Netflix’s Fundamentals Have Never Been Weaker – So Why Is the Stock Falling?

For years, investors viewed Netflix as a high-growth streaming company that prioritized subscriber growth over profitability. Today, the company looks very different.

Netflix generates billions in free cash flow, operates with industry-leading margins, maintains a healthy balance sheet, and continues to expand into advertising, gaming, and live sports. Yet despite these strengths, the stock has recently come under pressure.

This raises an important question:

If Netflix's business remains strong, why is the stock falling?

To answer that question, we first need to understand the company's fundamentals and what they reveal about Netflix's financial health.

Valuation Reflects Continued Growth Expectations

Netflix continues to trade at a premium valuation relative to many traditional media and entertainment companies. Investors are willing to pay higher earnings multiple because Netflix is still viewed as a growth company rather than a mature media business.

The market believes Netflix has several long-term growth drivers that can expand both revenue and profits over the coming years. These include its rapidly growing advertising business, the gradual expansion into gaming, increasing investments in live sports and events, and the company's ability to periodically raise subscription prices across its global user base.

Current PE v/s Forward PE

A particularly encouraging sign is that Netflix's Forward P/E ratio is lower than its current P/E ratio. This typically indicates that analysts expect earnings to grow faster than the stock price over the next few years. In other words, while the stock appears expensive based on today's earnings, it becomes relatively cheaper when measured against expected future profits.

For example, if a company trades at 50 times current earnings but only 40 times expected earnings next year, it suggests analysts expect profits to rise significantly. This is exactly the type of earnings growth investors are currently anticipating from Netflix.

Debt Is No Longer a Major Concern

A decade ago, Netflix relied heavily on borrowing to finance content production and expand its global streaming platform. During those years, the company regularly issued billions of dollars in debt to fund original shows, movies, and international growth.

That is no longer the case. Netflix now generates substantial cash flow from its operations, allowing it to fund most of its content spending internally rather than relying on new borrowing. As a result, the company's balance sheet is significantly healthier than it was during its aggressive expansion phase.

The current debt to equity ratio of the company is 0.54 which is decent. A lower debt burden also means Netflix spends less on interest payments, leaving more cash available for content creation, advertising initiatives, gaming investments, and potential shareholder returns.

Netflix Easily Covers Its Interest obligations

One of the clearest signs of Netflix's financial strength is its ability to comfortably service its debt obligations.

The company's operating income has increased significantly over the past several years as revenue has grown and profit margins have expanded. At the same time, interest expenses have remained relatively manageable. This has resulted in a strong interest coverage ratio, meaning Netflix generates many times more operating profit than it needs to pay annual interest on its debt.

The current interest coverage ratio of Netflix is 16.4 which means that Netflix is earning far more from its core business than is required to meet its debt obligations. This provides a substantial financial cushion and reduces the risk that debt could become a burden during periods of slower growth or economic uncertainty.

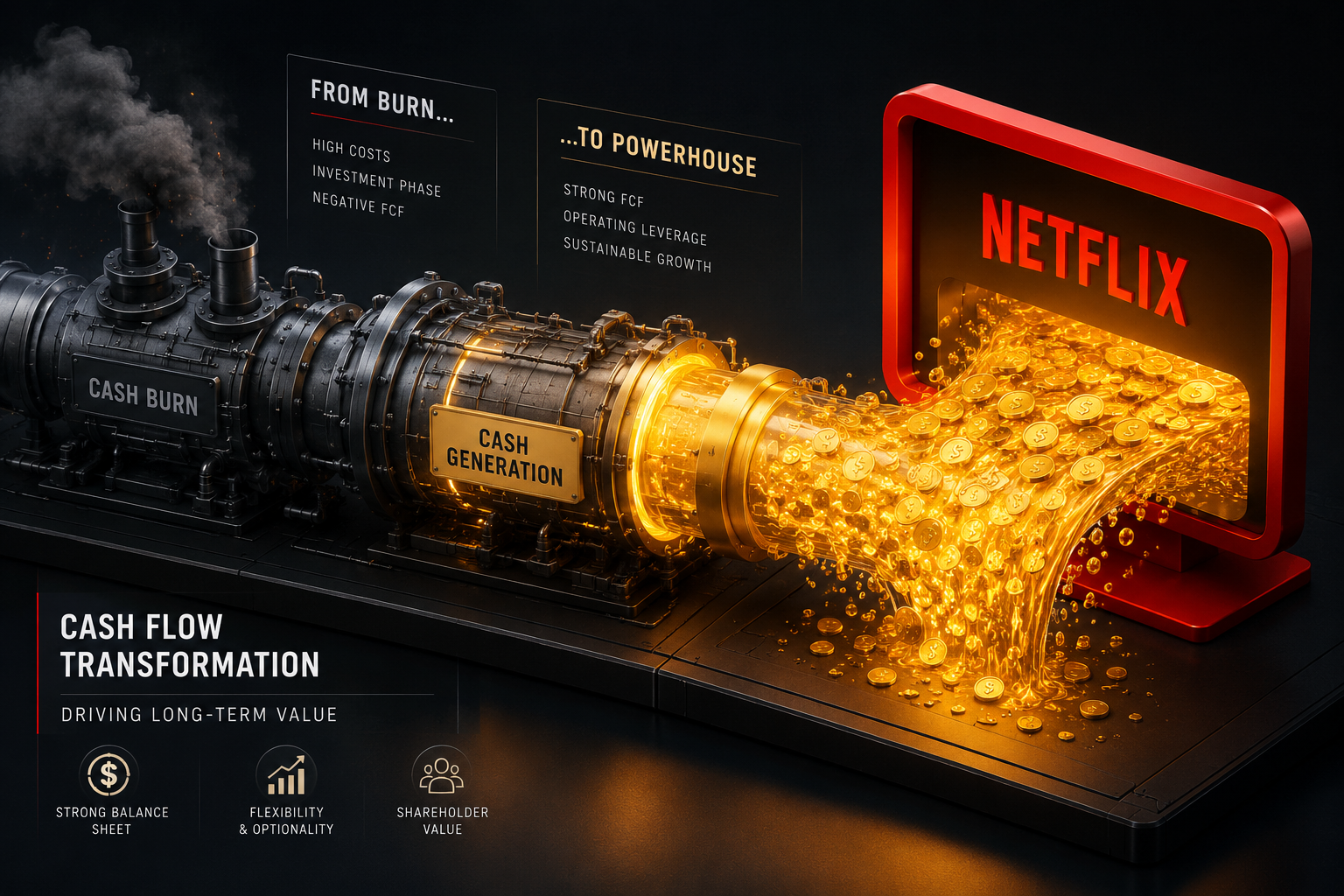

Cash Flow Continues To Improve

In 2024, Netflix produced approximately $10.1 billion in operating cash flow and nearly $9.4 billion in free cash flow. These figures are particularly impressive because they come after billions of dollars spent on content creation and platform investments.

The improvement over the past few years has been remarkable. Netflix generated just $1.6 billion of free cash flow in 2022, but that figure surged to nearly $6.9 billion in 2023 and remained at a similarly strong level in 2024. This demonstrates that Netflix has successfully transitioned from a cash-consuming growth company into a cash-generating entertainment powerhouse.

Strong cash generation gives management significant flexibility. Netflix can continue investing heavily in original content, expand its advertising platform, pursue opportunities in gaming and live sports, repurchase shares, and reduce debt - all without needing to raise additional capital. In fact, the company repurchased more than $6 billion of its own stock in 2024, highlighting the financial strength of its business model.

Source - Netflix financials

Investment Spending Signals Expansion, Not Weakness

Netflix continues to spend aggressively on future growth opportunities. The company is investing in:

- Advertising technology

- Video games

- Original content

- Live sports programming

These investments may create short-term costs, but they are designed to strengthen Netflix's competitive position over the long term.

Rather than slowing down, Netflix appears to be building multiple new revenue streams beyond traditional subscriptions.

If Fundamentals Are Strong, Why Is the Stock Falling?

Netflix's stock decline reflects a situation where the underlying business continues to grow, but investors have become increasingly concerned about several short-term challenges occurring simultaneously.

Brazil Tax Charge: The Biggest Immediate Shock

One of the biggest reasons behind Netflix's sharp stock decline was an unexpected tax charge related to Brazil.

The company was required to record a one-time tax expense of more than $600 million, stemming from a long-running tax dispute. Importantly, this was not related to the day-to-day performance of Netflix's business.

Operationally, the company continued to perform well. Revenue grew, subscriber engagement remained strong, and the business generated significant cash flow.

However, the large tax charge reduced Netflix's reported earnings for the quarter. Since investors closely track earnings results, the lower-than-expected profit overshadowed many of the company's positive operating metrics.

Reported vs. Adjusted Earnings

To see why the market overreacted, we have to look at the difference between Reported Net Income (which includes one-time legal/tax disasters) and Adjusted Net Income (which shows the true health of the core business).

When a company takes a one-time $600 million non-operational hit, it artificially drags down its earnings per share (EPS) for that specific quarter. Wall Street algorithms trigger automatic sell orders based on that headline.

However, human investors who strip away that single $600 million charge see that Netflix's actual subscription machine generated clean, predictable profits exactly as planned. The business didn't lose $600 million in performance; it just paid a one-time toll to the past.

As a result, the market reacted negatively, with Netflix shares falling roughly 10% in a single trading session, despite the underlying business remaining fundamentally healthy.

Warner Bros. Acquisition Created Fear

Another factor weighing on Netflix shares was speculation surrounding a potential acquisition of assets from Warner Bros. Discovery.

While the deal could have significantly expanded Netflix's content library and strengthened its competitive position, investors were concerned about the risks involved. Large acquisitions often raise questions about valuation, integration challenges, and regulatory approval.

As discussions attracted regulatory and political attention, uncertainty increased. Markets generally dislike uncertainty, especially when a transaction worth ten of billions of dollars is involved.

Although the deal offered potential long-term benefits, the lack of clarity surrounding its outcome added pressure to Netflix shares at a time when investors were already reacting to weaker-than-expected earnings.

Source: Netflix.com

Content Costs Are Rising

Netflix's success depends on its ability to continuously produce and acquire high-quality content. Popular series such as Stranger Things and Wednesday, along with investments in movies, live events, and sports rights, require substantial spending.

While these investments can help attract and retain subscribers, they also increase operating expenses. As Netflix expands its content offerings, the company must spend more to maintain its competitive advantage.

Management indicated that revenue is expected to continue growing, but expenses are also likely to rise. This raised concerns that profit margins may not expand as quickly as investors had hoped.

Although investing in content is essential for Netflix's long-term growth, the prospect of higher costs puts short-term pressure on investor sentiment and the stock price.

Investors Had Very High Expectations

Netflix is not valued like a mature media company. Instead, investors view it as a growth company and expect it to deliver strong revenue and earnings growth year after year.

Because of these high expectations, even small disappointments can trigger a negative market reaction. Investors are often focused not only on current results but also on what those results imply about future growth.

For example:

- Analysts expect revenue growth of 14%

- Netflix reports revenue growth of 13%

In absolute terms, the difference is small. The business is still growing at a healthy pace.

However, growth investors may interpret the slowdown as a sign that future growth could be weaker than previously expected. As a result, the market often reacts more strongly than the numbers alone would suggest.

This dynamic helps explain why Netflix shares can fall even when the company continues to grow revenue, subscribers, and profits. For growth stocks, missing expectations is often more important than the growth itself.

If you're interested in investing in companies like Netflix but aren't sure how to get started, I've created a step-by-step guide explaining how to invest in U.S. stocks from India. You can watch it here.

Final Verdict

Netflix's recent stock decline appears to be driven more by short-term concerns than by a weakening business.

The company continues to generate strong cash flow, maintains a healthy balance sheet, and is investing in multiple growth drivers, including advertising, gaming, and live sports. At the same time, investors have been rattled by the Brazil tax charge, acquisition uncertainty, rising content costs, and exceptionally high expectations.

While these factors may create near-term volatility, Netflix's core business remains fundamentally strong. For investors, the key question is not whether Netflix is still growing—it is whether the market has become too focused on short-term challenges and overlooked the company's long-term potential.