How CCL Products Make Money? – Business Model Explained

Coffee is one of the most consumed commodities in the world. Yet most investors rarely think about how it moves from farms to supermarket shelves.

Between raw coffee beans grown in tropical regions and branded coffee jars sold in retail stores sits a powerful layer of industrial processors. These companies make the transformation possible.

CCL Products (India) Ltd. is one of them. Understanding CCL’s business model is less about coffee as a product and more about value creation through commodity processing, global trade, and manufacturing efficiency.

The Wrong Way Most People Understand CCL

Most investors misread CCL Products as a simple FMCG coffee company. That framing misses the actual nature of the business.

CCL does not compete in retail branding or consumer recall. It operates deeper in the value chain as a large-scale processor of coffee beans into industrial-grade instant coffee, supplying global FMCG companies and private labels that ultimately sell to consumers.

In reality, it is not a consumer business. It is a B2B manufacturing export platform sitting inside a global commodity supply chain.

The Core Business: Converting Coffee, Not Selling Brands

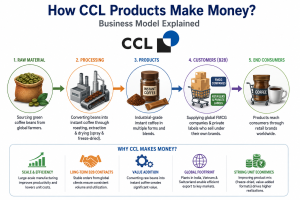

The entire business model begins with a simple flow. CCL buys raw green coffee beans, processes them into instant coffee, and supplies them to global buyers who sell it under their own brands.

This immediately removes branding from the equation. The company earns not from consumer demand creation, but from industrial conversion at scale.

The business is broadly divided into two product categories: spray-dried instant coffee, which drives volume and efficiency, and freeze-dried instant coffee, which sits at the premium end with stronger margins. Over time, the increasing contribution of freeze-dried coffee has become an important driver of profitability, even if spray-dried remains the backbone of scale.

Product Portfolio: A Wide but Industrial-Grade Coffee Mix

CCL Products (India) Ltd. operates across a surprisingly broad coffee portfolio, but the structure is more industrial than consumer-driven.

Its core offerings include:

- Spray dried coffee powder and granules

- Freeze dried coffee

- Freeze-concentrated liquid coffee

- Roast & ground coffee

- Roasted beans

- Premix coffee

- Decaffeinated variants

While this looks like a diversified consumer portfolio on paper, the underlying logic is different, the company is not building retail brands across all these categories, but rather offering a wide input-output manufacturing capability for global clients.

Over time, its internal “blend library” has expanded significantly, moving from roughly 500-600 blends in FY15-20 to nearly 1,000 blends by FY25. This expansion reflects increasing customization demand from global private label clients rather than traditional product innovation in the FMCG sense.

Private Label Manufacturing

A significant portion of CCL’s revenue comes from private label contracts. Global FMCG companies and retailers outsource production entirely to the company.

Under this model, CCL manufactures coffee under client-owned brands while customers manage marketing and distribution. This changes the economics of the business in a fundamental way.

The arrangement allows CCL to operate at scale without spending heavily on brand building.

However, large institutional buyers still hold significant bargaining power during pricing negotiations. The company’s advantage lies in consistent volumes and high capacity utilization rather than pricing control.

Brand Presence: Selective, Not Central to the Model

Unlike typical FMCG companies, CCL’s branding is limited and highly focused. The company operates under the “Continental” umbrella in select markets, but branding is not the core value driver.

Its key brand extensions include Continental Xtra and Continental Speciale in spray dried instant coffee, Continental THIS in the 3-in-1 premix category, Continental Black Edition / Premium in freeze dried coffee, and Continental Malgudi in roast & ground coffee.

However, these brands represent a small portion of the overall business. They function more as strategic retail touchpoints rather than the primary revenue engine, which continues to be dominated by private label manufacturing for global clients.

Global Manufacturing Footprint and Export Logic

CCL’s manufacturing base across India and international locations serves as more than an expansion strategy. It is a supply-chain advantage.

CCL positions its facilities close to key consumption markets such as Europe and North America. This helps the company serve large export clients efficiently. It reduces logistical friction, improves delivery timelines, and strengthens its ability to win large institutional contracts.

The business is therefore not India-centric. It operates as a global export-oriented coffee processor.

Manufacturing Footprint: A Multi-Country Export Infrastructure

The operating strength of CCL lies in its manufacturing scale and geographic distribution. The company operates four key production facilities across India, Vietnam, and Switzerland. Each facility plays a specific role in the global supply chain.

In India, CCL operates its Duggirala plant, which became the country’s first freeze-dried instant coffee facility in 2005. It also operates a newer freeze-dried unit at Kuvvakolli, Andhra Pradesh. Management built this facility with significant headroom and expects it to double capacity over time.

Internationally, Continental Coffee S.A. in Switzerland focuses on agglomeration and packaging activities. The Ngon Coffee plant in Vietnam, located in Dak Lak province, anchors the company’s presence in Southeast Asia.

This structure is not random expansion. It is a deliberate export-oriented manufacturing network. The company stays close to both coffee-producing regions and major consumption markets.

Why CCL is not a Typical FMCG Company?

Unlike traditional FMCG players, CCL does not rely on brand equity or consumer loyalty as its primary moat.

Its strength lies in operational capability: large-scale manufacturing, consistent quality, and long-term contracts with global buyers. The presence of a retail-facing brand is secondary and does not define earnings.

This makes CCL closer to an industrial export manufacturer than a consumer brand company, despite operating in a consumption-driven category.

The Real Economics: De-Risking the Commodity Cycle

CCL Products (India) Ltd. operates on a cost-plus model in its B2B business. The company largely passes raw coffee costs through to customers once it locks in orders. This structure insulates the business from short-term commodity price volatility.

The key unit metric is EBITDA per kg. It remains broadly stable at around ₹135-₹140 per kg, even during volatile coffee cycles. During periods of high coffee prices, profitability per unit remains largely unchanged. Instead, reported margins appear compressed. For example, margins may decline from around 18% to 15-16% because higher coffee costs increase pass-through revenues.

The main pressure point is working capital. Higher coffee prices increase the cash required to fund inventory and receivables for the same sales volume. As a result, short-term borrowings often rise during inflationary cycles.

Growth Runway: Capacity Expansion and Mix Shift

CCL is moving into a phase of utilization-led growth after a significant capacity build-up across India and Vietnam. With blended utilization of roughly 65-70%, the company has clear room to increase volumes without proportional capital expenditure. This opportunity becomes more meaningful as newer Vietnam capacities continue to ramp up.

Product mix improvement is also driving growth. The company is steadily shifting toward freeze-dried coffee. This premium category generates materially higher realizations than spray-dried products. At the same time, CCL is increasing its presence in small-pack and value-added formats. This allows the company to capture more downstream value without taking on the full costs of consumer brand building.

Key Risks

Despite structural strengths, the model remains exposed to external risks. Global freight volatility can impact competitiveness in export markets, even under FOB contracts, if sustained cost differences alter sourcing preferences.

Extreme weather events in key coffee-producing regions can also disrupt raw material availability, leading to lower utilisation and pressure on fixed-cost absorption.

Finally, the company’s domestic B2C push under the Continental brand introduces a different risk profile altogether, requiring higher marketing intensity and distribution spending, with uncertain return on capital compared to its core B2B model.

Conclusion

CCL Products (India) Ltd. is not a consumer-facing coffee brand. It is a processing-led export business sitting in the middle of the global coffee value chain, converting raw beans into instant coffee for FMCG companies and private labels.

Its strength lies in scale, efficiency, and long-term institutional contracts rather than branding or retail presence. This makes revenues relatively stable, but earnings remain cyclical due to coffee price movements, currency shifts, and product mix changes.

In the end, CCL is a business that wins by being embedded in the system, not by being visible in it.