The Hidden US Estate Tax: The Wealth Destroyer Most Indian Investors Don’t Know About

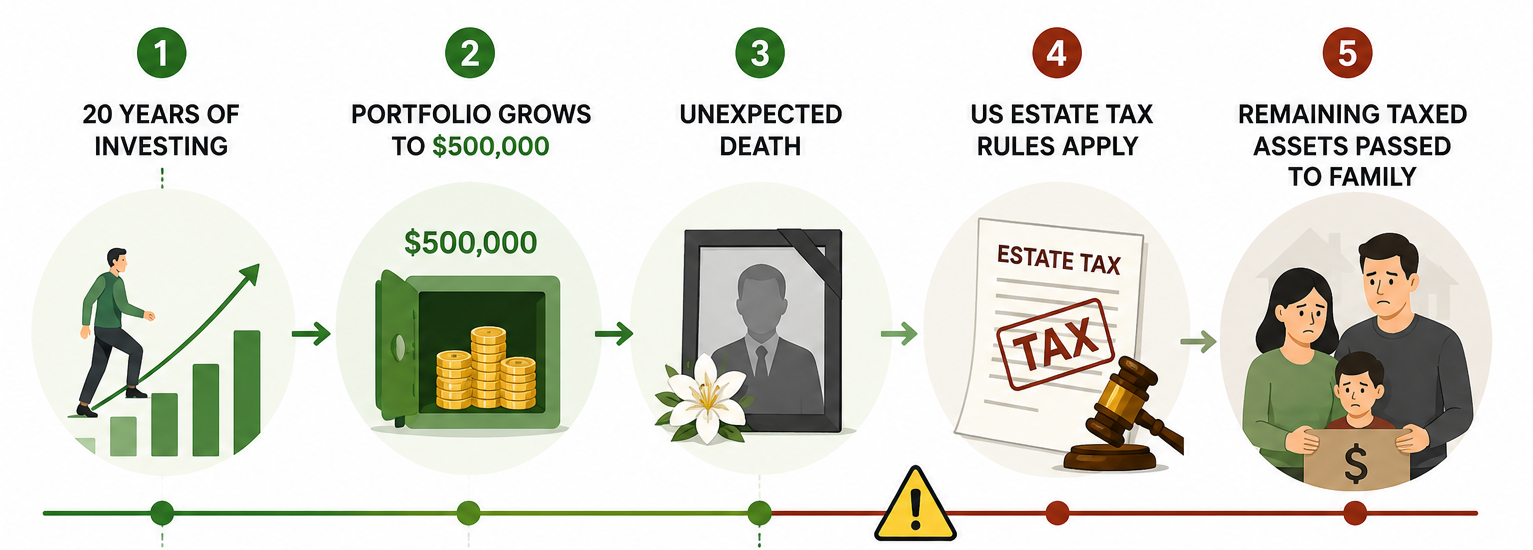

Imagine you've spent the last 20 years building your dream investment portfolio.

You invested consistently in some of the world's best companies - Apple, Microsoft, Nvidia, Amazon, and Alphabet. Your patience paid off, and your portfolio is now worth $500,000.

Everything went according to plan.

Until something completely unexpected happened.

After your passing, your family expects to inherit your investments just as they would inherit property or bank deposits in India.

Instead, they discover that before the assets can be transferred, the US Government may have a claim on part of your portfolio.

Not because you sold your investments.

Not because you earned a profit.

But simply because you owned certain US assets when you passed away.

This is known as the US Estate Tax—one of the least understood risks for Indian investors building international portfolios.

As investing in US stocks becomes easier through platforms like Interactive Brokers, Vested, INDmoney, and others, thousands of Indians are unknowingly increasing their exposure to this rule. While investors spend countless hours researching the next multibagger, very few spend time understanding how those investments will eventually be passed on to their family.

And that could prove to be an expensive mistake.

What Exactly Is the US Estate Tax?

Many investors confuse Estate Tax with Capital Gains Tax or Inheritance Tax, but they are completely different.

The US Estate Tax is a federal tax imposed on the transfer of certain assets after a person's death. Instead of taxing the profit earned on an investment, it taxes the value of the estate that is being transferred to heirs.

This is an important distinction.

Suppose you purchased shares of Apple for $50,000, and over time those shares grew to $400,000.

If Estate Tax becomes applicable, the calculation is based on the current market value of $400,000, not the original purchase price or the profit earned.

In other words, Estate Tax looks at what the assets are worth at the time of death, not how much money you made from investing.

For Indian investors who primarily think in terms of capital gains tax, this difference often comes as a surprise.

Why Should Indian Investors Care?

For many years, investing directly in US stocks was limited to wealthy individuals.

Today, that has changed dramatically.

Indian investors can easily buy fractional shares of companies like Apple, Tesla, Microsoft, Amazon, and Nvidia with just a few clicks. As a result, overseas investing has become a core part of many long-term portfolios.

However, this growing trend also means more investors are exposed to US Estate Tax without realizing it.

The biggest reason is that US tax laws treat non-US residents differently from US citizens and residents.

While US citizens and individuals considered domiciled in the United States benefit from a very large lifetime estate tax exemption (approximately $15 million per person in 2026, subject to annual inflation adjustments), most non-resident, non-US citizens (NRNCs) receive an exemption equivalent to only $60,000 of US-situs assets.

This difference is enormous.

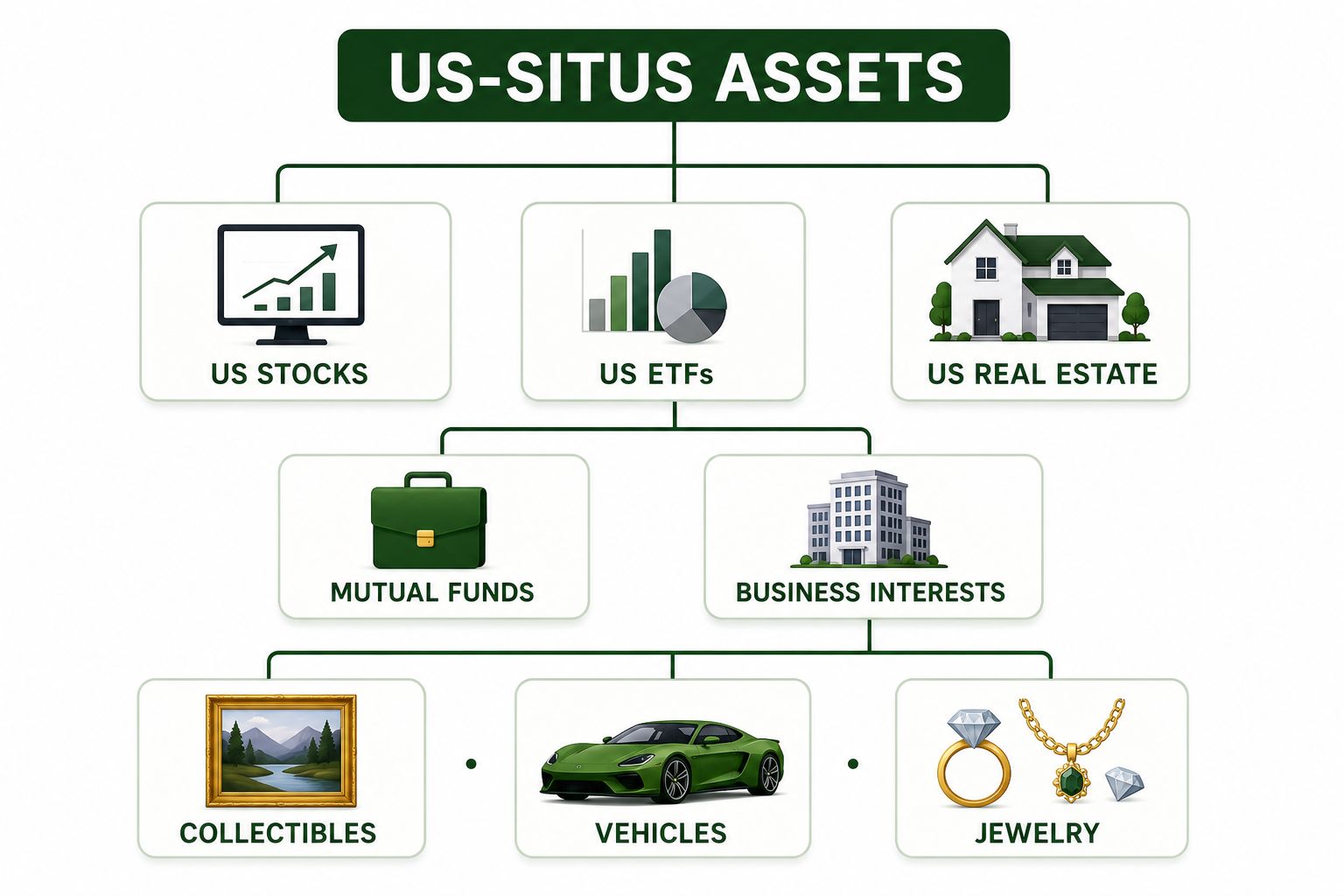

Which Assets Can Be Covered?

The US Estate Tax generally applies to US-situs assets - assets that are considered to have a legal connection and are located in the United States. While many Indian investors only think about US stocks, the scope is much broader.

Depending on the circumstances, examples of US-situs assets can include:

- Shares of US-listed companies (such as Apple, Microsoft, Nvidia, Amazon, Tesla, etc.)

- US-listed Exchange Traded Funds (ETFs)

- Certain US mutual funds

- Real estate located in the United States

- Interests in certain US-based businesses or partnerships

- Tangible personal property located in the US

For most Indian investors, directly held US stocks and US-listed ETFs are the most common assets that may create estate tax exposure. However, investors with property, businesses, or other assets in the United States should also understand how these rules may apply to their overall estate.

It's also important to remember that where an investment is legally domiciled matters more than the companies it invests in. For example, many Irish-domiciled UCITS ETFs invest in Apple, Microsoft, and Nvidia while generally avoiding classification as US-situs assets. This structure makes them a popular choice for international investors seeking to reduce US estate tax exposure.

A Common Misconception That Can Cost Families Dearly

One of the biggest misconceptions among Indian investors is:

"I live in India, so US tax laws don't apply to me."

Unfortunately, that's not how Estate Tax works.

Estate Tax is based primarily on the location and legal nature of the assets, not simply on where the investor lives.

If you directly own qualifying US-situs assets, those assets may become subject to US estate tax rules upon your death—even if you have never lived in the United States.

This is why estate planning is a crucial part of international investing.

Choosing the right investment structure can sometimes be just as important as choosing the right stock.

What Can Indian Investors Do to Reduce US Estate Tax Exposure?

The purpose of understanding US Estate Tax isn't to discourage international investing.

The United States is home to many of the world's largest companies, making international diversification important for long-term wealth creation.

The goal is to structure investments efficiently, so your family avoids unnecessary tax and legal complications.

Every investor's situation is different, but several widely used strategies can help reduce potential estate tax exposure.

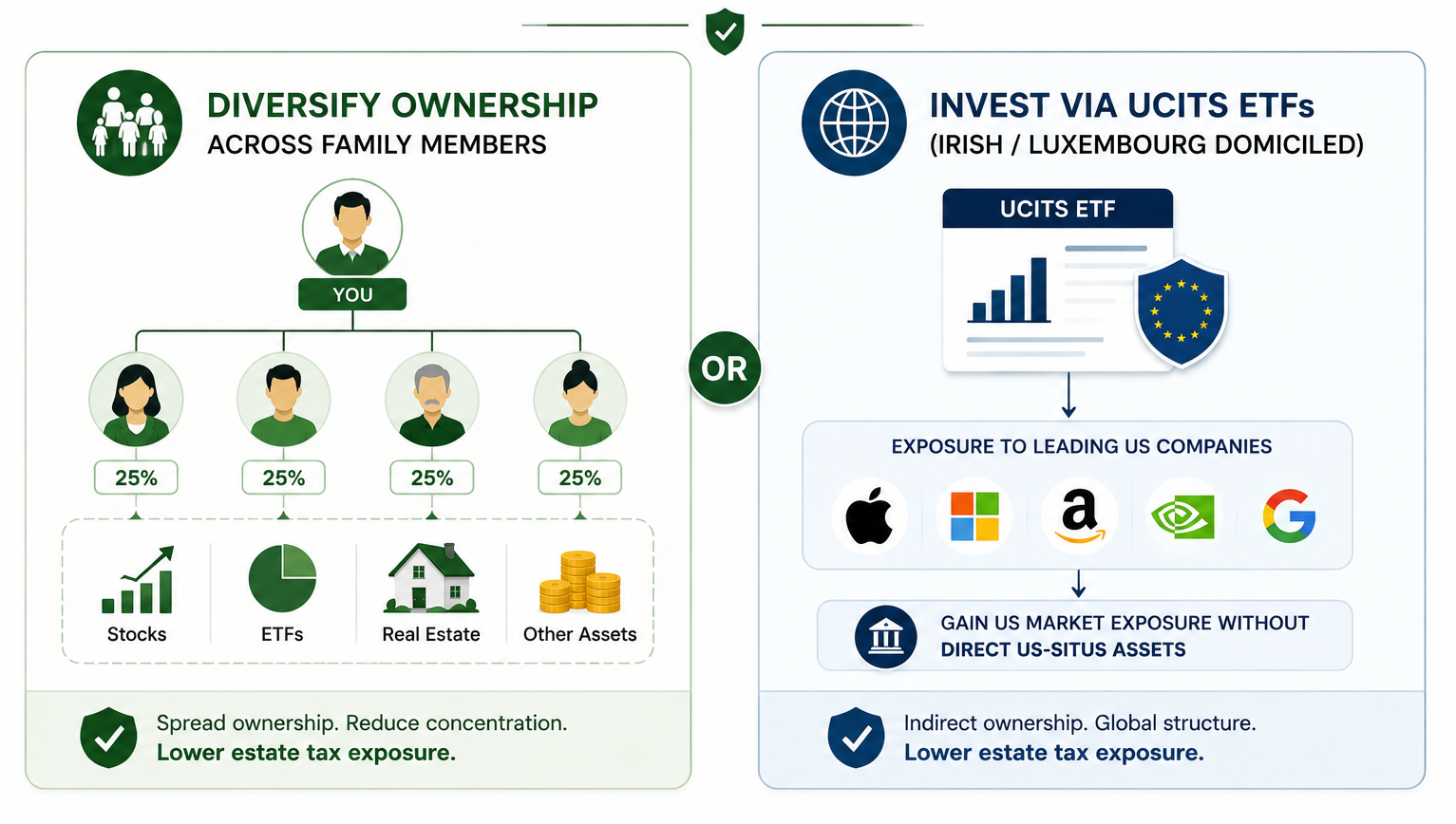

1. Diversify Investments Across Family Members

One of the simplest ways to reduce concentration is to spread investments among different eligible family members instead of holding the entire US portfolio in a single person's name.

For example, under India's Liberalised Remittance Scheme (LRS), each resident individual has an annual remittance limit of USD 250,000.

Each adult family member can invest through their own account, creating separate portfolios instead of concentrating US assets under one person.

This also uses each member's LRS limit and may reduce estate tax exposure, as each person legally owns their assets.

However, ownership should always reflect genuine investment and legal ownership. Simply adding someone's name without proper ownership or documentation may not achieve the intended outcome.

2. Consider Investing Through Non-US Domiciled Funds

Another widely discussed strategy is to gain exposure to US companies without directly owning US-situs securities.

One of the most popular ways of doing this is through UCITS ETFs.

Although these funds invest in Apple, Microsoft, Nvidia, Amazon, and Alphabet, investors own units of a European fund, not US-listed securities.

As a result, these investments generally fall outside the definition of US-situs assets, attracting investors who want to reduce their exposure to US estate tax.

- Lower expense ratios than many Indian feeder funds.

- Better global liquidity due to a larger international investor base.

- Potentially more efficient dividend withholding structures through Ireland's tax treaty with the United States.

- Lower tracking error in many widely followed index funds.

However, investors should evaluate factors such as taxation in their country of residence, brokerage access, fund size, and overall investment objectives.

Conclusion

For most investors, building wealth is the primary goal. They carefully select quality companies, stay invested for decades, and focus on maximizing long-term returns.

But preserving that wealth for the next generation is equally important.

The US Estate Tax often goes unnoticed because it applies after death, not during your lifetime.

It can affect your heirs when they're already facing emotional and legal challenges.

Fortunately, awareness is the first step toward better planning.

Diversifying ownership, using UCITS ETFs, or planning your estate early can simplify future wealth transfer.

The goal isn't to avoid US companies. It's to invest while minimizing avoidable estate tax risks.

As international investing becomes increasingly popular among Indian investors, understanding how to build wealth is no longer enough.

Understanding how to protect and transfer that wealth may be just as important.