NMDC’s Watershed Year: Breaking Down the Surge to ₹31,000+ Crore in Sales Revenue

When a commodity company reports record revenue, investors often ask the same question: was the growth driven by higher prices or stronger execution? The distinction matters because commodity prices are cyclical, while operational improvements tend to create more sustainable value.

NMDC’s FY26 performance makes this question particularly interesting. The company crossed ₹31,000 crore in sales revenue, becoming one of the strongest years in its history. At first glance, the achievement may appear to be another beneficiary of favorable iron ore market conditions. However, a closer look reveals a much deeper story- one driven by record production, rising sales volumes, and years of capacity expansion finally translating into measurable financial results.

Understanding how this operational momentum converted into revenue growth offers valuable insight into both NMDC’s current strength and its long-term growth trajectory.

The Real Story Behind ₹31,000 Crore

A record revenue figure often grabs the headlines. But for a mining company, revenue is ultimately the result of three variables: how much ore it produces, how much it sells, and the price it receives for every tonne.

FY26 was exceptional because NMDC delivered on all three.

The company produced a record 53.15 million tonnes (MT) of iron ore and sold 50.23 MT during the year. In doing so, it became the first iron ore miner in India to cross the 50 MT production milestone.

That distinction is important.

Commodity companies frequently report higher revenues during periods of strong pricing. However, volume growth is often a better indicator of operational strength because it reflects factors that management can directly influence.

In NMDC’s case, the revenue milestone was supported by record physical output. More tonnes moved out of its mines, more tonnes reached customers, and more tonnes were converted into revenue.

In other words, FY26 was not just a pricing story. It was a scale story.

Crossing 50 MT Rubicon

The 50 MT milestone is more significant than it initially appears.

Producing an additional million tonnes of iron ore is not simply a matter of mining more material. It requires mine development, equipment availability, transportation capacity, and customer demand to work together without creating bottlenecks.

Crossing 53 MT suggests that NMDC’s operating ecosystem is becoming capable of handling much larger volumes than it could just a few years ago.

More importantly, it offers investors something they have been looking for: proof of execution.

For years, NMDC’s growth narrative revolved around future expansion plans and long-term production targets. FY26 marks one of the clearest signs yet that those plans are beginning to translate into measurable results.

The company is still some distance away from its 100 MTPA ambition. But after crossing the 50 MT threshold, that target looks considerably more realistic than it did a few years ago.

From Bottlenecks to Throughput: The Infrastructure Unlock

NMDC’s FY26 volume expansion was not accidental, it was enabled by long-gestation infrastructure projects finally moving toward operational maturity.

Historically, the biggest constraint in scaling output from the Bailadila region has been evacuation capacity rather than ore availability.

This constraint is now being structurally addressed.

The upcoming downhill conveyor system at Deposit 5 is a key unlock. It is designed to increase evacuation capacity from ~12 MTPA to ~20 MTPA, significantly reducing dependency on traditional truck and rail bottlenecks.

Alongside this, the ongoing doubling of the Kottavalasa–Kirandul (KK) railway line is gradually improving long-distance logistics throughput, strengthening NMDC’s ability to sustain higher dispatch volumes from Chhattisgarh’s high-grade iron ore belt.

Together, these projects represent a step-change in logistics capability rather than incremental improvement.

Importantly, they explain how NMDC was able to cross the 50 MT production threshold without encountering major structural breakdowns in its supply chain.

The implication is clear: future growth will be increasingly defined not by mining capacity, but by how quickly logistics infrastructure can keep pace with output expansion.

From Capacity Creation to Capacity Monetization

For much of the last decade, NMDC focused on expanding mining capacity and strengthening supporting infrastructure.

These investments often carry a delayed payoff. Capital is deployed years before meaningful revenue benefits become visible.

FY26 appears to be one of the first years where investors could clearly see those investments translating into commercial outcomes.

The company was no longer simply building capacity. It was monetizing it.

That distinction matters because it changes the narrative around growth. Instead of depending solely on future projects, NMDC is increasingly generating returns from assets that are already operational.

For investors, this reduces execution uncertainty and strengthens confidence in the company’s long-term expansion strategy.

The Volume VS Price Equation

FY26 did not coincide with a global iron ore boom. In fact, external conditions were far from supportive.

China’s property sector weakness and uneven infrastructure demand kept global steel sentiment under pressure, limiting pricing strength across the iron ore value chain.

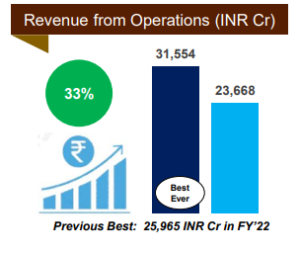

Yet NMDC delivered a 33% year-on-year jump in revenue to ₹31,554 crore.

The driver was clearly volume, not price.

Production rose 21% to 53.16 MT, while sales crossed 50.23 MT for the first time. This physical expansion allowed NMDC to partially decouple from global commodity volatility and rely more heavily on domestic demand resilience.

The key demand anchor was India’s structural steel expansion, led by integrated steel producers such as JSW Steel and ArcelorMittal Nippon Steel (AM/NS), which continued to absorb higher iron ore volumes.

In effect, NMDC’s FY26 performance was less about riding a commodity cycle and more about scaling into a structurally growing domestic consumption base.

The Operating Leverage Effect

NMDC’s operating leverage is not a theoretical concept- it is visible in its unit economics.

As production scaled up to 53.16 MT in FY26, fixed costs such as mining overheads, employee expenses, and logistics infrastructure were spread across a much larger base.

This alone naturally improves per-tonne profitability.

But the more important shift came from cost efficiency.

At key mining clusters like Bacheli in the Bailadila region, production costs have trended down toward ~₹800 per tonne, compared to earlier levels closer to ~₹1,000 per tonne. This improvement reflects better asset utilization, higher throughput, and improved operational discipline.

Despite a relatively stable global pricing environment, NMDC maintained a strong standalone EBITDA margin of ~42%.

The implication is clear: as volumes rise, NMDC is not just growing revenue, it is structurally protecting profitability through cost dilution and scale efficiency. Each incremental tonne produced now contributes more meaningfully to earnings than it did in lower operating regimes.

The Missing Nuance: Margin Stability vs Capital Commitments

While NMDC’s operational performance in FY26 was strong, consolidated financials highlight an important nuance.

Margins at the consolidated level softened in parts of FY26, with Q4 showing pressure due to working capital and support arrangements linked to the recently demerged NMDC Steel (NSL). Consolidated EBITDA margins moderated toward ~27% in this phase.

This does not negate the strength of the core mining business, where standalone margins remain robust.

However, it does highlight an important structural factor: NMDC operates within a broader public sector ecosystem where balance sheet flexibility is sometimes used to support downstream industrial capacity.

Management has indicated that such support measures are transitional in nature. Still, from an investor perspective, it introduces a layer of capital allocation complexity that must be monitored alongside operational performance.

The core mining engine remains strong but consolidated outcomes can temporarily diverge due to group-level priorities.

The 100 MTPA Credibility Test

The 100 MTPA target has long been central to NMDC’s long-term narrative. For years, it functioned more as a strategic aspiration than a near-term operational reality.

FY26 begins to change that perception.

With production crossing 53.15 MT, NMDC is now operating at more than half of its stated long-term capacity goal. While the gap to 100 MTPA remains large, the more important shift is in execution credibility.

Scaling from here is not just about ambition. It is about repeatable delivery.

Mining expansion at this scale requires alignment across multiple layers-

- Mine development

- Equipment deployment

- Evacuation infrastructure

- Steady demand from the steel sector

Any one constraint can slow the trajectory.

FY26 does not eliminate these challenges. But it demonstrates that NMDC’s system is capable of operating at a materially higher base than in the past.

That alone improves visibility on the long-term target and reduces uncertainty around execution risk.

Key Metrics Investors Should Track

With NMDC entering a higher operating base, future performance will be judged less on expansion intent and more on consistency of delivery.

The first key metric is production and sales volume growth. Sustaining momentum above the 50 MT level will be critical in determining whether FY26 was a peak or a new baseline.

The second is realisations per tonne. While volumes drive scale, pricing determines the quality of earnings, especially in a commodity-linked business.

The third is progress on capacity expansion projects. Timely commissioning of new mines and debottlenecking existing assets will decide how quickly NMDC can move toward its 100 MTPA ambition.

Together, these metrics will define whether NMDC’s FY26 performance marks a one-year peak or the beginning of a sustained structural upcycle in operating scale.

Conclusion

FY26 was not just a record revenue year for NMDC. It was the year its long-term expansion strategy finally showed up in production, sales, and revenue together.

Crossing ₹31,000 crore in sales revenue reflected more than pricing strength. It was backed by record production of 53.15 MT and sales crossing 50 MT, marking a clear shift in operating scale.

What stands out is the transition from capacity creation to capacity utilization. Years of investment in mines and infrastructure are now translating into measurable output.

That said, FY26 is still an inflection point, not an endpoint. Sustaining this scale and progressing toward 100 MTPA will determine whether this becomes a one-year peak or the start of a longer growth cycle.

For investors, the message is simple: NMDC is no longer just building capacity, it is beginning to consistently monetize it.