KPIT Tech: Is the Worst Phase over?

For years, KPIT Technologies has been one of India's fastest-growing automotive engineering companies, benefiting from the global shift toward electric vehicles, software-defined vehicles, autonomous driving, and connected mobility.

However, that growth story faced an unexpected setback when the company warned that its Q1 FY27 revenue is likely to decline by around 1% year-on-year, primarily due to sudden actions taken by multiple European automobile manufacturers. The announcement caught investors off guard because the slowdown emerged only in the final few weeks of the quarter, forcing the company to revise expectations after previously maintaining a healthy outlook.

The market's reaction was immediate. Investors were no longer asking whether Q1 would be weak—the bigger question became whether this marks a temporary pause in KPIT's long-term growth story or the beginning of a more prolonged slowdown in automotive engineering spending.

Management believes the disruption is temporary and expects the business to recover in the second half of FY27, supported by new markets, expanding technology offerings, AI-led initiatives, and a resilient order pipeline. At the same time, the company has acknowledged that Q2 FY27 revenue is expected to remain broadly similar to Q1, indicating that an immediate recovery is unlikely.

So, has KPIT already gone through its worst phase, or should investors prepare for further challenges? To answer that, we need to examine what actually happened, why it happened, and whether the company's recovery thesis is supported by the available evidence.

What Exactly Happened?

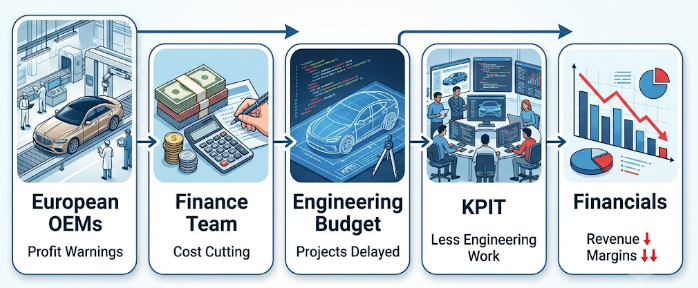

The slowdown at KPIT Technologies did not originate within the company. Instead, it was the result of a rapid change in customer behavior.

According to the company's latest outlook, multiple European automobile manufacturers (OEMs) revised their business outlook after issuing profit warnings. In response, these companies cut discretionary spending, including engineering and product development budgets for partners like KPIT.

Because KPIT derives a significant portion of its business from automotive engineering services, these decisions had an almost immediate impact.

Projects were delayed, scaled down, or temporarily paused, reducing work during the final weeks of the quarter. The slowdown emerged late in the quarter, leaving little time to offset the lost revenue before Q1 results.

To address investor concerns, the company clarified a day later that Q2 FY27 revenue is expected to remain broadly in line with Q1 FY27, suggesting that while the sharp deterioration may have stabilized, management is not yet forecasting an immediate rebound.

In simple terms, the sequence was clear:

European automakers faced business pressure → reduced engineering spending → outsourced work to KPIT declined → revenue softened → margins came under even greater pressure.

Why Did Demand for KPIT's Services Slow Down in Europe?

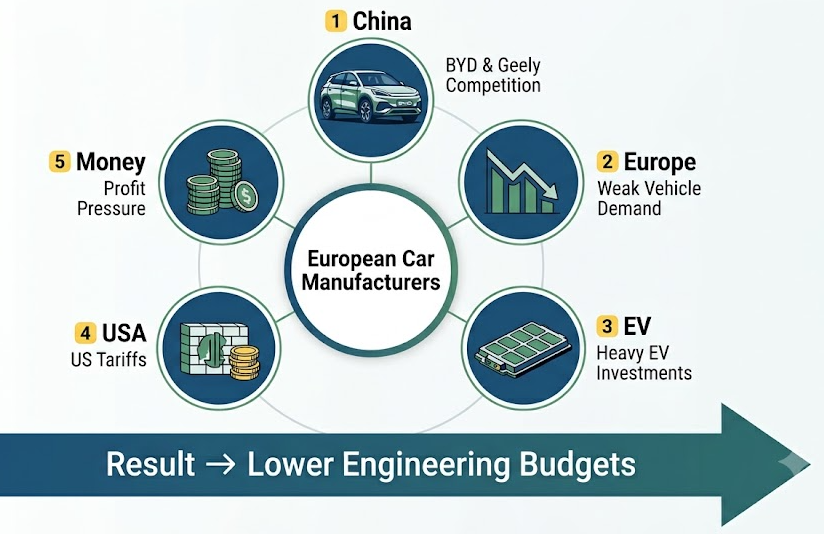

The slowdown in KPIT's European business was not driven by a decline in demand for automotive software. Instead, it was a consequence of the financial and strategic challenges facing European automakers.

Over the past few years, European OEMs have steadily lost market share to Chinese EV manufacturers such as BYD and Geely, particularly in China—once one of their most profitable markets. At the same time, weak vehicle demand in Europe, heavy investments in electrification, and geopolitical pressures, including US tariffs, have weighed on their profitability.

In response, several automakers shifted their focus from growth to financial discipline. Companies like Volkswagen announced restructuring measures such as factory closures, workforce reductions, lower capital expenditure, and broader cost-control initiatives. Rather than abandoning software development, many OEMs chose to delay, reprioritize, or phase engineering and vehicle development programs that were not immediately critical.

What Is Management's Recovery Plan?

Despite the weak near-term outlook, KPIT believes the slowdown is temporary and expects the business to recover through a combination of strategic initiatives:

- Leverage outsourcing trend -

Management believes that as automakers intensify cost-cutting, they will increasingly outsource engineering work, creating long-term opportunities for KPIT. - Focus on growth drivers -

The company expects continued traction from its Products & Solutions business, US, Korea, and India markets, Trucks & Off-Highway segment, new client wins, and technology areas such as Autonomous Driving, Connected Vehicles, After-sales, and Full Vehicle Design & Engineering - Improve efficiency -

KPIT is implementing AI-led productivity improvements and cost-containment measures while continuing to invest in AI-powered products and solutions. - Recovery timeline -

Management expects Q2 FY27 to remain similar to Q1, with sustainable growth in H2 FY27 and stronger sequential growth by Q4 FY27, laying the foundation for FY28.

Is the Worst Phase Really Over?

At this stage, there are valid arguments on both sides. While management believes the slowdown is temporary, investors should weigh both the positives and the risks before concluding that the worst is over.

🟢 Bull Case: Why the Worst Could Be Over

- Q2 appears to have stabilized -

Management expects Q2 FY27 revenue to remain broadly in line with Q1, indicating that the sharp deterioration seen in Q1 is unlikely to worsen further. - Recovery drivers remain intact -

The company continues to see traction in the US, Korea, and India, along with growth in its Products & Solutions business, Trucks & Off-Highway segment, and new client acquisitions. - Strong future visibility -

A resilient order book and a growing project pipeline suggest that customer demand has slowed, but not disappeared. - Long-term outsourcing trend -

Management believes that as automakers focus on reducing costs, outsourcing engineering work will increase, creating long-term opportunities for companies like KPIT.

🔴 Bear Case: Why Investors Should Still Be Cautious

- Recovery has not started yet -

Although Q2 is expected to stabilize, management is not expecting meaningful growth until the second half of FY27. - Europe remains the biggest risk -

If European automakers continue restructuring or delay engineering programs for longer than expected, KPIT's recovery could take more time. - Margins remain under pressure -

Even a small decline in revenue has a larger impact on profitability because employee costs cannot be reduced immediately. - Execution is key -

Management's recovery plan now needs to translate into actual revenue growth, stronger margins, and sustained project wins over the coming quarters.

⚖️ Balanced Opinion

Based on the available information, the worst may be behind KPIT, but it cannot yet be declared over. The immediate shock appears to have stabilized, and the company's long-term growth drivers remain intact. However, a sustained recovery will depend on whether European OEMs resume engineering spending and whether KPIT delivers the H2 FY27 growth that management has guided for.

For investors, the next two quarters will be crucial. If management's recovery thesis plays out, the current slowdown may prove to be a temporary bump. If not, the recovery timeline could extend further than expected.

Key Factors Investors Should Watch Going Forward

Whether KPIT's recovery materializes over the coming quarters will largely depend on a few critical indicators. Investors should closely monitor the following:

1. Q2 FY27 Revenue Performance

Management has guided that Q2 revenue is likely to remain similar to Q1. Any improvement beyond this would indicate that customer spending is recovering faster than expected, while another decline could signal prolonged weakness.

2. Engineering Spending by European OEMs

3. Margin Recovery

KPIT expects margins to come under pressure in the near term. Investors should watch whether AI-led productivity initiatives and cost-containment measures begin supporting profitability over the coming quarters.

4. Order Book & New Deal Wins

A resilient order book and continued client additions will indicate whether customer confidence remains strong despite the temporary slowdown.

5. Management's H2 FY27 Execution

The company has guided for a recovery in the second half of FY27. Delivering on this guidance will be the biggest test of management's recovery thesis.

Conclusion

KPIT Technologies has undoubtedly entered one of its most challenging phases in recent years. The available evidence suggests that the slowdown is more cyclical than structural. It is mainly driven by temporary spending cuts by European automakers, not weaker competitiveness or demand for software-defined vehicles.

At the same time, it would be premature to declare that the worst is completely over. Management itself expects Q2 FY27 to remain similar to Q1, indicating that the recovery has yet to materialize. The real test will come in the second half of FY27, when KPIT aims to convert its strong order book and AI initiatives into stronger financial performance.

For long-term investors, the current situation should be viewed as a period to monitor rather than to panic. If European OEM spending normalizes and KPIT delivers on it's H2 FY27 guidance, the slowdown may prove temporary. However, until those improvements become visible in quarterly results, cautious optimism remains the most reasonable stance.