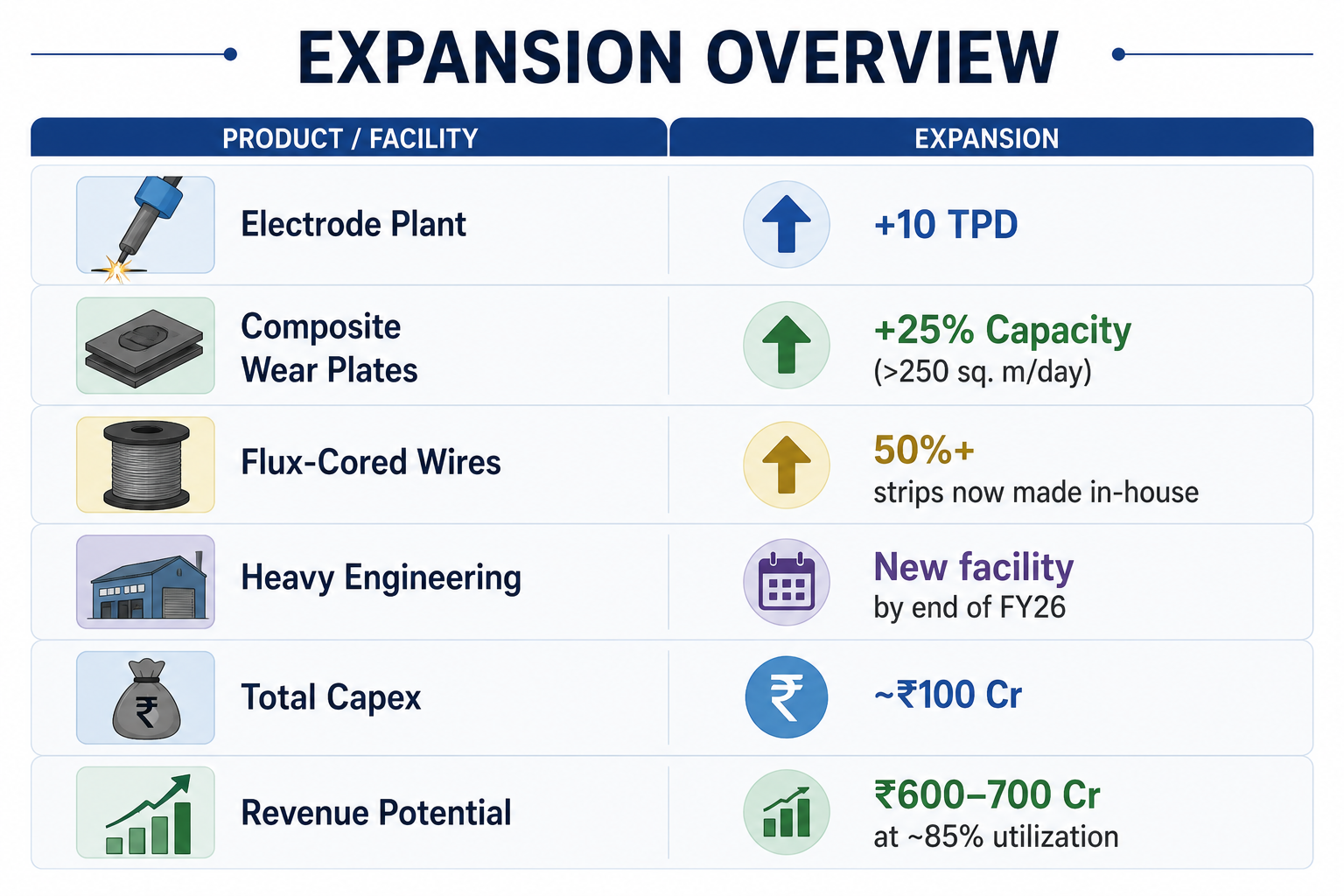

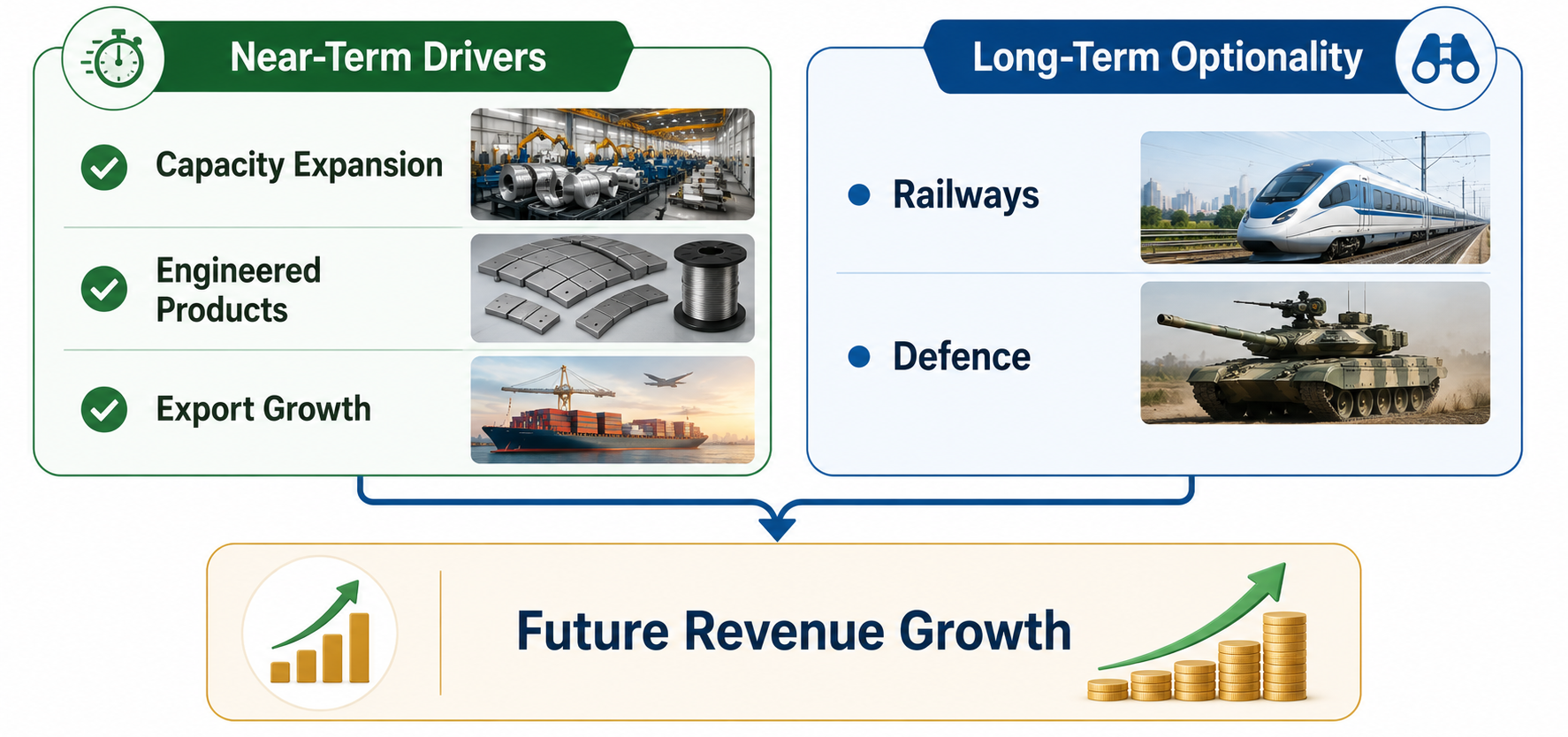

Growth Driver #1: Capacity Expansion

One of the biggest growth drivers for Diffusion Engineers is its ongoing capacity expansion.

Over the past few quarters, management has repeatedly stated that several of its manufacturing facilities were operating at around 80–85% utilization. This meant the company was gradually running out of room to execute additional orders, making fresh capacity expansion essential for sustaining growth.

To address this, the company has undertaken an IPO-funded capex programme of around ₹100 crore, aimed at expanding capacity across multiple product categories rather than a single plant.

Some of these projects have already been completed.

The company has commissioned a new electrode plant, adding 10 tonnes per day of electrode manufacturing capacity. It has also expanded its composite wear plate capacity by around 25%, taking total production capacity to more than 250 square metres per day.

Another important milestone is the commissioning of a strip-slitting line, which allows the company to manufacture steel strips used in flux-cored welding wires. According to management, more than 50% of these strips are now produced in-house, reducing dependence on external suppliers. The company also plans to increase this share further over time.

According to the company, the current capex has the potential to support asset turns of 3.0–3.5x, translating into an annual revenue potential of around ₹600–700 crore once the new capacities reach 85% utilization. However, management expects this ramp-up to happen gradually over FY28–FY29, rather than immediately after commissioning.

Going forward, investors should closely monitor how quickly these new facilities ramp up. Higher capacity alone does not guarantee growth, but successful utilization could become one of the biggest drivers of Diffusion Engineers' future revenue and earnings.

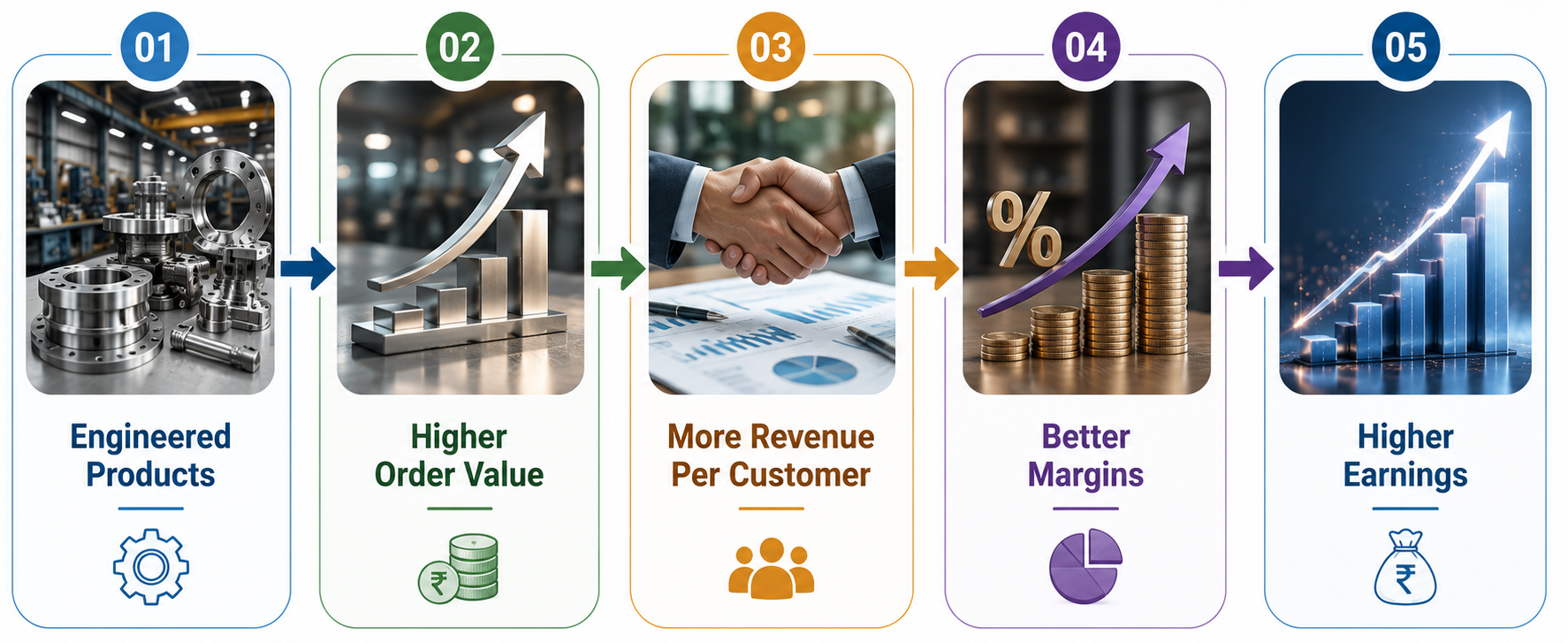

Growth Driver #2: Shift Towards Higher-Value Engineered Products

Capacity expansion is only one part of the growth story.

The second driver is the company's changing product mix.

Over the years, Diffusion Engineers has gradually moved beyond selling only welding consumables. Today, it is increasingly focusing on high-value engineered products such as composite wear plates, ready-to-fit wear parts, and heavy engineering equipment.

This shift is important because engineered products typically generate higher order values than standalone consumables.

Instead of supplying a welding electrode or a flux-cored wire, the company can now supply an entire wear-resistant component that is ready to be installed. This not only increases the value of each order but also makes Diffusion a more strategic partner for its customers.

Management also highlighted that demand for these engineered products continues to remain strong. The company's order book of around ₹200 crore is supported by healthy demand from sectors such as cement, steel, power, mining, and infrastructure, with particularly strong traction in wear plates, engineered wear parts, and specialized welding consumables.

Another encouraging sign is the company's customer base.

According to management, more than 80% of the company's revenue comes from repeat customers. This indicates that customers are not only satisfied with the products but are also returning with larger and more complex engineering requirements.

As the contribution from engineered products increases, Diffusion Engineers could benefit from larger orders, stronger customer relationships, and better profitability, making this an important driver of future earnings growth.

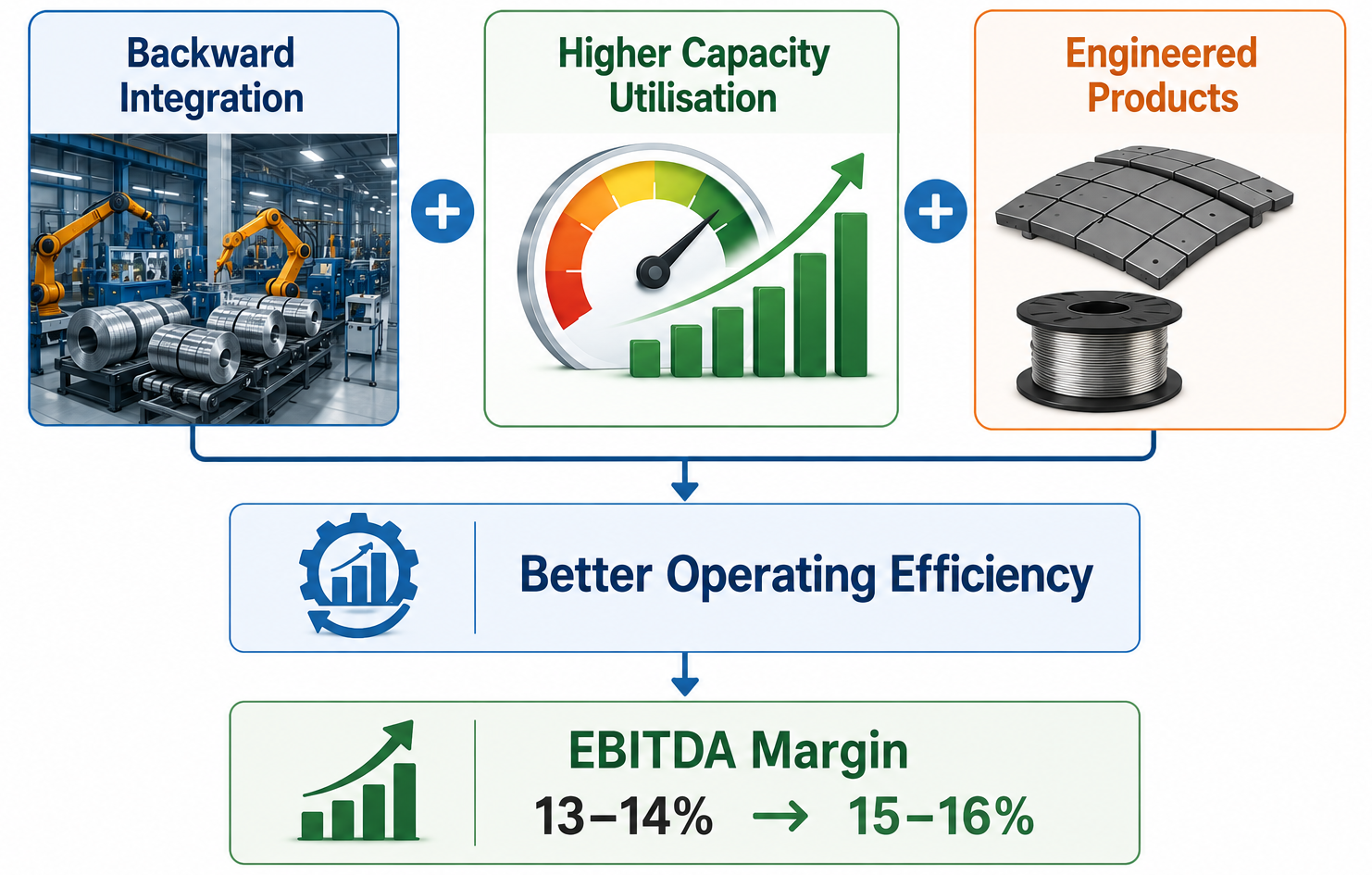

Growth Driver #3: Backward Integration Could Improve Margins

Growing revenue is important.

But growing profits at a faster pace is even more important.

This is where Diffusion Engineers' backward integration strategy comes into play.

One of the key raw materials used in manufacturing flux-cored welding wires is steel strips. Earlier, the company depended largely on external suppliers for these strips.

To reduce this dependence, Diffusion Engineers has installed a new strip-slitting line, allowing it to manufacture these strips in-house.

According to management, more than 50% of the strips are now produced internally, and the company plans to increase this share further by adding more equipment in the future.

This offers several advantages.

Producing strips in-house gives the company better control over quality and production schedules. It also reduces dependence on external vendors and lowers procurement costs over time.

More importantly, it helps protect margins during periods of raw material volatility.

Management highlighted that metals such as tungsten, molybdenum, nickel, and cobalt have witnessed sharp price fluctuations in recent years. Since there is usually a time lag before higher raw material costs can be passed on to customers, margins can temporarily come under pressure. By increasing in-house manufacturing and diversifying suppliers, the company aims to reduce this impact.

As these initiatives scale up alongside higher production volumes, management expects profitability to improve.

The company has guided for an EBITDA margin of around 15–16% over the medium term, supported by backward integration, operating leverage, and a richer product mix.

While this strategy may not immediately boost revenue, it has the potential to improve earnings by making the business more efficient and resilient.

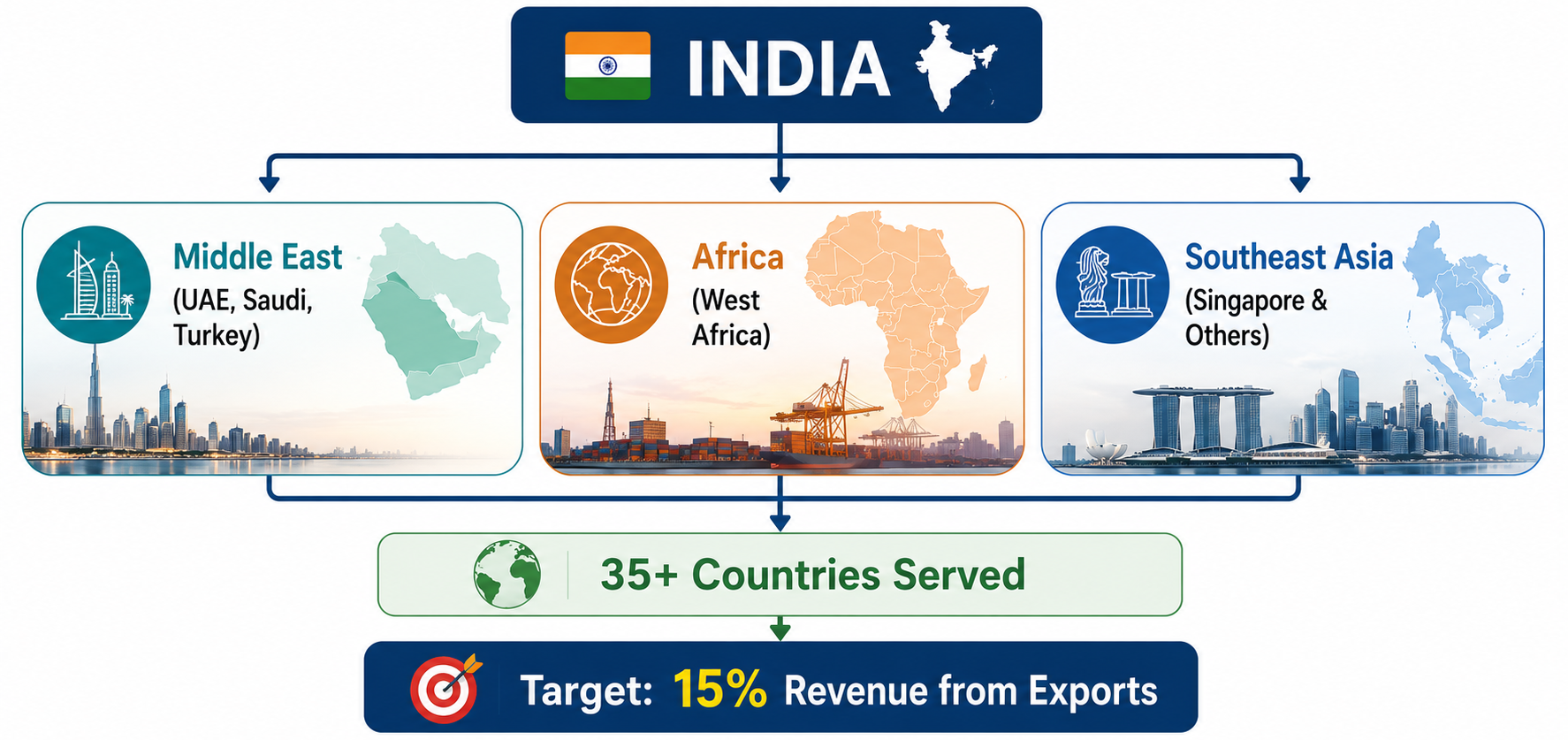

Growth Driver #4: Export Expansion Opens Up a Larger Market

India remains Diffusion Engineers' largest market.

However, the company is steadily increasing its presence overseas.

Today, Diffusion Engineers exports its products to more than 35 countries across the Middle East, Africa, and Southeast Asia. Management believes exports can become a much larger contributor to the business over the next few years.

To support this strategy, the company has established a service centre in the UAE. This facility allows Diffusion Engineers to provide faster deliveries and better after-sales support to customers across the Middle East.

At the same time, the company is actively expanding its presence in markets such as Saudi Arabia, Turkey, West Africa, and Singapore, where demand for industrial maintenance and wear-resistant solutions continues to grow.

Management has also outlined a clear target.

The company aims to increase exports to around 15% of its total revenue over the next two years. Achieving this would diversify its revenue base and reduce its dependence on the domestic market.

Another advantage of exports is access to a much larger customer base.

Many of the industries served by Diffusion Engineers—such as cement, steel, mining, and power—operate globally. As the company expands its international footprint, it gains opportunities to win repeat orders from multinational customers and participate in larger industrial projects.

If the company executes its export strategy successfully, overseas markets could become an important contributor to its long-term revenue growth.

Growth Driver #5: Railways and Defence Could Become Long-Term Growth Opportunities

Apart from its core industrial business, Diffusion Engineers is also exploring new growth opportunities in Railways and Defence.

While these segments are not expected to contribute meaningfully in the near term, they could become important growth drivers over the long run.

Railways

The company has been actively participating in railway tenders.

According to management, Diffusion Engineers participated in six railway contracts and emerged among the top two bidders in all of them. It has already received Letters of Intent (LOIs) for three projects.

The next step is obtaining final approvals.

RITES has already completed a capacity and capability assessment of the company's manufacturing facilities. Once the approval process is completed, the company expects the respective railway divisions to issue final purchase orders.

Management also clarified that these are currently developmental orders.

The immediate financial impact is likely to be limited. However, successful execution could help the company qualify for larger railway contracts in the future.

Defence

The company has also taken its first major step into the defence sector.

Diffusion Engineers recently acquired a 10% strategic stake in Tejorup Sunmay Systems Pvt. Ltd., a company developing Very Short Range Air Defence Systems (VSHORADS) under the Government's Make-II programme.

This investment is more than just a financial investment.

Management stated that its objective is to secure manufacturing rights if the prototype is successfully approved. In that case, Diffusion Engineers could manufacture key components of the missile system, including the launcher, while leveraging its existing fabrication and engineering capabilities.

However, investors should also note that this opportunity is still at the prototype stage.

Commercial production will depend on successful prototype development, regulatory approvals, and future defence orders. As a result, management does not expect this business to contribute meaningfully in the near term.

For now, Railways and Defence should be viewed as long-term optionality rather than immediate earnings drivers. If these initiatives scale successfully, they could open up entirely new revenue streams over the coming years.

Key Risks Investors Should Watch

Diffusion Engineers has outlined multiple growth initiatives for the coming years. However, the success of these plans will depend on execution. Investors should keep an eye on a few key risks that could impact the company's future earnings.

1. Delay in Capacity Ramp-Up

The company has invested heavily in expanding its manufacturing capacity. While several facilities have already been commissioned, the real challenge lies in ramping up production and achieving higher capacity utilization.

Management expects the new capacities to reach 80–85% utilization over the next 24–36 months. Any delay in order inflows or slower utilization could postpone the expected revenue and earnings growth.

2. Raw Material Price Volatility

Diffusion Engineers uses specialty metals such as tungsten, molybdenum, nickel, and cobalt to manufacture its products.

Management highlighted that prices of some of these metals have increased sharply in recent years. Since the company cannot immediately pass on higher input costs to customers, sudden price spikes can temporarily impact profitability.

3. Execution in New Business Segments

Railways and Defence offer attractive long-term opportunities.

However, both businesses are still at an early stage.

Railway projects are currently developmental orders, while the defence opportunity depends on successful prototype approvals and future commercial orders. Any delays in these processes could push revenue contributions further into the future.

4. Dependence on Industrial Capex

A significant portion of Diffusion Engineers' business comes from industries such as cement, steel, power, mining, and infrastructure.

Any slowdown in capital expenditure or maintenance spending across these sectors could affect order inflows and reduce demand for the company's products and services.

Conclusion

Diffusion Engineers has laid out a clear roadmap for future growth. Capacity expansion, a gradual shift towards higher-value engineered products, backward integration, export expansion, and new opportunities in railways and defence could all contribute to higher revenue and earnings over the coming years.

However, future growth will ultimately depend on execution. The company must successfully ramp up its new capacities, improve capacity utilization, expand its export business, and convert emerging opportunities into meaningful revenue. Investors should also keep a close watch on raw material prices and the pace at which these growth initiatives translate into earnings.

Based on our Forward P/E analysis, the stock appears fully valued to slightly overvalued over the next one year, as a large part of the near-term earnings growth seems to be reflected in the current market price.

However, the long-term picture could be different.

If Diffusion Engineers executes its expansion plans successfully, achieves its revenue targets, and sustains healthy profit growth over the next few years, the company's earnings could grow significantly. In that scenario, today's valuation may look very different from a longer-term perspective.

Ultimately, the investment thesis will depend less on the company's current valuation and more on whether management can consistently deliver on its growth roadmap. For investors, tracking capacity utilization, revenue growth, EBITDA margins, export contribution, and the progress of new business initiatives will be far more important than focusing on the current P/E alone.