How Commercialisation of 5G will bring new stream of revenue for Airtel and Reliance Jio?

India completed one of the fastest 5G rollouts in telecommunications history. In less than three years, the country’s largest operators, Airtel and Reliance Jio, deployed nationwide 5G networks, covering hundreds of millions of users and investing tens of thousands of crores in spectrum purchases and infrastructure upgrades. Yet despite the technological achievement, investors continue to ask a critical question: where will the returns come from?

The answer lies in understanding that 5G is not merely a faster version of 4G. If consumers continue paying roughly the same monthly tariffs while using more data, telecom operators gain little financial benefit from their massive investments. The real opportunity emerges when 5G evolves from a connectivity service into a digital infrastructure platform capable of powering homes, factories, enterprises, vehicles, and intelligent devices.

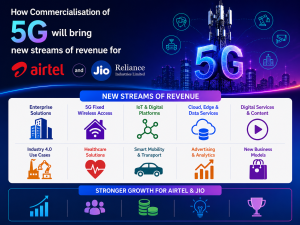

For Airtel and Jio, the commercialisation of 5G could create multiple high-margin revenue streams that extend far beyond traditional mobile subscriptions. The next phase of competition will not be about acquiring more users but about extracting greater value from every user, enterprise, and connected device on their networks.

The Challenge: Monetising a Multi-Billion Dollar Investment

India’s telecom sector spent more than ₹1.5 lakh crore in the 2022 spectrum auction alone, with Jio committing nearly ₹88,000 crore and Airtel investing over ₹43,000 crore. The subsequent rollout of nationwide 5G networks added billions more in capital expenditure.

Historically, telecom operators justified such investments through subscriber growth.

However, India’s mobile market is already highly penetrated, leaving limited room for meaningful subscriber expansion. The industry’s next growth phase must therefore come from higher revenue per user and entirely new business categories.

This is particularly important because India remains one of the world’s cheapest telecom markets. Airtel’s average revenue per user (ARPU) climbed to ₹257 by the close of FY26, while industry benchmarks remain significantly below global averages. For telecom operators, increasing ARPU by even ₹50 per month across hundreds of millions of subscribers can translate into thousands of crores in incremental annual revenue.

The commercialisation of 5G provides several pathways to achieve exactly that.

Airtel and Jio Are Not Playing the Same 5G Game

India’s two largest telecom operators may be competing in the same market, but they are pursuing fundamentally different 5G strategies. Understanding this distinction is critical because it will largely determine how each company monetises its network over the next decade.

Reliance Jio opted for a Standalone (SA) 5G architecture, building a dedicated 5G core network from scratch. The company also acquired significant holdings of the premium 700 MHz spectrum during the 2022 spectrum auction. This approach required substantially higher upfront capital expenditure, but it gives Jio access to capabilities such as network slicing, ultra-low latency applications, and large-scale industrial IoT deployments. In effect, Jio is making a long-duration bet that enterprise digital transformation will become one of the most lucrative opportunities in Indian telecom. Check more information about this in our latest video.

Airtel’s strategy is often described as a Non-Standalone (NSA) counterpoint to Jio’s Standalone (SA) network, but that characterisation is becoming increasingly outdated. Airtel initially used NSA architecture to accelerate deployment and reduce capital intensity by leveraging its existing 4G infrastructure. However, as enterprise use cases and network traffic evolve, the company has begun migrating key parts of its network toward Standalone capabilities through partnerships with Ericsson and other vendors.

This evolution suggests that Airtel’s NSA approach was less a technological limitation and more a capital-allocation decision. By delaying a full SA rollout, Airtel preserved cash flows during the industry’s heaviest investment cycle while retaining the flexibility to upgrade network capabilities as commercial demand emerges. In contrast, Jio incurred higher upfront costs by building a dedicated 5G core from the outset, effectively placing a larger bet on future enterprise, IoT, and network-slicing revenues.

The investment implication is clear. Jio is prioritising future enterprise monetisation, while Airtel is emphasising capital efficiency. The success of each strategy will ultimately depend on how quickly India’s enterprise 5G ecosystem matures.

Fixed Wireless Access: A Massive Opportunity With Hidden Costs

Fixed Wireless Access is no longer a future opportunity for Indian telecom operators; it is already reshaping the broadband market. Reliance Jio’s AirFiber business expanded rapidly during FY26, helping the company build a broadband base of 27.1 million users by the end of March 2026 with its subsidized AirFiber (FWA) connections alone accounting for roughly 13 million of those subscribers. This makes Jio one of the largest FWA operators globally and highlights how 5G is beginning to disrupt traditional cable and fixed-line broadband providers.

The appeal is obvious. Instead of waiting months for fibre deployment, households can receive high-speed broadband through wireless infrastructure that already exists. For telecom operators, broadband customers typically generate significantly higher revenue than mobile subscribers and often remain with providers longer, improving customer lifetime value.

Yet scale does not automatically translate into profitability. Every new AirFiber connection requires Customer Premise Equipment (CPE), typically costing ₹4,000-₹5,000, much of which is subsidised by operators. As subscriber additions accelerate, the industry must balance customer acquisition, network capacity, and equipment costs to ensure that growth ultimately converts into attractive returns on capital.

Enterprise 5G May Become the Highest-Margin Revenue Stream

While consumer 5G attracts the headlines, enterprise adoption may ultimately generate the highest returns on invested capital.

The importance of this opportunity became evident during the debate over Captive Non-Public Networks (CNPNs), where large enterprises sought direct access to spectrum for private networks. Telecom operators strongly opposed the move because it threatened to bypass them in what could become one of the most profitable segments of the 5G value chain.

The reason is straightforward. Enterprise customers are not merely purchasing connectivity; they are investing in automation, productivity, and digital transformation.

Airtel has already demonstrated healthcare-focused use cases, including connected ambulance and telemedicine initiatives. Jio has pursued industrial deployments across sectors such as manufacturing, logistics, and ports. These projects extend far beyond traditional telecom services and increasingly resemble technology infrastructure contracts.

More importantly, the battle is no longer about telecom spending alone. Operators are competing for a share of enterprise cloud budgets, cybersecurity spending, IoT deployments, edge computing investments, and AI infrastructure projects. The winner could gain access to a significantly larger addressable market than connectivity revenue alone.

The Internet of Things Could Create Millions of New Connections

Another significant opportunity lies in the expansion of the Internet of Things (IoT).

The previous generation of mobile networks primarily connected people. 5G is designed to connect machines.

Smart electricity meters, water meters, connected vehicles, industrial sensors, agricultural equipment, smart streetlights, logistics assets, and surveillance systems all require continuous connectivity. Individually, these devices generate small amounts of revenue. Collectively, they represent a massive recurring revenue opportunity.

India’s machine-to-machine connection base has already reached tens of millions of devices and continues to expand rapidly. As government initiatives around smart cities, infrastructure modernisation, and digital governance accelerate, connected-device deployments are expected to increase substantially.

For Airtel and Jio, the attractiveness of IoT lies in its predictability. Unlike consumer customers who frequently change plans or switch operators, enterprise IoT deployments often remain active for years, creating sticky and recurring revenue streams.

In effect, telecom companies gain access to a subscription business built around machines rather than people.

Cloud, Edge Computing, and AI Could Redefine the Telecom Business Model

The most underappreciated aspect of 5G commercialisation is its potential to transform telecom operators into digital infrastructure companies.

Emerging technologies such as artificial intelligence, augmented reality, cloud gaming, autonomous systems, and industrial automation require computing resources located closer to end users. Processing data in distant data centres can create latency that limits performance.

This is where edge computing becomes critical.

By combining 5G networks with distributed computing infrastructure, Airtel and Jio can offer cloud services, edge computing platforms, cybersecurity solutions, AI infrastructure, and managed enterprise services.

The economics are attractive because these services typically command significantly higher margins than traditional connectivity offerings. Global telecom operators increasingly view cloud and digital infrastructure as future growth engines, and Indian operators are moving in the same direction.

Jio’s broader ecosystem strategy already spans cloud services, digital platforms, content, commerce, and artificial intelligence. Airtel has similarly expanded its enterprise portfolio through cloud, cybersecurity, and digital transformation offerings.

As AI adoption accelerates across industries, telecom operators may find themselves competing not only with other telecom companies but also within the broader digital infrastructure market.

The 5G Monetization Playbook

To evaluate how these moving parts stack up financially, telecom operators must balance immediate execution speeds against long-term profit generation:

| Revenue Stream | Growth Velocity | Margin Profile | Primary Structural Risk / Friction |

| Fixed Wireless (FWA) | Extremely High | Medium (Near-term) | Heavy upfront CPE device subsidies (₹4K–5K) dragging down immediate cash flows. |

| Enterprise Private 5G | Medium | Exceptionally High | Long corporate sales cycles and complex network integration across diverse industries. |

| Mass IoT & M2M | High | Medium | Low standalone ARPU per device; requires massive deployment volumes to move the revenue needle. |

| Cloud, Edge, & AI Infrastructure | Medium | High | Intense infrastructure competition from established global hyperscalers. |

The ₹300 ARPU Question That Will Define 5G Returns

For all the excitement surrounding enterprise 5G and AI infrastructure, the simplest measure of monetisation remains Average Revenue Per User (ARPU).

Bharti Airtel ended FY26 with an industry-leading ARPU of ₹257, while Reliance Jio reported ARPU of ₹214 across a subscriber base exceeding 524 million users. The gap reflects Airtel’s premiumisation strategy and stronger focus on high-value customers, while Jio continues to prioritise scale and market share.

Despite recent tariff increases, industry ARPUs remain well below the levels many analysts consider necessary for sustainable 5G returns. A commonly cited benchmark is ₹300 ARPU, which would provide significantly greater operating leverage against the enormous capital invested in spectrum and network infrastructure.

The mathematics are compelling. Every ₹10 increase in ARPU across hundreds of millions of subscribers can generate thousands of crores in additional annual revenue. As a result, tariff hikes, premium plans, broadband bundles, and enterprise services are not merely growth initiatives; they are critical components of the industry’s path toward acceptable returns on invested capital.

Early Scorecard: Who is Winning the Monetisation Race?

At this stage, Airtel appears to be winning on profitability, while Jio is winning on scale.

Airtel’s higher ARPU, stronger free-cash-flow profile, and disciplined capital allocation suggest that it is extracting more value from each subscriber. Jio, meanwhile, has built the industry’s largest 5G user base, broadband footprint, and Standalone network architecture, positioning it to capture a disproportionate share of future enterprise and digital infrastructure opportunities.

The market is therefore witnessing two different monetisation models. Airtel is maximising returns from its existing customer base, whereas Jio is building a broader digital ecosystem that could generate larger long-term revenue streams if enterprise adoption accelerates.

The next three to five years will reveal whether scale or capital efficiency proves to be the more successful strategy.

The Real Test: Can 5G Earn More Than Its Cost of Capital

The ultimate measure of 5G success is not network coverage or subscriber growth, but whether Airtel and Jio can generate returns that exceed their cost of capital.

The challenge is significant. In the 2022 spectrum auction alone, Reliance Jio spent nearly ₹88,000 crore, while Bharti Airtel invested over ₹43,000 crore. This was followed by billions of rupees in additional spending on towers, fibre networks, data centres, and 5G equipment. Such large investments require sustained revenue growth and margin expansion to generate attractive returns.

This is why operators are increasingly focusing on higher-margin opportunities such as Fixed Wireless Access, private enterprise networks, IoT, cloud services, and AI infrastructure. At the same time, improving ARPU remains critical. Airtel ended FY26 with an industry-leading ARPU of ₹257, while Jio reported ₹214. However, many analysts believe industry ARPU must move closer to ₹300 to fully support long-term 5G monetisation.

Ultimately, the winner of India’s 5G race will not be the company with the largest network, but the one that generates the highest return on its investment and converts 5G infrastructure into sustainable profit growth.

Conclusion

India’s 5G rollout phase is largely complete. The next challenge is monetisation. While both Airtel and Jio are pursuing opportunities across broadband, enterprise networks, IoT, cloud services, and AI infrastructure, they are taking different paths to get there. Jio is leveraging its scale and standalone architecture to build a broader digital ecosystem, while Airtel is focusing on capital efficiency, premiumisation, and stronger cash flow generation.

The success of 5G will ultimately not be measured by subscriber additions, coverage maps, or download speeds. It will be determined by how effectively operators convert billions of rupees of network investments into sustainable revenue growth and attractive returns on capital. The company that monetises its 5G infrastructure most efficiently, not necessarily the one with the largest network will be best positioned to create long-term shareholder value in India’s next phase of digital growth.