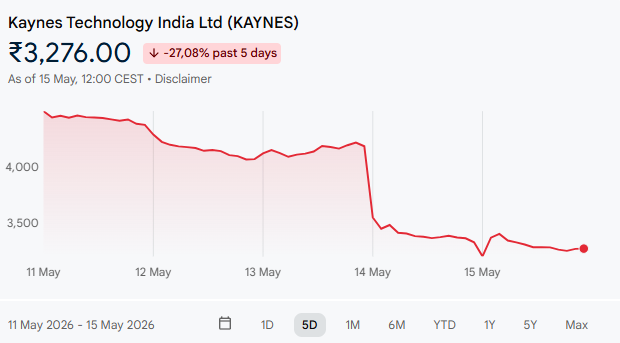

Why did Kaynes Stock Price Crash? May 15, 2026

Kaynes Technology shares witnessed a sharp intraday fall of ~17%–20% after Q4 FY26 results, disappointing the market.

Despite revenue growth, a decline in profits, margin pressure, and weaker-than-expected guidance led to negative investor sentiment.

This triggered heavy selling, further intensified by valuation concerns and brokerage downgrades.

Trigger Event: Weak Q4 FY26 Earnings

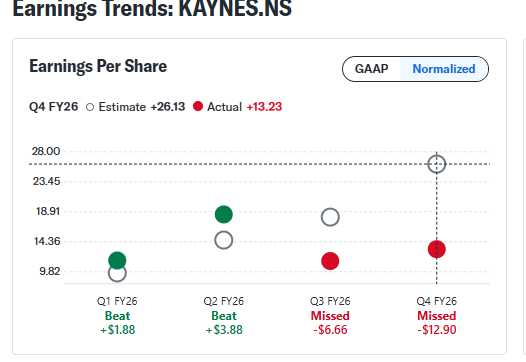

The sharp fall in Kaynes Technology’s stock was triggered by its Q4 FY26 results, where revenue grew around ~26% YoY but net profit declined by about ~21% YoY to ~₹91 crore.

This contrast between strong top-line growth and weaker bottom-line performance disappointed the market.

In a high-growth stock like Kaynes, investors primarily price in consistent earnings expansion. Even though sales momentum remained intact, the drop in profitability signaled margin and execution pressure, which was enough to trigger a sharp re-rating in the stock.

So, Growth in revenue, but fall in profit = Negative Surprise

Key Reasons for the Fall

1. Profit Decline & Margin Pressure

One of the biggest reasons behind the sharp fall was the clear pressure on profitability in Q4 FY2026. The company reported a decline in net profit along with margin contractions in EBITDA levels, while the revenue continued to grow.

From a market perspective, this was a bigger concern than the profit drop itself. Kaynes is positioned as a high-growth EMS player, where investors expect both scale and expanding margins.

So when margins start slipping, it raises doubts about how efficiently the company can handle rapid expansion.

2. Missed Guidance & Execution Concerns

Apart from weak profits, the market also got worried about the company’s future outlook. The management did not sound as strong as expected on future growth, and there were hints that execution may not be as smooth in the coming quarters.

For investors, this was important because Kaynes is valued as a fast-growing company.

So when there is even slight doubt about how well it can turn orders into actual revenue and profit, confidence drops quickly.

This uncertainty added more pressure on the stock fall.

3. Balance Sheet & Cash Flow Worries

Another concern for the market was the company’s cash flow and working capital situation. Even though Kaynes has a strong order book, investors started questioning how smoothly it is converting business into actual cash.

There were signs of pressure in receivables and working capital, which means money is getting stuck for longer in the business cycle.

For investors, this is important because weak cash flow can reduce financial flexibility, even if revenue is growing.

This added another layer of concern to the stock’s sharp fall.

4. Brokerage Downgrades

The fall was further intensified after several brokerages downgraded the stock or cut their target prices. This happened mainly because of weaker-than-expected profits, margin pressure, and concerns about execution going forward.

When big brokerages turn cautious, it impacts market sentiment quickly because institutional investors often follow these signals.

As a result, selling pressure increased, making the stock fall even sharper in a short period.

5. Sentiment Reversal in EMS Sector

The broader electronics manufacturing services (EMS) sector also played a role in the fall. Earlier, EMS stocks like Kaynes were trading at high valuations due to strong growth expectations and themes like “China+1” and rising electronics demand.

However, once results showed even slight weakness in profits and margins, sentiment shifted quickly. In such high-expectation sectors, investors tend to react strongly, and optimism can turn into caution very fast.

This change in sentiment amplified the selling pressure on the stock.

Technical Breakdown

Post results, the stock fell by nearly 15% in a short span, with volumes rising significantly above average levels. It also broke key short-term support levels and moved below important moving averages.

This triggered stop-loss selling and momentum exits, which accelerated the fall beyond fundamental reasons. The combination of high volume and broken technical levels confirmed a broader exit by traders and institutions.

Peer Benchmark: Kaynes vs Dixon

| Metric | Kaynes Technology | Dixon Technologies | Interpretation |

| Market Position | Mid-cap EMS player | Large-cap EMS leader | Dixon has scale advantage |

| Business Stage | High-growth phase | Mature growth phase | Kaynes = higher volatility potential |

| Revenue Growth | Faster but less stable | Steady and consistent | Market rewards stability differently |

| Margin Profile | Relatively improving | More stable margins | Dixon = predictability premium |

| Client Base | Diversifying | More diversified & established | Lower perceived risk in Dixon |

| Valuation Perception | Premium growth stock | Quality compounder | Kaynes more sentiment-sensitive |

| Stock Behavior | Higher volatility | Relatively stable trends | Explains sharper corrections |

This comparison shows a key market reality: the same sector doesn’t mean the same risk pricing.

Kaynes behaves like a high-expectation growth stock, where sentiment shifts can trigger sharp corrections.

Dixon, in contrast, is priced more like a steady compounder with more gradual, earnings-driven moves.

So, Kaynes’ 15–20% correction is not just a standalone fall, but also a reflection of how the market values growth versus stability within the same sector.

Conclusion

Kaynes’ recent correction reflects a broader re-rating in the EMS sector rather than a standalone weakness. It highlights how high-growth stocks face sharper moves due to elevated expectations.

In the end, it’s a reminder that in such sectors, volatility often comes with growth.