Medanta’s ₹4,500 Crore Expansion Plan: Where Will The Money Come From?

Growth stories are exciting.

Funding them is where the real analysis begins.

Over the next five years, Medanta plans to invest approximately ₹4,524 crore across new hospitals, capacity expansions, medical infrastructure, and a new medical college. For context, Medanta generated ₹4,509 crore of revenue in FY26.

In other words, the company plans to spend an amount roughly equivalent to an entire year's revenue on future growth. Whenever investors hear numbers of this magnitude, the immediate assumption is usually the same:

More debt. More dilution. More financial risk.

But that assumption may not tell the full story. Medanta enters this expansion cycle from a position of financial strength, with growing profitability, healthy cash generation, and one of the strongest balance sheets in the hospital sector.

This raises an important question:

Does Medanta actually need significant external funding to execute its ₹4,500 crore expansion plan?

Or is the market overestimating the financial risk associated with this capex cycle?

The answer lies in understanding not just how much Medanta plans to spend, but how the company intends to finance that spending over the coming years. This article breaks down Medanta's ₹4,500 crore expansion program, the expected funding sources, potential debt requirements, and what the expansion could mean for shareholders.

Understanding The ₹4,500 Crore Expansion Plan

Before discussing funding, it is important to understand exactly what Medanta plans to build.

The ₹4,524 crore capex program is not a single project or a one-time investment.

Instead, it represents a multi-year expansion strategy spanning new hospitals, capacity additions, medical education infrastructure, and supporting healthcare facilities.

This distinction matters because the financial risk profile of a diversified expansion program is very different from that of a single large project.

Broadly, the planned investments include:

- New Greenfield Hospitals – Expanding Medanta's presence into new healthcare markets.

- Brownfield Capacity Additions – Increasing bed capacity and infrastructure at existing hospitals.

- Medical College Development – Building educational infrastructure that can support future doctor availability and create an additional revenue stream.

- Clinical Infrastructure & Equipment – Investments in advanced medical technology, specialized departments, and supporting facilities.

The Key Insight

Many investors focus solely on the ₹4,500 crore headline figure.

However, the more important takeaway is that the spending is spread across multiple growth initiatives that are expected to become operational at different points in time.

As these projects gradually come online, they can begin generating revenue and cash flows that may help support the next phase of expansion.

This makes the capex program less about a single large expenditure and more about building Medanta's future growth platform over the next decade.

The largest project is the upcoming Mumbai hospital, which alone accounts for over ₹1,250 crore of planned investment.

This will be followed by the Gurugram medical college project, the Pitampura hospital, and the Guwahati hospital.

Combined, these four projects account for nearly two-thirds of the total capex commitment.

This concentration is important because it allows investors to identify where most of the future funding requirements will arise.The company is also investing in maintenance capex across existing facilities and expanding capacity in Lucknow, Patna, Ranchi and Noida. Taken together, the expansion pipeline could add more than 3,000 beds across the network over time.

The scale of the plan makes it one of the most ambitious growth programs currently underway in Indian private healthcare. However, the size of the capex figure alone can be misleading. Because Medanta is not required to spend ₹4,524 crore immediately. And that distinction changes the funding equation dramatically.

The Biggest Misconception About This Capex Plan

When investors hear that a company plans to spend ₹4,500 crore, many immediately assume that the company must raise a similar amount of capital upfront.

That assumption is usually incorrect.

Large hospital expansion projects are rarely funded in a single year.

Hospitals take years to build, commission, and operationalize. Land acquisition, construction, equipment installation, licensing, and staffing all happen in phases.

As a result, the cash outflow is spread across multiple years rather than occurring all at once.

For example:

- Construction spending is incurred gradually as projects progress.

- Medical equipment purchases are often made closer to commissioning dates.

- Regulatory approvals and project timelines naturally stagger capital deployment.

- Different projects become operational at different points in time, reducing the need for upfront funding.

This distinction is critical because it changes how investors should think about the funding requirement.

The ₹4,524 crore figure represents the total planned investment over several years, not the amount Medanta needs to finance immediately.

This timeline fundamentally changes the funding challenge. The company does not need ₹4,500 crore today.

Instead, it needs approximately ₹800–900 crore during FY27, followed by a lower spend in FY28, with a significant portion of the expenditure occurring later.

This staggered schedule creates an important advantage. While construction is underway, Medanta's existing hospitals continue generating cash. That operating cash flow can then be recycled into new projects.

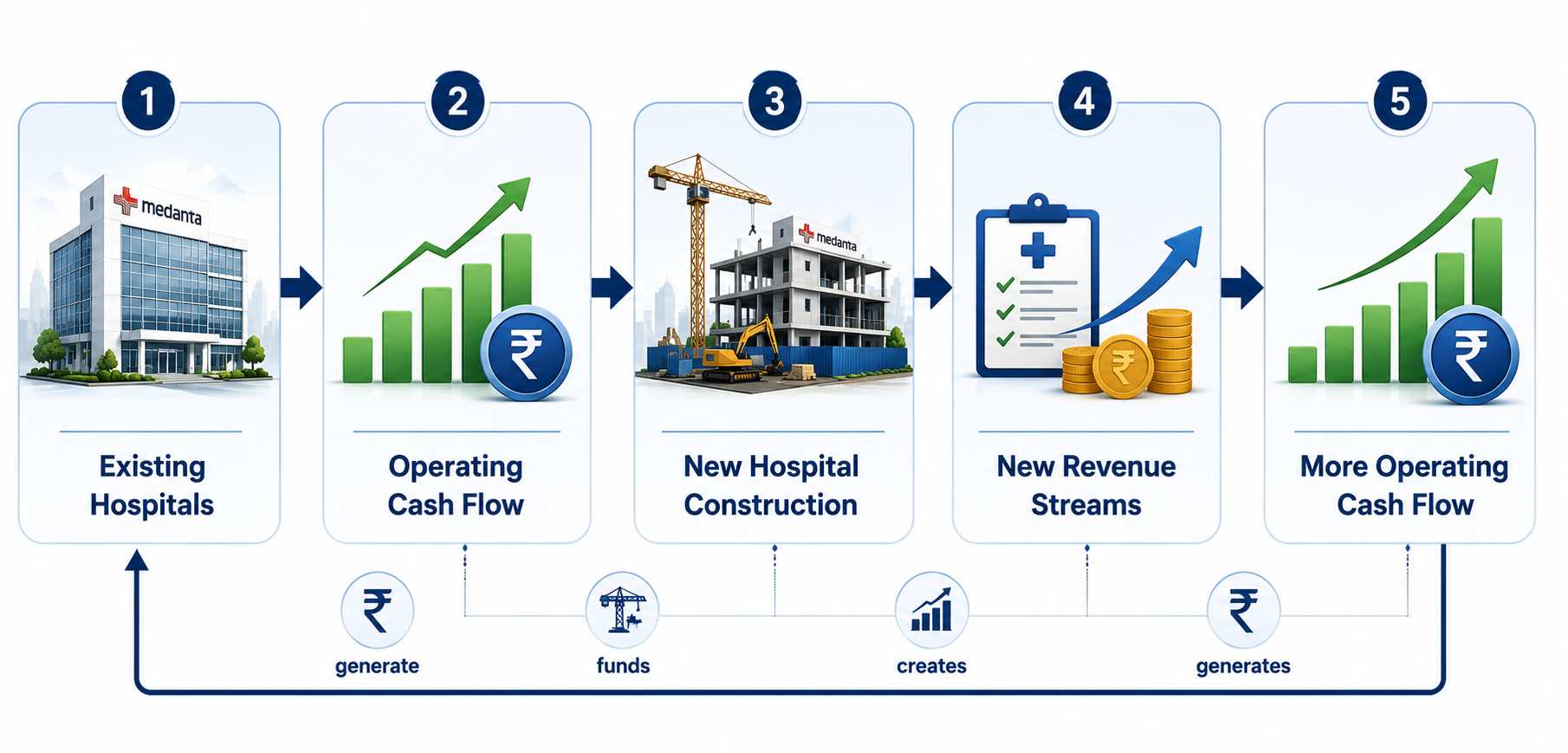

Funding Source 1: Existing Hospitals Are Financing Future Hospitals

Every large expansion program ultimately depends on one thing:

Cash generation.

For Medanta, the first and most important funding source is internal accruals—the cash generated from its existing hospital network.

Every surgery performed, patient admitted, diagnostic test conducted, and pharmacy transaction completed contributes to operating cash flow.

That cash flow does not simply support day-to-day operations.

It also becomes the primary source of capital for future expansion.

Many investors focus on cash balances when evaluating a company's ability to fund growth.

However, for a growing hospital chain, ongoing cash generation is often far more important than cash already sitting on the balance sheet.

A hospital that consistently generates strong operating cash flows can reinvest those funds into new hospitals, capacity expansions, medical equipment, and infrastructure.

This creates a powerful growth cycle:

Existing Hospitals → Operating Cash Flow → Expansion Investments → New Hospitals → Higher Cash Flow

The stronger the performance of Medanta's current hospitals, the greater its ability to fund future growth without relying heavily on external capital.

The Key Insight

The ₹4,500 crore expansion plan is not being financed by a single pool of money.

Instead, a significant portion of the funding is expected to come from the cash flows generated by Medanta's existing hospitals over the next several years.

In effect, today's hospitals are helping finance tomorrow's hospitals.

Why Internal Accruals Matter?

Imagine two companies. Both want to build a new hospital. The first company has no meaningful cash generation. It must borrow almost everything.

The second company generates healthy cash flows every year. It can fund a large portion of the project internally.

Which company faces less financial risk?

Obviously the second one.

This is why internal accruals are so important. They reduce reliance on lenders and provide management with greater control over expansion plans.

For Medanta, existing hospitals are not just healthcare assets. They are also funding engines for future growth.

Funding Source 2: Existing Financial Strength

The second funding source is Medanta's balance sheet.

Management has repeatedly emphasized that the company enters this expansion cycle from a position of financial strength. This distinction is important. Many companies undertake large expansion programs because growth has slowed or because they need additional scale to improve profitability.

Medanta's situation is different. The company is already operating a large and profitable hospital network that generates substantial cash flows and maintains a healthy balance sheet.

A strong financial position provides several advantages during a major capex cycle:

- Greater Funding Flexibility – Expansion can be funded through a combination of cash flows, existing liquidity, and debt.

- Lower Financial Risk – The company is not entering the expansion phase with an overstretched balance sheet.

- Better Access To Capital – Financially strong companies typically find it easier to raise debt on favorable terms.

- Improved Execution Capability – Management can focus on building hospitals rather than worrying about liquidity.

The Key Insight

Medanta is not attempting to fund growth from a position of weakness.

It is expanding while already operating a profitable healthcare platform with strong cash generation and financial flexibility.

That foundation significantly improves the company's ability to execute its ₹4,524 crore expansion plan over the coming years.

Funding Source 3: Project-Specific Debt

No large expansion program can be funded entirely through internal cash generation.

Debt is usually part of the funding mix, and Medanta has acknowledged that project-specific borrowing may be used where required. However, there is an important distinction between using debt to fund growth and using debt to sustain operations.

Medanta falls into the first category.

The company is not borrowing because its existing business is struggling to generate cash. Instead, any future borrowing is expected to support the construction of new hospitals and expansion projects that can generate revenue for decades.

Hospitals are long-life assets.

A new hospital requires significant upfront investment but can continue generating revenue and cash flows for many years after becoming operational.

As a result, using a reasonable amount of debt to finance hospital construction is common across the healthcare industry.

The key consideration is whether the future earnings generated by these projects are sufficient to comfortably service the additional borrowing.

The Key Insight

Investors should not view future debt in isolation.

The more relevant question is whether the company is deploying borrowed capital into assets that can create long-term value.

In Medanta's case, the company expects to use project-specific debt to finance revenue-generating healthcare infrastructure rather than fund day-to-day operations.

That makes it a growth-enabling tool rather than a sign of financial stress.

Why Debt Alone Is Not The Story?

Whenever investors hear about a large capex announcement, attention quickly shifts to debt. That reaction is understandable. Large projects often lead to higher borrowings.

However, focusing only on debt can be misleading. The more important question is whether the company can comfortably manage any additional borrowing.

In Medanta's case, management has emphasized balance sheet discipline throughout its expansion plans. The company has also indicated that it will link borrowing decisions to specific projects rather than rely on aggressive leverage.

For long-term investors, the second question is far more important.

The Real Funding Engine

When all three funding sources are combined, the picture becomes much clearer. Medanta is not relying on a single source of capital to fund its ₹4,524 crore expansion plan.

Instead, the company is building a layered funding structure where multiple sources work together. Internal cash generation from existing hospitals provides the primary funding base.

The balance sheet provides financial flexibility and liquidity. Project-specific debt can be deployed where additional capital is required.

Together, these sources create a funding framework that allows expansion projects to move forward without depending excessively on any one source of capital.

Many investors view the ₹4,500 crore capex plan as a financing challenge. Management appears to view it differently.

The company is effectively using the cash flows generated by today's hospitals, supported by balance sheet strength and selective borrowing, to build the next generation of hospitals. This significantly reduces the need for aggressive debt accumulation or equity dilution.

The Key Insight

The real funding engine behind Medanta's expansion is not debt.

It is the combination of:

- Strong Operating Cash Flows

- Existing Financial Strength

- Prudent Project-Specific Borrowing

As long as the existing hospital network continues to generate healthy cash flows, these three funding pillars can reinforce each other and support the company's long-term growth ambitions.

What Investors Should Monitor?

The success of Medanta's expansion program will ultimately depend on execution rather than announcements.

While the ₹4,524 crore capex plan attracts attention, the more important question is whether the company can convert this investment into profitable growth over time.

Investors may benefit from tracking a few key indicators.

1) Operating Cash Flow

A large part of the expansion strategy relies on internal cash generation.

Healthy and growing operating cash flows would indicate that existing hospitals continue to provide the financial resources needed to support future expansion.

2) Debt Levels

Some increase in borrowing is expected during a capex cycle of this size.

The key is whether debt rises in a measured and sustainable manner relative to earnings and cash generation.

3) Occupancy Growth

New hospitals create value only when beds are filled.

Occupancy trends can provide early signals regarding patient demand, hospital utilization, and the success of newly commissioned facilities.

4) Return on Capital

Perhaps the most important metric is return on capital.

The Key Insight

The headline capex number tells investors how much Medanta plans to spend.

These operating and financial indicators reveal whether that spending is actually creating value.

In the long run, successful execution—not the size of the investment—will determine the success of Medanta's expansion strategy.

Conclusion

At first glance, a ₹4,524 crore expansion plan appears enormous.

And it is.

The company is effectively building multiple hospitals, expanding capacity, investing in medical education, and creating the foundation for its next phase of growth.

However, the funding picture appears more balanced than the headline number initially suggests. The company will deploy the capex gradually over several years rather than all at once. Existing hospitals will generate a significant portion of the required funding through operating cash flows. A strong balance sheet provides financial flexibility.

And project-specific debt can supplement internal resources where required. As a result, the central investment question is not whether Medanta can raise ₹4,500 crore. The more important question is whether management can deploy that capital efficiently and generate attractive returns from the assets it creates.

If the new hospitals achieve healthy occupancy levels, maintain strong clinical outcomes, and replicate the economics of Medanta's existing facilities, today's capex could become the foundation for the company's next decade of growth.

For now, management's approach appears focused on balancing ambitious expansion with financial discipline. And ultimately, that combination may prove just as important as the expansion itself.