Why HSBC Cut Target Price of Jubilant FoodWorks?

If you have been tracking Jubilant FoodWorks for a while, HSBC’s recent target price cut probably came as a surprise. After all, Domino’s has remained one of the strongest food brands in India for years.

So what exactly changed? Is this just a temporary slowdown, or is the market starting to worry about deeper issues in the QSR industry? Let’s break down why HSBC Holdings turned cautious on the stock and what investors should actually focus on now.

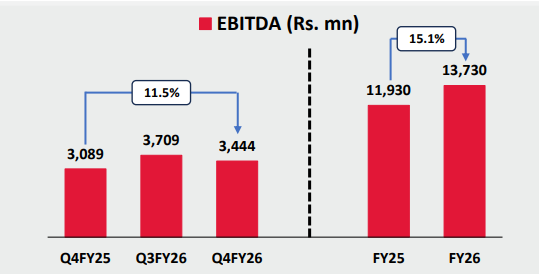

Jubilant Food In Q4 FY26

For the March quarter, Jubilant Foodworks reported revenue growth of 6.4%, while EBITDA increased by 11.5% from last year. Margins expanded by 94 basis points as well.

The company's delivery channel revenue increased by 10.3% from last year, with the delivery mix at 76.1% of the overall business.

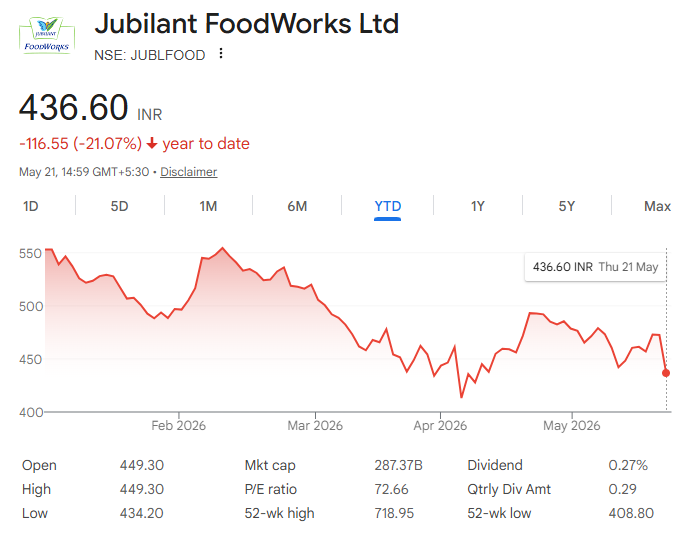

Shares of Jubilant Foodworks are trading 6.6% lower on Thursday at ₹436.60. The stock is now down 21.07% so far in 2026.

What Exactly Happened?

HSBC Holdings cut its target price on Jubilant FoodWorks after the company reported weaker-than-expected performance in its latest quarter.

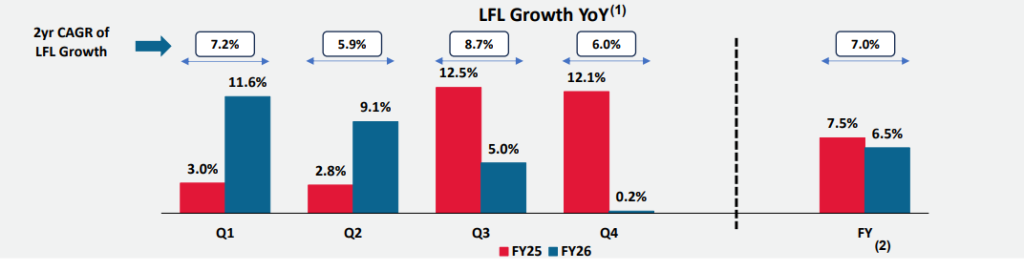

While consolidated revenue grew around 19% YoY, the core Domino’s India business remained sluggish. The biggest concern was same-store sales growth (SSSG), which came in at just around 0.2%, showing almost flat growth in existing stores.

For a stock that trades at premium valuations, even small slowdowns can hurt investor sentiment.

What Disappointed the Market?

The biggest concern was the company’s same-store sales growth (SSSG), which remained almost flat.

This means existing Domino’s stores are not generating significantly higher sales despite store expansion and promotional offers.

For a company like Jubilant FoodWorks, investors expect strong growth not only from opening new stores but also from higher demand at existing outlets.

(1) LFL ADS/Mature Store ADS: Defined as average daily sales for non-split(mature) restaurants opened before previous financial year(computed on 1,638 stores) LFL: Defined as YoY growth in revenue for non-split(mature) restaurants opened before previous financial year

(2) Full year LFL growth is simple average of LFL growth of the four quarters during the year

(3) Restaurant margin is post direct marketing expense and aggregator commission (4) Adjusted EBITDA margin is Pre-Ind AS 116 EBITDA margins

Why Same-Store Sales Matter?

In QSR businesses, same-store sales are considered one of the most important indicators of real demand.

Opening new outlets can increase revenue, but flat same-store growth signals:

- Weak customer spending

- Slower order growth

- Pressure on discretionary consumption

This is one of the key reasons why brokerages like HSBC became cautious.

Why Brokerages Cut Target Prices?

Brokerages cut target prices when they expect lower future earnings or slower growth, since valuations depend on future performance, not past results.

If growth slows or margins come under pressure, analysts reduce earnings estimates and the target price falls.

Premium Valuation Became a Problem

Jubilant FoodWorks has historically traded at premium valuations because investors viewed it as a long-term consumption growth story.

However, premium stocks usually react sharply even to small disappointments.

The target price cut is more about lower growth expectations rather than the company becoming fundamentally weak.

A strong brand alone is not enough if earnings growth starts slowing down.

Is India’s QSR Boom Slowing?

The issue may not be limited to Jubilant FoodWorks alone.

India’s QSR industry is facing:

- More price-sensitive consumers

- Rising competition from local food brands

- Pressure from food delivery platforms

- Slower urban demand

Consumers are becoming more selective with spending, especially in discretionary categories like ordering food online.

Increasing Competition

Earlier, Domino’s enjoyed a very strong position in India’s pizza market.

But now competition is increasing from local pizza chains, cloud kitchens, quick commerce platforms and international QSR brands.

Consumer preferences are also changing, with people increasingly looking for variety and value-for-money options.

Can Popeyes Become the Next Growth Engine?

Jubilant FoodWorks is also focusing on expanding Popeyes in India.

The company may be trying to build a second major growth engine beyond Domino’s. India’s fried chicken market still has large growth potential, but scaling a new brand profitably takes time.

This will be an important area for investors to watch in the coming years.

What Investors Should Watch Now?

Going Forward, investors should focus on the improvement in same-store growth, margin recovery, demand trends in Domino’s India, growth of Popeyes and international business and profitability instead of only store expansion.

The market now wants quality growth, not just aggressive expansion.

Conclusion

HSBC’s target price cut reflects growing concerns around allowing growth and rich valuations in Jubilant FoodWorks.

The company still has strong brand value and long-term potential, but near-term challenges in demand and profitability are making investors more cautious.

The next few quarters will be important in deciding whether Jubilant FoodWorks can regain the market’s confidence.