India’s Aviation Market Size and Growth Prospects

Twenty years ago, air travel in India was considered a luxury. Today, it is becoming an essential part of the country's transportation system. Millions of Indians are flying for business, tourism, education, healthcare, and family visits. As incomes rise and connectivity improves, flying is gradually replacing long train journeys for a large section of the population.

When most people hear "aviation industry," they immediately think of airlines like IndiGo or Air India. In reality, airlines are just one part of a much larger ecosystem. Every time an aircraft takes off, hundreds of businesses participate in generating revenue - from airports and fuel suppliers to aircraft manufacturers, maintenance companies, software providers, catering firms, logistics companies, and financial institutions.

This is what makes India's aviation sector one of the country's most exciting long-term growth stories.

The opportunity is not simply that more people are flying. The opportunity lies in the fact that India is still significantly underpenetrated compared to developed economies. The industry is expanding from a relatively low base, giving it decades of potential growth rather than just a few years.

For investors, understanding where the aviation market stands today - and where its future growth will come from - is far more important than simply knowing passenger numbers.

The Numbers Behind the Boom: Market Size and Passenger Volume

To understand where Indian aviation is heading, we first need to look at how rapidly the industry has grown. In 2020, during the COVID-19 pandemic, India's aviation market was valued at around ₹80,200 crore.

As travel demand recovered, the industry witnessed remarkable growth, reaching an estimated ₹1.40 lakh crore in 2025. Looking ahead, the market is projected to almost triple and reach ₹3.92 lakh crore by 2034, reflecting the strong long-term growth potential of the sector.

Annual domestic passenger traffic has already climbed to around 167 million passengers, and the Ministry of Civil Aviation aims to increase this to 400 million passengers annually by 2030.

While commercial aviation commands the lion's share of the market (nearly 80%), an unexpected driver is military aviation. Fueled by the government's Atmanirbhar Bharat (self-reliant India) initiative, defense aviation is actually growing the fastest, highlighted by massive multi-billion-dollar contracts for indigenous fighter jets like the Tejas Mark-1A.

Geographically, the market is also shifting balance. While Western India (anchored by Mumbai) historically dominated with over 32% of the market share, Eastern and Northeastern India are emerging as the fastest-growing regions, expanding at a CAGR of nearly 12.8%.

The Four Pillars Driving the Growth

India’s aviation boom isn't an accident; it is the result of four powerful, intersecting forces.

The Rise of the Aspirational Middle Class

Over 350 million Indians have transitioned into disposable income brackets where time is valued over marginal cost differences.

For routes longer than 500 kilometers, the price gap between an air ticket and a premium air-conditioned train ticket has narrowed significantly. The baseline consumer behaviour has fundamentally shifted: flying is no longer a special occasion event; it is a practical utility.

The UDAN Scheme and Regional Democratization

The government’s UDAN (Ude Desh ka Aam Nagrik) regional connectivity scheme has rewritten the rules of the industry. By subsidizing unserved routes and capping fares for short flights, UDAN expanded India’s operational airport network from just 74 airports in 2014 to roughly 160. Tier-2 and Tier-3 cities - like Darbhanga, Jharsuguda, and Kalaburagi - which were completely cut off from the aviation map, now generate thousands of daily flyers.

Aggressive Fleet Expansion

Indian airlines are placing the largest aircraft orders in global aviation history. Collectively, Indian carriers have more than 1,000 aircraft on order.

- IndiGo continues its high-frequency, low-cost dominance by locking in hundreds of narrowbody A320-family jets.

- Air India, under the unified ownership of the Tata Group, is undergoing a massive transformation (Vihaan.AI). By merging with Vistara and Air India Express, Tata is building a multi-brand powerhouse capable of taking back the international long-haul market from Gulf carriers, placing historic orders for both narrowbody and widebody planes.

- Akasa Air has carved out its own space as an aggressive, fast-growing challenger, adding capacity at record speed.

The E-Commerce Cargo Explosion

Aviation isn't just about people; it's about packages. E-commerce penetration in smaller Indian cities grew past 35%, driving a 23% annual surge in express air-cargo volumes.

All-cargo freighters operated by players like Blue Dart and Delhivery are running at near-peak utilization, aided by newly relaxed night-parking rules and priority airport slots.

The Turbulence: Hidden Gaps and Structural Weaknesses

Despite the stellar growth metrics, the Indian aviation industry operates on razor-thin margins and faces severe, systemic headwinds. In fact, rating agencies like ICRA recently adjusted their industry outlook to negative, highlighting that beneath the glitz of record plane orders lie deep structural pain points.

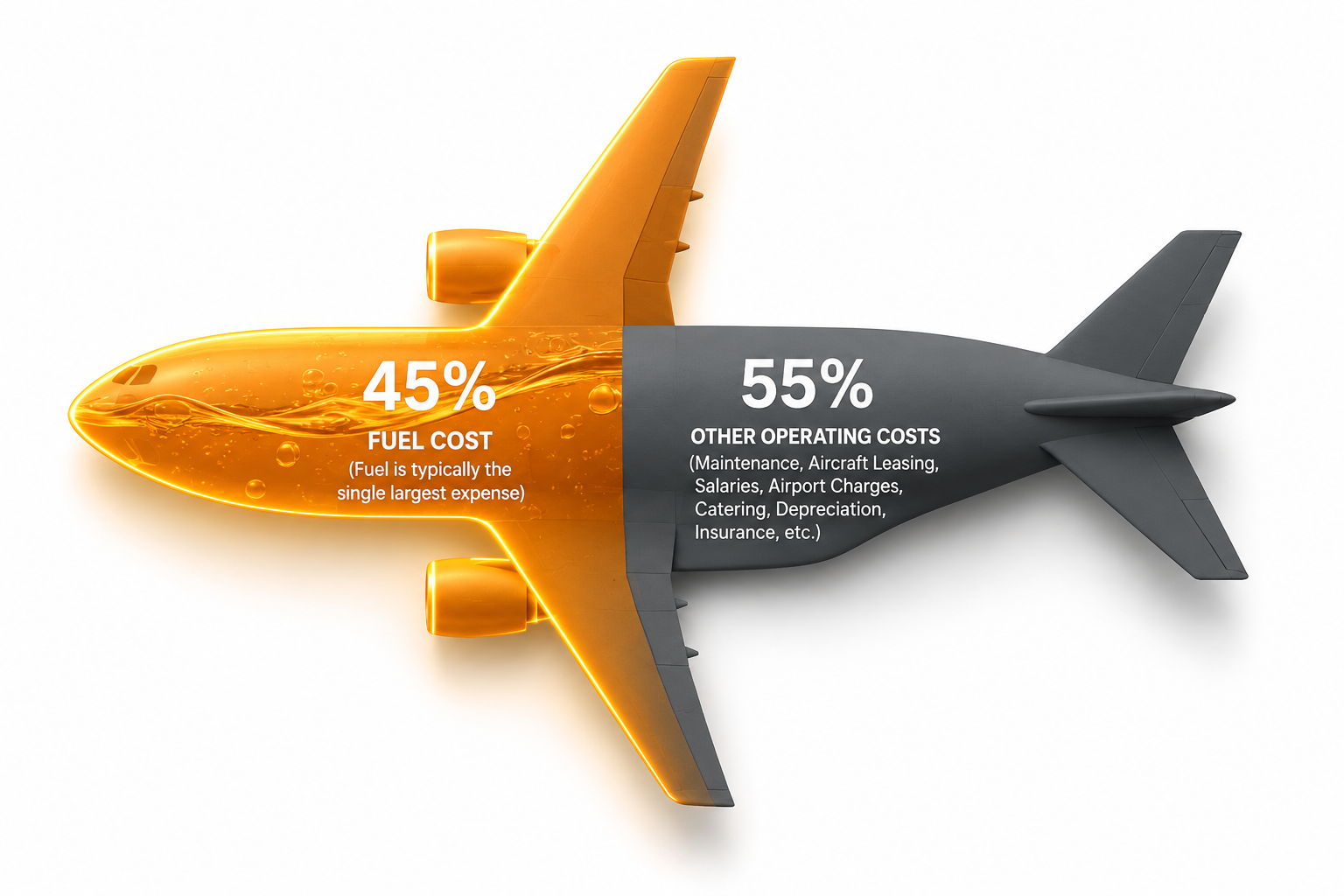

The 40% Fuel Tax Trap: Aviation Turbine Fuel (ATF) accounts for a staggering 35% to 45% of an Indian airline's total operating costs. Compounding this issue, India's state-level Value Added Tax (VAT) structures create artificial cost disparities, ranging anywhere from 1% to 30% depending on where a plane refuels.

Furthermore, Indian carriers historically hedge only about 15% of their fuel needs, leaving them dangerously exposed to global oil spikes compared to international peers who hedge 60% to 80%.

Beyond fuel, the industry faces three critical bottlenecks:

- The Dollar-Rupee Mismatch: Most airline revenue is earned in Indian Rupees (INR), but major expenses - such as aircraft lease agreements, spare parts, and international maintenance - are dollar-denominated ($). Persistent currency depreciation acts as a constant drain on profitability.

- The Talent Drought: India is facing an acute shortage of skilled commercial commanders, experienced line pilots, and specialized Aircraft Maintenance Engineers (AMEs). While training academies are spinning up, the supply simply cannot keep pace with the influx of new aircraft.

- Supply Chain and Engine Snags: Global supply chain constraints have grounded dozens of aircraft across Indian fleets due to delayed engine deliveries and lack of components, freezing capacity exactly when passenger demand is at its peak.

Future Outlook: The Next Decade in the Skies

The coming decade will determine whether India can convert its massive volume into sustainable value. We are likely to see the market consolidate into a powerful duopoly, with the Tata Group (Air India) dominating the full-service and international segments, and IndiGo firmly commanding the low-cost domestic grid. Challengers like Akasa Air will need to maintain intense cost discipline to protect their niches.

Furthermore, India is aggressively positioning itself to become a global hub for MRO (Maintenance, Repair, and Overhaul) services. Historically, Indian airlines flew their planes to Europe, Sri Lanka, or Singapore for heavy maintenance, losing millions in transit costs and downtime. By lowering local taxes and setting up dedicated MRO zones near new greenfield airports, India aims to keep that business - and the highly skilled jobs that come with it - within its borders.

Finally, expect a massive push toward sustainability. As the country aims for net-zero goals, the adoption of Sustainable Aviation Fuel (SAF) blends and the deployment of next-generation turbofan engines will take center stage.

Source - India Aviation

Conclusion

India’s aviation market is no longer just a story of potential; it is a live demonstration of economic mobility. The sheer velocity of passenger growth, combined with an unprecedented infrastructure rollout, has turned the subcontinent into the most watched aviation arena in the world.

If the industry can navigate the volatile traps of fuel pricing, fix its domestic supply chains, and build out its regional airports, the next decade won't just see more Indians flying - it will see India anchoring the global economics of the sky.