Varun Beverages Stock Analysis 2025: Full Breakdown

What’s common between Pepsi, Sting, Nimbuz and Creambell? They’re all tied to one silent FMCG giant that’s been powering India’s soft drink market - Varun Beverages Ltd. (VBL).

Once a lesser known bottler, VBL turned into a stock market superstar, delivering 1200% returns between 2020 and 2024. But now the stock has corrected. The big question is - Is this the calm before another rally or the start of a slowdown?

Let’s breakdown everything you must know about VBL in 10 simple and sharp points. Whether you're already invested or planning to enter, this is your one-stop guide to understanding the reality behind the hype.

Business Model

Image generated from - Gemini

Think of VBL as PepsiCo's secret weapon in India and beyond. While you're sipping that ice-cold Pepsi, VBL is the invisible force that made it, bottled it, and got it to your local store.

- Carbonated drinks (Pepsi, Mirinda, Mountain Dew) contribute 70-75% in its revenue.

- Packaged water contributes 15-20% in its revenue.

VBL barely touches PepsiCo's snack business - they only distribute Lays in three African countries.

Ever heard of Creambell? That's VBL trying to build its own empire. But it's not working. Even their four "popular" South African brands are basically rounding errors in the revenue game.

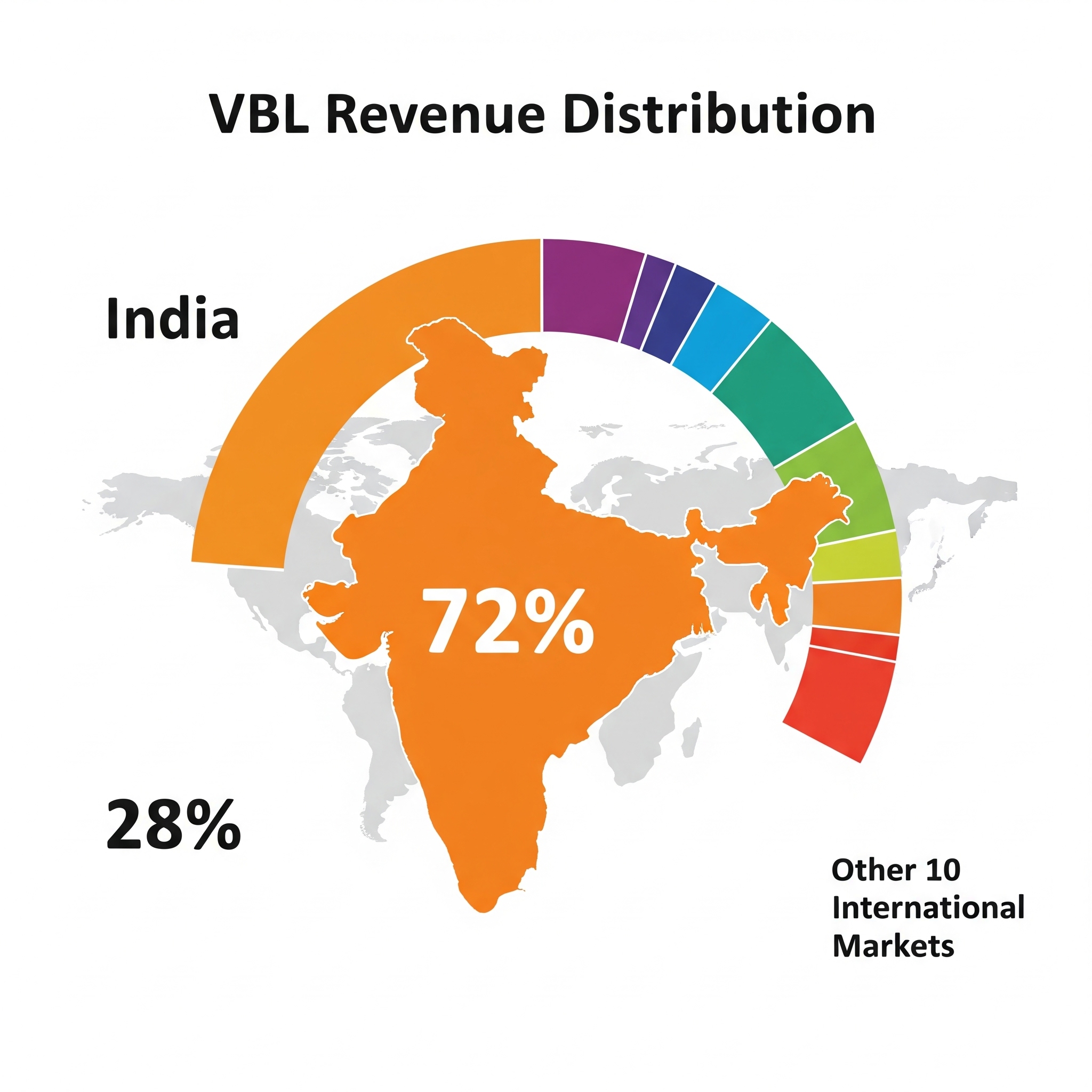

Global Presence

VBL operates in 10+ countries, but its revenue distribution tells us its real and interesting picture i.e. :

Image generated from -Gemini

- India is its biggest and important market that contributes almost 72% of VBL’s revenue.

- Other international markets i.e. in other 10 countries contribute the remaining 28% of its revenue.

International Highlights

- South Africa is the fastest-growing market for VBL with a 13% YoY volume growth.

- In Zimbabwe, VBL holds a leading market share.

- Plans to expand into Tazania and Ghana were recently scrapped due to regulatory hurdles.

International Profit Margins

The profit margins from overseas are significantly lower than India due to :

- Sugar Taxes, especially in Zimbabwe

- Currency fluctuations and inflation

- Costlier supply chains and Local market inefficiencies.

The Reason Behind its Stock’s Decline

If you invested in VBL during 2024, you’re likely facing 15–30% losses. But this drop isn’t due to weak fundamentals. Between April 2020 and June 2024, the stock skyrocketed 1200%, while revenue grew just 3–4x and profit about 6x.

Such a gap between price and actual business performance led to unsustainable valuations. Investor euphoria, social media buzz, and momentum buying pushed the stock far ahead of its fundamentals.

What we’re seeing now is a healthy valuation correction, not a red flag on the business, but a reset of expectations to more realistic levels.

Revenue and profit Growth

Now if we see VBL’s growth story, it is very impressive and also consistent.

Over the past decade, VBL’s sales have grown consistently every year except during COVID. In the last 5 years, it delivered 23% CAGR in sales and 41% CAGR in profit, hitting all-time high revenues and earnings.

Looking ahead, the management expects strong double-digit growth, with brokerages like Sharekhan and Motilal Oswal projecting 18% sales growth in FY25. The momentum in volumes and profitability remains robust.

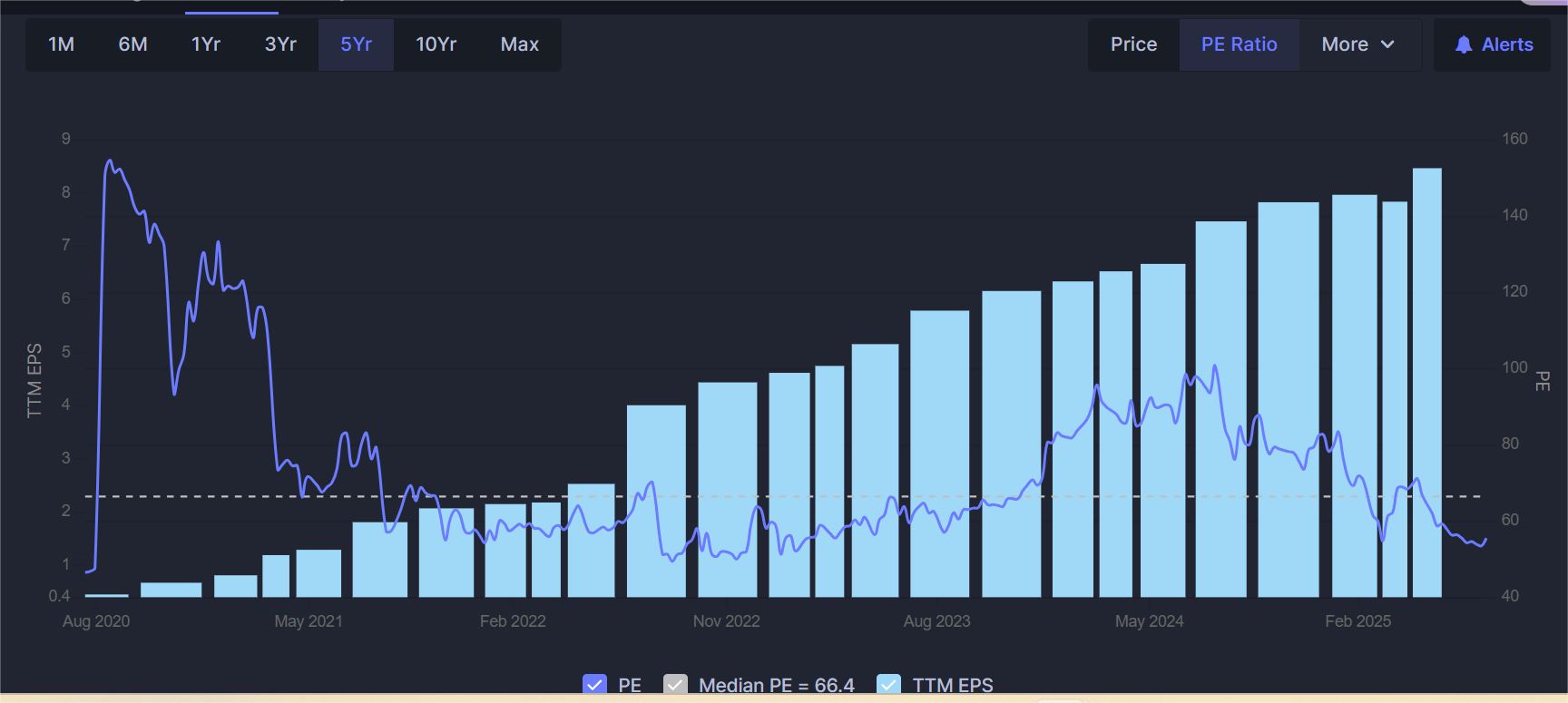

Valuation of Company

Now let’s understand VBL’s valuation requires historical context and careful analysis of its PE ratio trends :

Historical PE Analysis

Screenshot taken from - Screener

- During 2020 i.e. pre-COVID time, PE ratio was 51.

- In January 2024, PE reached its peak i.e. 100+, it clearly represents its unsustainability.

- In 2025, PE is 54 which is approximately at half of its peak level.

While historical performance doesn’t guarantee future results, the current PE of 54 suggests that VBL is dramatically overvalued by its own historical standards. However investors should consider multiple valuation metrics rather than relying solely on PE ratios for investment decisions.

Promoter’s Shareholding

Screenshot taken from Screener

A common concern among investors is the decline in promoter shareholding from 62% to 60%. On the surface, it may look like the promoters lost their confidence. But this drop is not actually due to promoter selling, But it's due to QIP (Qualified Institutional Placement).

QIP is a fundraising method where companies issue new shares to institutional investors (like FIIs and DIIs) to raise capital without going through a public offering.

VBL raised ₹7,500 crores through QIP in November 2024 by issuing 13 crore new shares, leading to 4% dilution in overall equity including promoter holding.

The funds were used to reduce debt ny nearly 50%, strengthening the company’s balance sheet. Despite the dilution, promoter holding remained healthy at 60%, indicating continued long-term commitment.

Watch Our Varun Beverages Stock Analysis Video

Technical Analysis

Looking at VBL’s technical charts reveals 2 distinct trendlines :

- Yellow Trendline represents historical data weighted which suggests 175% returns over 5 years which seems unlikely now.

- Blue Trendline represents recent correction weighted and it indicated 100% returns over 5 years which seems more realistic.

The blue trendline appears more realistic given VBL's current large-cap status (₹1.5 lakh crore market cap). A 100% return over 5 years translates to 15% CAGR, which aligns with Goldman Sachs' prediction of 22% returns over the next year.

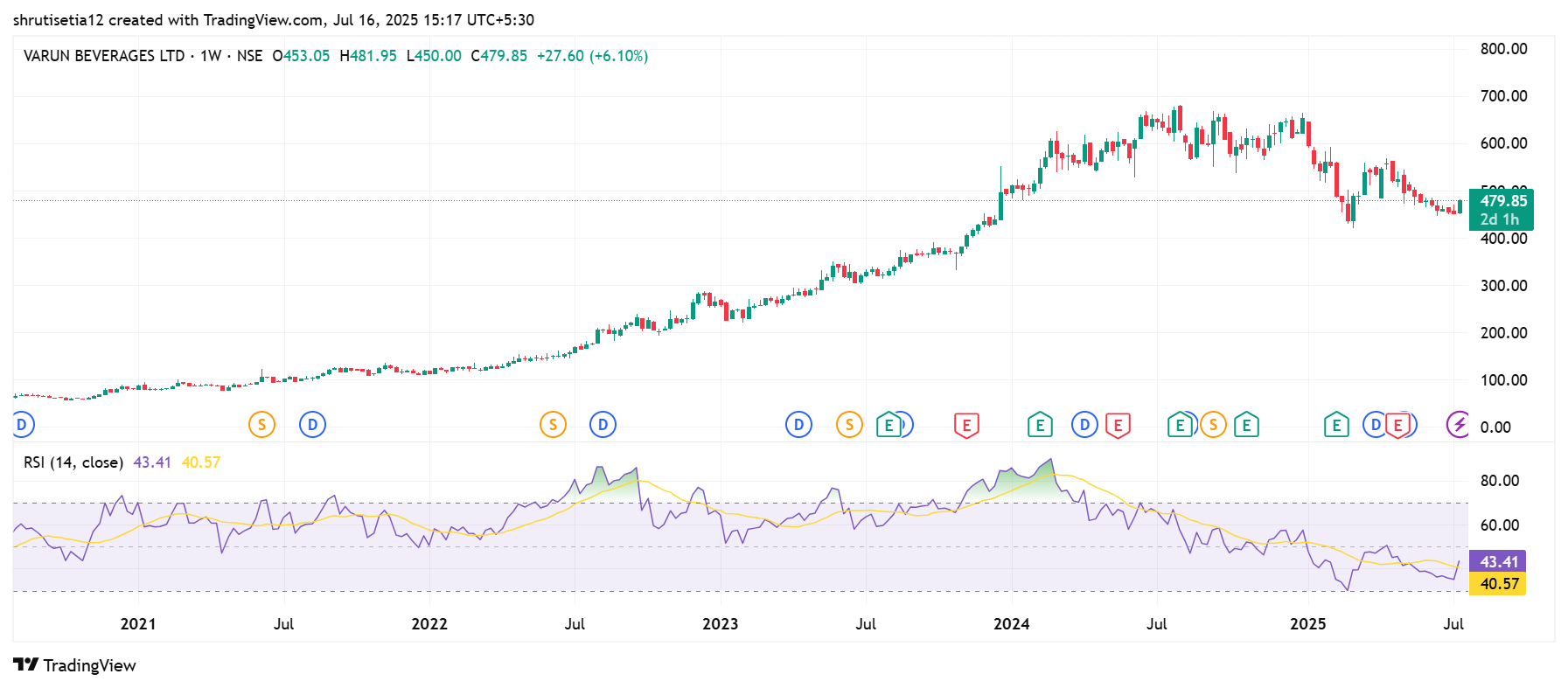

RSI Level - Is the Stock Oversold Now?

Screenshot taken from Trading View

For long-term investors, weekly RSI levels provide valuable insights:

- Current RSI is 35 which is close to oversold territory

- The recent low was a few weeks ago when RSI touched below 30.

- Stock price remained relatively stable during RSI fluctuations.

Technically, VBL is not expensive and is close to a decent entry point for long-term investors.

Growth Drivers

As we all know by now that Pesi and Mirinda is its mature brands But its real growth may come from the newer products :

- Sting : It’s an energy drink that’s competing with Red Bull at ⅕ the price. Already contributing 8% of the total sales.

- Nimbus : It’s basically a lemonade drink with massive potential and its growing at 100% YoY.

- Creambell : It’s a value added dairy beverage which is growing at 80% YoY, though its contribution is still small.

These new-age products are fueling future revenue growth beyond traditional cola sales.

Strategic Initiatives

VBL isn’t just riding on its existing products. It’s actively expanding with new plants in Kangra, Prayagraj, Bihar, and Meghalaya. The company is also boosting its retail presence , aiming to grow from 40 lakh to over 1 crore outlets with aggressive visi-cooler placements.

On the financial front, VBL has strengthened its balance sheet by cutting debt through a ₹7,500 Cr QIP, reducing interest costs, and earning a CRISIL AAA (Stable) rating.

Also Check : Embassy REIT Stock Analysis 2025

Final Take

Varun Beverages remains a strong growth story with solid financials, promoter trust, and expansion plans. The recent correction makes valuations more reasonable.

Long-term investors should focus on the company’s fundamentals and future roadmap , not just past returns or market noise.

Check Other Post Posts

-

How to buy NCD in Groww?

How to buy NCD in Groww?March 11, 2025

-

How to Cancel a Withdrawal Request in Zerodha?

January 15, 2025

-

RBL Net Banking: Features, Benefits & Guide

January 8, 2025