Kaynes Technologies – Order book Structure Explained

When investors study a manufacturing company, one of the most important things they look at is the order book. Revenue and profits tell us what the company has already achieved in the past, but the order book gives an idea about the company’s future business visibility.

This becomes even more important in the case of companies like Kaynes Technologies, which operate in the Electronics System Design and Manufacturing (ESDM) industry. The company manufactures electronic systems and provides design-led manufacturing solutions for industries such as automotive, railways, aerospace, defence, industrial automation, medical devices, and electric vehicles. Since these industries generally work on long project cycles and customised manufacturing requirements, the order book becomes a critical metric for evaluating business strength.

But understanding the order book is not only about looking at one large number. Investors need to understand where the orders are coming from, which sectors are growing faster, how much of the business is recurring, and whether the company can execute these projects efficiently. This is where the structure of Kaynes Technologies’ order book becomes important.

Order book Size

An order book is the total value of orders a company has received but has not yet completed. One of the strongest indicators of business visibility for Kaynes Technologies is its growing order book

The order book has shown strong and consistent growth over the past few quarters. This growth is largely driven by rising electronics demand across industries in India.

| Period | Order book (₹ Cr) |

| Q3 FY25 | 6,047 |

| Q4 FY25 | 6,596 |

| Q1 FY26 | 7,401 |

| Q2 FY26 | 8,994 |

| Q3 FY26 | 9,072 |

| Q4 FY26 | 8,366 |

The table shows how the order book of Kaynes Technology India Limited has grown over the last few quarters. This is one of the most important indicators for investors because the order book reflects future business visibility.

The order book increased from ₹6,047 Cr in Q3 FY25 to ₹9,072 Cr in Q3 FY26.

This represents nearly a 50% YoY growth, which indicates strong demand across the company’s business verticals.

However, in Q4 FY26, the order book declined slightly to ₹8,366 cr from ₹9,072 cr in the previous quarter.

From the above table, we can conclude that the company continuously received new orders across industries such as industrial electronics, automotive & EV, railways, aerospace and defence.

The rising trend suggests that demand for electronics manufacturing and system design services remains strong.

Although the order book showed strong long-term growth, the company witnessed a slight sequential decline in Q4 FY26.

Why Did the Order Book Decline in Q4 FY26?

The decline in Kaynes Technologies' order book during Q4 FY26 was mainly due to order execution. The company converted a large portion of its existing orders into revenue through faster manufacturing and deliveries.

In manufacturing businesses, a declining order book does not always signal weak demand. It can also indicate strong execution capabilities and efficient conversion of orders into revenue.

Composition by Segment & Vertical

Let us now examine the sources of the company's orders and revenue. This includes the industries it serves and the business segments it operates in.

Investors closely analyse this because growth rates vary across industries. Profit margins also differ from one business segment to another. So, by studying the composition, investors try to understand how strong the business is and whether future growth is sustainable.

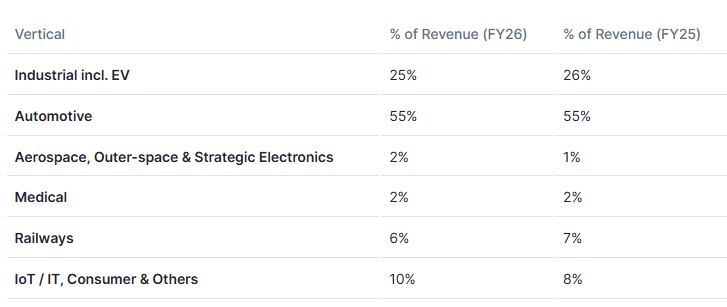

Revenue Vertical Mix (FY26)

The revenue vertical mix shows the industries from which Kaynes generates its revenue. Here we can see that more than half of Kaynes’ revenue comes from automotive electronics. This indicates that the company has a strong position in fast-growing automotive electronics. The stable contribution over both years also suggests consistent demand and long-term customer relationships. The table also mentions Industrial incl. EV which indicates that the company has exposure to electric vehicle ecosystem growth and that's the reason why this has become a positive sign for future demand visibility.

But on the other side we can conclude that Kaynes is heavily dependent on automotive demand. If EV growth slows or vehicle production weakens, demand from the automotive sector will decline and therefore Kaynes revenue can get affected.

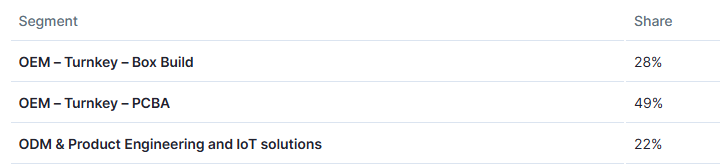

Revenue by business model (FY26)

The management has confirmed that about 20% of the order book contains ODM products. Which means 20% of the total order book consists of design led products, smart metering solutions and Engineering-led ODM products. And also the management has confirmed that this number is increasing and it can go up by 5 to 7 percentage points which three major means the ODM order book can potentially rise towards 25% to 27%.

ODM orders are generally high margin, more technology intensive and stickier which can improve the order book quality.

OSAT (Outsourced Semiconductor Assembly and Testing) & PCB (Printed Circuit Board) order book – New Growth Engines

OSAT (Outsourced Semiconductor Assembly and Testing)

An OSAT is the process where semiconductor chips are packaged and tested before use.

>The semiconductor chips cannot be directly used, so OSAT companies connect them electrically and test whether they work properly or not.

The OSAT business of Kaynes Technology India Limited is gradually emerging as a major long-term growth opportunity for the company.

Management highlighted that the business already has revenue visibility of over ₹2,500 crore over the next five years this indicates strong future demand and customer confidence.

The company has already secured three major anchor customers — Alpha & Omega Semiconductor (AOS), Infineon, and L&T Semiconductor through the Fujitsu acquisition — which significantly strengthens the credibility and commercial viability of the OSAT business. Additionally, around 60% of the company’s OSAT capacity has already been committed by large players. Management has guided for OSAT revenues of approximately ₹250–300 crore in FY27.

Management clarified that the OSAT business will initially be export-oriented. Domestic revenue contribution will be minimal in the early stages. The company will primarily serve international markets during the initial phase of operations.

PCB (Printed Circuit Board)

PCB is the green board inside electronic devices on which all electronic components are placed and connected. It acts like a pathway through which electricity and signals travel. Without PCB electronic components cannot communicate with each other.

The PCB business of Kaynes Technology India Limited is also witnessing strong long-term demand visibility, with management highlighting a robust and confirmed demand pipeline for the next five years.

Multiple customers have already indicated the requirement for additional capacity, reflecting strong market interest even before full-scale operations begin. The company has guided for PCB revenues of around ₹300–400 crore in FY27, while the PCB manufacturing facility is expected to become operational by July 2026.

Management also stated that customer traction is already strong, with interest coming from more than 16 customers. One of the most important strategic aspects of the PCB business is the PCB-to-PCBA multiplier effect, where every ₹1 of PCB revenue can potentially generate nearly ₹9 of EMS (PCBA) revenue for the group.

Based on current investments and demand trends, management estimates a business opportunity of nearly ₹15,000 crore across the EMS ecosystem.

Execution Timeline – How Fast Does the order book Convert?

Execution time refers to the period a company takes to convert an order into revenue. After receiving an order, the company must manufacture, deliver, install, and complete the project before recognizing revenue.

Kaynes Technologies' order book currently provides around 1.5 years of revenue visibility. Most orders are executed within 6–18 months. However, large projects in railways, aerospace, and industrial electronics can take up to 5 years due to customer deployment schedules and approval processes.

Management stated that most orders are non-cancelable because Kaynes manufactures highly customized products. The company designs products such as automotive control systems and railway signalling modules for specific customers, making them difficult to sell elsewhere.

In FY25, Kaynes generated nearly ₹2,721 crore in revenue through order execution. At the same time, monthly order inflows continued to grow by around 11–12% sequentially every quarter, indicating healthy demand.

However, execution remained below earlier expectations due to temporary external factors. The West Asia conflict disrupted supply chains and delayed customer production schedules. In addition, a large EV OEM customer reduced order volumes by nearly 90% from original projections, affecting near-term execution.

Government projects also faced delays because approval and deployment processes took longer than expected. Management noted that over 50% of certain project-related activities remained in the pipeline and were delayed rather than cancelled. Railway Kavach orders were also pushed into Q1 and Q2 FY27 due to product revisions and regulatory approvals.

As a result, the company faced an execution shortfall of around 20% compared to planned levels. However, management emphasized that these were mainly delays in revenue recognition, not order cancellations. The company retains such orders in its order book and recognizes revenue once customers complete deployment and approval requirements.

Order Book Quality & Customer Concentration

While analysing Kaynes Technologies, investors should focus not only on the size of the order book but also on its quality, diversification, and customer concentration. A large order book creates value only when it is diversified, executable, and supported by long-term customer relationships.

Management has consistently described the order book as healthy, diversified, and largely non-cancelable. It has also stated that demand, customer relevance, and order quality remain strong.

Customer concentration appears manageable. The largest customer contributes less than 6% of revenue, reducing dependence on any single client. However, the top 5 customers account for around 46% of revenue, the top 10 contribute nearly 60%, and the top 20 contribute about 76%. This reflects a mix of diversification and strong relationships with large strategic customers.

Such concentration is common in the EMS industry, where major OEMs place large, long-term orders. These customers tend to remain sticky because electronic systems in sectors such as automotive, railways, aerospace, industrial automation, and medical devices require extensive testing, qualification, and engineering support before deployment.

Kaynes serves over 300 active customers across more than 30 countries and maintains average customer relationships of 7–10 years. Once customers integrate Kaynes' products into their systems, switching suppliers becomes costly and time-consuming, strengthening customer retention.

Another key strength is the customized nature of the company's products. Kaynes designs solutions such as automotive ECUs, railway signalling systems, aerospace electronics, and industrial controllers for specific customer requirements. Since these products cannot be easily sold to other customers, order cancellations remain relatively low. Most disruptions arise from execution delays rather than order losses.

Overall, Kaynes Technologies has a high-quality order book supported by diversified customers, long-term relationships, strong customer stickiness, and customized non-cancelable orders.

Risks & Challenges to Order Book Execution

Even though the company has a strong order book, execution is not always smooth. Many external and internal factors can delay revenue recognition, impact cash flows, or reduce the expected growth from certain projects. Below are the major risks and challenges associated with the execution of the order book.

Geopolitical Disruptions

One of the key risks is geopolitical tensions, especially the West Asia conflict, which caused last-minute deferments during Q4 FY26. This means that even if customers had already placed orders, some projects were delayed because global uncertainty affected customer confidence, logistics, or shipment schedules.

For example, imagine a customer planning to launch a new industrial or EV-related product. Due to rising tensions in a region, they may postpone their expansion plans temporarily. As a result, the company’s delivery schedule and revenue recognition also get pushed forward.

So, the order is still there, but the timing of execution changes.

Customer Project Readiness

Another important challenge is customer project readiness. In many industries, especially electronics and industrial manufacturing, customers may not always be fully prepared to start production immediately. Sometimes their factories, approvals, software integration, or end-market demand are not ready on time.

Because of this, revenue recognition gets shifted to later quarters even though the order itself remains valid.

For example, a customer may place an order for smart meters or industrial electronics, but if their deployment site or installation infrastructure is incomplete, the company cannot recognize the revenue immediately.

This creates quarterly fluctuations in sales despite having a strong order book.

Government Project Cycles & Approval Delays

Government-linked projects also introduce execution risks. Factors such as state election model codes of conduct, slow approvals, tender delays, and administrative procedures can slow down project execution timelines.

For example, if a state government announces elections, many approvals and new spending decisions may temporarily pause until elections are completed. This directly impacts sectors like smart metering, infrastructure electronics, and public-sector projects.

So, even if the company has already won the order, actual implementation may take longer than expected.

Smart Metering Working Capital Pressure

One of the biggest financial challenges is the smart metering receivables issue. Around ₹1,365 crores is stuck in receivables, and management expects nearly three quarters for normalization.

This means the company has already supplied products or completed work but has not yet collected payments from customers.

As a result, the company faces working capital pressure. It locks up cash, reduces liquidity, and may force the company to borrow additional funds to run operations smoothly.

De-growth From a Large EV Customer

The company also faced a major setback from one EV customer whose projected volumes dropped by nearly 90%.

Even if the company has many customers, a sharp reduction from a large customer can impact - revenue growth, factory utilization, and future projections. This shows that future order expectations are not always guaranteed to convert into actual business volumes.

This is an example of customer concentration risk.

Supply Chain Disruptions

The company remains heavily dependent on imports for raw materials, with nearly 55–60% sourced from regions like - China, Singapore and Europe

This creates supply chain risks. Any disruption such as shipping delays, rising freight costs, trade restrictions, semiconductor shortages, or currency fluctuations can affect production schedules and margins.

OSAT & PCB Execution Risks

The company is also entering advanced areas like OSAT and PCB manufacturing, which come with execution challenges.

Key risks include - timely commissioning of plants, successful customer qualifications, technology stabilization and smooth subsidy disbursement.

In businesses like OSAT, customers usually conduct strict quality checks before giving large-scale commercial orders. Even a small delay in plant readiness or certification can postpone revenue generation.

Check Other Post Posts

-

How to do Swing Trading on Groww?

How to do Swing Trading on Groww?February 14, 2025

-

How to Check Sarva Haryana Gramin Bank Balance?

October 8, 2024

-

What is a Trading Account?

May 13, 2025