MosChip’s Promoter Shareholding Drop Explained – Corporate Alarm or Calculated Scaling?

When investors see promoter shareholding falling, the first reaction is often negative. The logic appears straightforward. If the people running the business are reducing their ownership, perhaps they have become less confident about the company's future.

MosChip Technologies presents an interesting case.

Between June 2023 and March 2026, promoter ownership declined from 51.23% to 39.83%. On the surface, such a sharp drop may appear alarming. However, a deeper investigation reveals a very different story.

The decline is not primarily the result of promoters selling shares in the open market. Instead, it is largely driven by a series of equity issuances used to acquire businesses, reward employees, and raise capital for expansion.

This distinction matters because promoter selling and promoter dilution can produce the same shareholding outcome while conveying entirely different signals.

The more important question for shareholders is not why promoter ownership fell, but whether the value created through these dilutive actions exceeds the value lost through reduced ownership and lower earnings per share.

The Denominator Effect: Selling vs. Dilution

Investors must understand a key corporate governance concept: dilution. Imagine a pizza divided into ten slices, and you own five of them, giving you 50% ownership. Now suppose five additional slices are created.

You still own the same five slices, but your ownership percentage falls from 50% to 33.33% because the total number of slices has increased. You have not sold anything; your share simply represents a smaller portion of a larger whole.

The same principle applies to companies. An investor’s ownership stake can decline when new shares are issued to employees, new investors, or acquisition targets, even if existing shareholders do not sell a single share. Understanding this distinction is essential to understanding the MosChip story.

What Happened to MosChip's Promoter Shareholding?

From June 2023 to March 2026, promoter ownership declined from 51.23% to 39.83%. This decline is more than 11 percentage points which naturally attracts attention. However, examining corporate actions during this period shows that most of the reduction resulted from an expanding share count rather than aggressive promoter exits.

The company repeatedly issued new shares through:

- Acquisition-related transactions

- ESOP allocations

- Preferential allotments

- Capital raising exercises

Each issuance increased the total number of outstanding shares. As the denominator expanded, promoter ownership percentages declined. The key issue therefore becomes whether these newly issued shares created enough value to justify the dilution.

The Vayavya Labs Acquisition: The Biggest Dilution Event

One of the most significant reasons behind MosChip's promoter dilution was the acquisition of Vayavya Labs. Instead of funding the entire transaction with cash, the company chose to issue equity as part of the consideration.

In simple terms, this is similar to purchasing a house by paying part of the price in cash and offering the seller a stake in your existing business for the remaining amount. The seller receives shares, the company preserves cash, and existing shareholders end up owning a smaller percentage of the enlarged company.

This approach is common in technology and engineering sectors, where acquisitions can be expensive and management often prefers to conserve cash for future investments, research and development, and working capital requirements. By using shares as currency, companies can pursue strategic acquisitions without placing excessive pressure on their balance sheets.

For MosChip, the acquisition of Vayavya Labs was aimed at strengthening its capabilities in semiconductor design, embedded systems, automotive engineering, product development, and other high-value engineering services. These are areas that are expected to play an increasingly important role as global demand for semiconductor and electronics design services continues to expand.

The Financial Architecture of the Deal

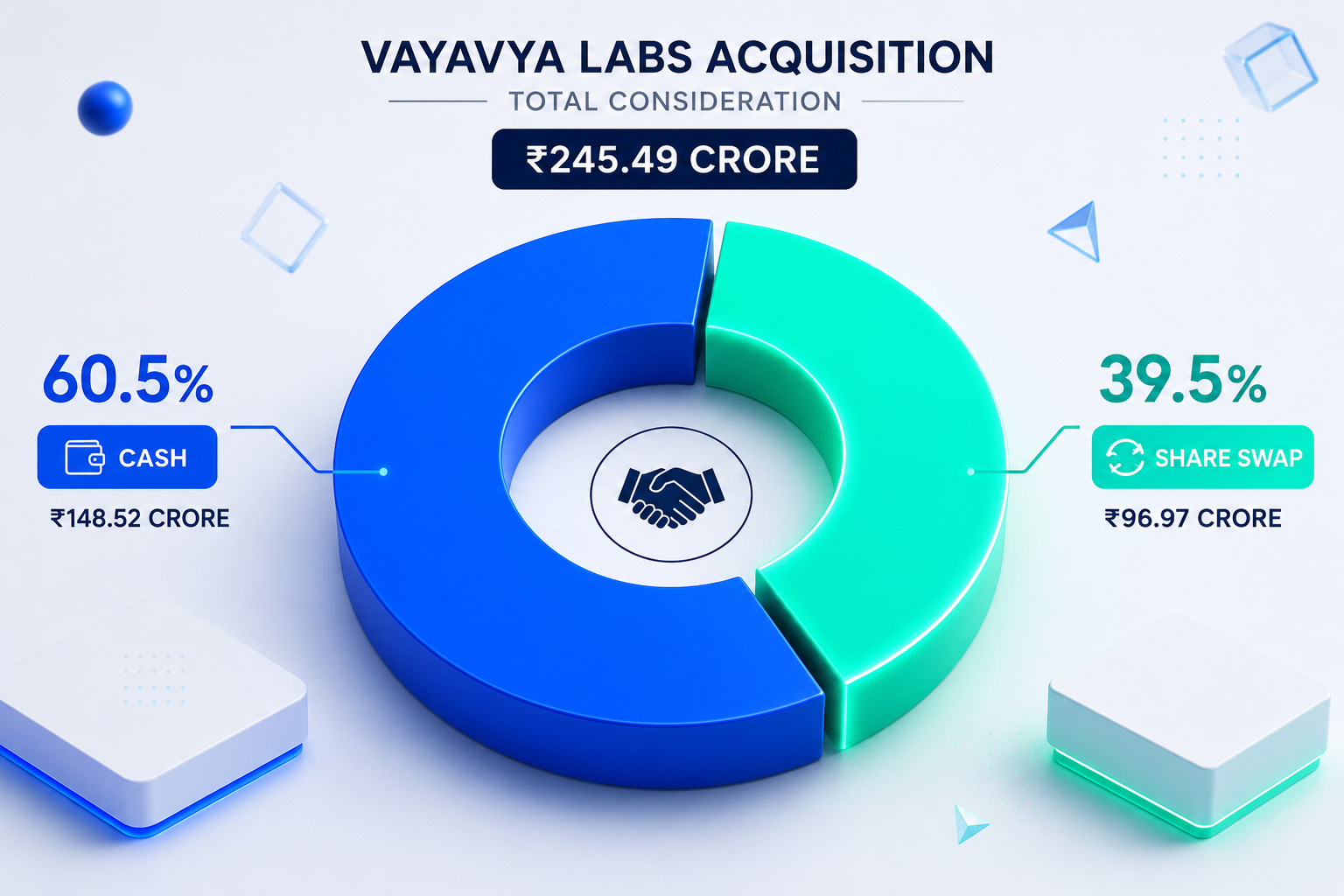

The Valuation: MosChip’s board approved the acquisition of a 73% controlling stake in Vayavya Labs for ₹245.49 crore.

The Hybrid Funding Structure: It wasn't a pure stock printing party. MosChip split the payment into 60.5% cash (₹148.52 crore) from internal accruals and 39.5% share swap (₹96.97 crore).

The Dilution Math: To cover the share swap, MosChip issued exactly 5,050,686 fresh equity shares (Face Value ₹2) to 67 selling shareholders of Vayavya.

The Price: The shares were locked in at ₹192 per share under SEBI ICDR guidelines.

The Talent Tax: Tracking the Silent Cost of ESOPs

The second major source of dilution comes from employee stock options (ESOPs). Semiconductor design is a talent-intensive business where skilled engineers and chip designers are often the company's most valuable assets.

To attract and retain top talent, companies frequently grant stock options. From management's perspective, ESOPs align employee interests with those of shareholders by making employees partial owners of the business.

However, ESOPs come with a cost. When employees exercise their options, the company typically issues new shares, increasing the total share count and diluting existing shareholders.

The impact is visible in earnings per share (EPS). For example, if a company earns ₹100 crore and has 100 crore shares, its EPS is ₹1. If the share count rises to 120 crores while profits remain unchanged, EPS falls to ₹0.83.

The business has not become weaker, but each shareholder now owns a smaller portion of the same profit pool. This is why investors should track not only revenue and profit growth but also the growth in shares outstanding.

Ultimately, ESOPs create value only when the benefits from attracting and retaining talent outweigh the dilution caused by issuing additional shares.

The Real Risk: EPS Dilution

The real risk of dilution lies in its impact on earnings per share (EPS). While most investors focus on revenue and profit growth, experienced investors pay closer attention to per-share growth.

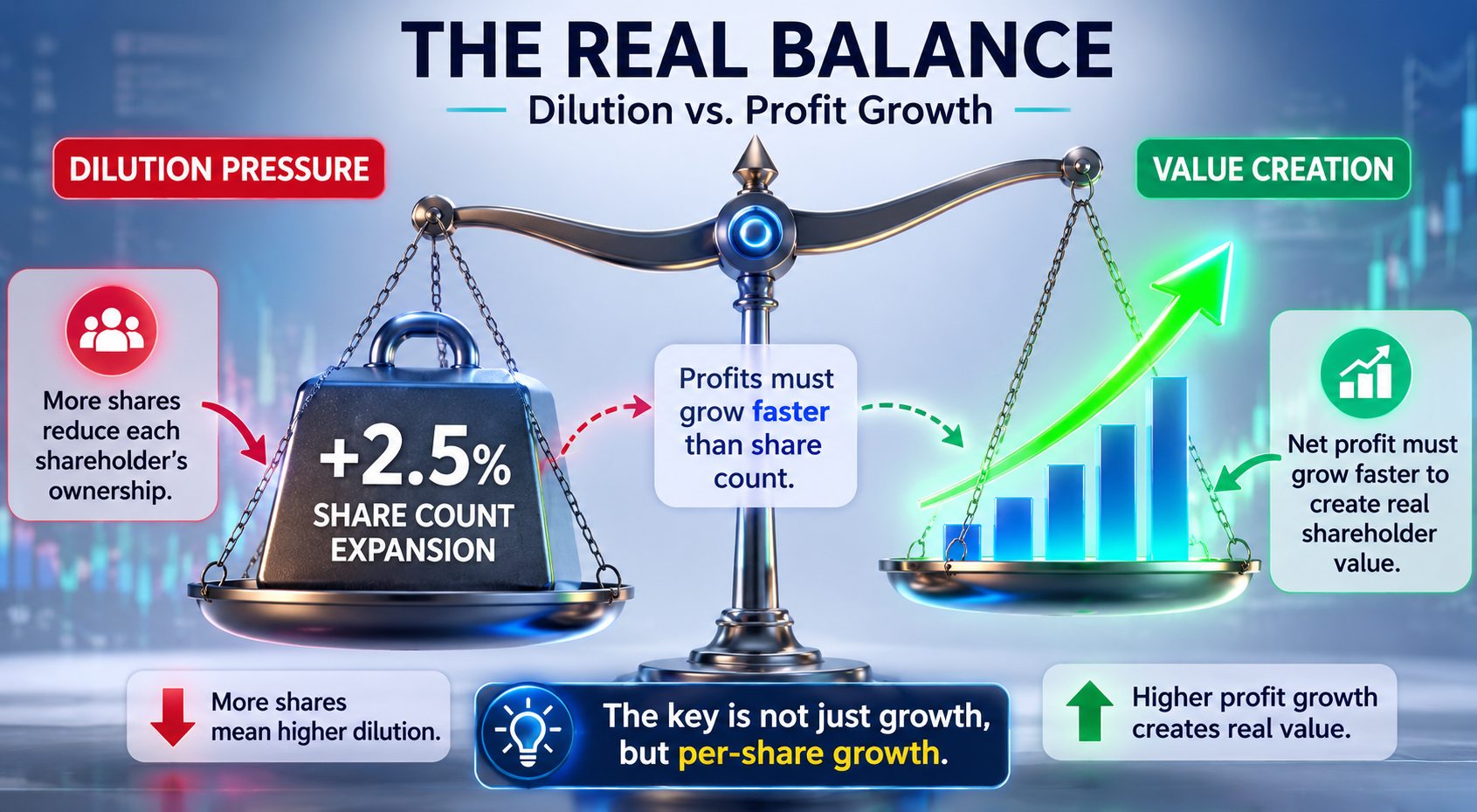

Let’s look at the raw, un-hypothetical math facing MosChip. The company's consolidated net profit for FY26 hovers around ₹23.63 crore on a total revenue base of ₹585.15 crore—meaning it operates on paper-thin net margins of roughly 4%. Meanwhile, its total outstanding share base has expanded to roughly 196 million shares.

When your share count grows by 2.5% to accommodate transactions like Vayavya, your net profit must expand by a larger delta just to keep Earnings Per Share (EPS) flat. With the stock trading at a triple-digit price-to-earnings (P/E) multiple of over 160x, the market has priced in flawless execution.

If Vayavya's profits do not hit the tape immediately, minority shareholders will face immediate, structural EPS compression. This is why dilution can become a concern. Shareholders may own a smaller percentage of a growing company, limiting the benefits they receive from that growth.

For MosChip, investors should track three metrics together: revenue growth, profit growth, and EPS growth. Revenue shows whether the business is expanding, profit shows whether earnings are increasing, and EPS reveals whether shareholders are actually benefiting.

Ultimately, EPS growth is the clearest measure of shareholder value creation because it reflects how much profit is available to each individual share.

The Preferential Issue Controversy

One of the most debated aspects of MosChip's recent capital allocation strategy is its preferential share issue. The company reportedly issued new shares at a price around 20% below the prevailing market price, raising important corporate governance questions.

The key concern is straightforward: why should new investors receive shares at a discount when existing shareholders purchased them at higher prices? Whenever shares are issued below market value, the economic benefit often shifts toward incoming investors.

A simple analogy helps explain this. Imagine a bakery worth ₹100 crore with 100 shares outstanding, making each share worth ₹1 crore. If the bakery issues 20 new shares at only ₹80 lakh each, the new investors gain ownership at a lower valuation than existing shareholders paid.

Some corporate governance observers questioned MosChip's decision to issue shares for the Vayavya Labs acquisition at ₹192 per share, around 20% below the stock's peak of ₹288.45.

However, the price was not set arbitrarily. Under SEBI's preferential allotment rules, the issue price must be calculated using a formula based on the stock's recent VWAP(Volume Weighted Average Price) over the previous 90 and 10 trading days. Since semiconductor stocks had corrected from earlier highs, the formula resulted in a price of ₹192.

Even so, the governance concern remains valid. Because the shares were issued at a lower valuation, MosChip had to issue more shares to meet its ₹96.97 crore obligation, increasing dilution for existing shareholders.

As a result, existing shareholders bear the dilution cost. Their ownership percentage declines, and part of the company's value is effectively transferred to the new investors through the discounted pricing.

For corporate governance-focused investors, this remains one of the most important aspects of MosChip's recent actions. The long-term outcome will depend on whether the benefits generated by the new capital outweigh the value transferred through the discounted share issuance.

here is the PDF of Intimation of Board Meeting under Regulation 29 (1) (d) and Regulation 30 of SEBI https://www.bseindia.com/xml-data/corpfiling/AttachHis/9c0ab8ca-13b5-4974-b756-cc051463b2fa.pdf

What Investors Should Watch Going Forward

Rather than focusing only on promoter shareholding, investors should evaluate whether management is creating value for each shareholder. The following five indicators can provide a clearer picture of MosChip's long-term performance.

Further Equity Dilution

Investors should monitor whether the company continues issuing new shares through acquisitions, preferential allotments, or other fundraising activities. Occasional dilution may be justified if it supports growth, but repeated issuances can steadily reduce existing shareholders' ownership.

The key question is whether dilution begins to stabilize after recent strategic initiatives. A stable share count makes it easier for shareholders to fully participate in future earnings growth.

EPS Growth

Earnings per share (EPS) is one of the most important metrics to track because it measures how much profit is attributable to each share. Strong profit growth alone is not enough if the share count is rising rapidly.

If MosChip's earnings grow faster than dilution, shareholders benefit. However, if new shares are issued at a pace that offsets profit growth, the value created for each shareholder may remain limited.

Acquisition Performance

The success of the Vayavya Labs acquisition will be a critical factor in evaluating recent dilution. Investors should assess whether the acquisition is contributing to higher revenue, stronger margins, and improved business capabilities.

A successful acquisition should generate returns that exceed the cost of the additional shares issued. If the expected synergies fail to materialize, shareholders may bear the dilution without receiving adequate benefits in return.

ESOP Expansion

Employee stock options can be a powerful tool for attracting and retaining talented engineers in the semiconductor industry. When used responsibly, ESOPs help align employee interests with those of shareholders.

However, investors should watch whether ESOP issuances remain reasonable. Excessive stock option grants can gradually increase the share count and reduce the benefits of future earnings growth for existing shareholders.

Capital Allocation Discipline

Perhaps the most important factor is how management allocates capital in the years ahead. Investors should evaluate whether future growth initiatives are funded through internally generated cash flows or through additional equity issuance.

Companies that can finance expansion using their own cash generation often create greater long-term value for shareholders. Frequent reliance on new share issuances may signal that growth is coming at the cost of ongoing dilution.

Ultimately, these five indicators should be viewed together. Strong revenue growth, disciplined capital allocation, successful acquisitions, controlled ESOP issuance, and consistent EPS growth would suggest that MosChip's recent dilution is creating long-term shareholder value rather than destroying it.

Before making an investment decision, investors should also consider the key risks factors which are faced by the company. here is our video in which I have briefly explained the risk factors

Conclusion

MosChip's decline in promoter shareholding from 51.23% in June 2023 to 39.83% in March 2026 may initially appear concerning. A closer examination, however, suggests that the fall is largely the result of equity dilution rather than outright promoter selling.

The company used shares to acquire businesses, reward employees, and raise capital for expansion. These actions can accelerate growth, preserve cash, and strengthen competitive positioning. Yet they also come with a cost: every new share reduces the ownership percentage of existing shareholders and places pressure on earnings per share.

For investors, the central issue is not whether promoter ownership declined. The central issue is whether the benefits generated by acquisitions, ESOPs, and capital raising exceed the long-term cost of dilution.

If MosChip can convert these newly issued shares into substantially higher profits and stronger competitive advantages, the dilution may ultimately prove justified. If not, shareholders may discover that growth in size did not translate into growth in per-share value.

Ultimately, MosChip is executing a calculated leap, not signaling a red flag. Management has successfully used its equity as a currency to weaponize its talent pool and buy intellectual property. Now, the operational machinery must sweat those assets aggressively enough to reverse the EPS drag, proving to equity researchers that this smaller slice of the pie was worth the wider table.