PhonePe IPO: Business Model, Risks and Valuation

Do you remember the Paytm IPO? The stock fell nearly 30% within two days of listing and went on to decline over 70% within the first four months. That episode sets the context for a deeper PhonePe IPO analysis, reminding investors that popular fintech brands do not automatically translate into successful IPOs.

Now, as the market prepares for another major fintech listing - the PhonePe IPO - it may be tempting to draw quick parallels with Paytm. Fundamentally, the two companies are very different. Their business models, revenue structures, and risk profiles vary significantly, and understanding these differences is crucial before making any IPO decision.

PhonePe Is Not Just a UPI App

A common misconception is that PhonePe is merely a UPI payments app. In reality, UPI is only the entry point, not the end product.

Nearly half of all UPI transactions in India are routed through PhonePe, making it the undisputed market leader. This scale gives PhonePe a massive advantage - habit formation. Users open the app daily, creating a powerful distribution channel.

However, P2P UPI transactions are free. When individuals transfer money to each other, PhonePe earns nothing.

PhonePe's revenue comes from three primary sources:

- Merchant payments, where shops pay a fee on QR-based transactions

- Utility services, such as bill payments and recharges

- Financial products, including loans, insurance, and investments, where PhonePe earns commissions by generating leads for banks and insurers

In simple terms, UPI brings users, while financial products are expected to bring profits.

Watch Our Video on PhonePe IPO

A Pure OFS IPO: What That Really Means

One of the most important aspects of the PhonePe IPO is that it is a pure Offer for Sale (OFS).

This means:

- No fresh capital will enter the company

- All proceeds go to existing shareholders

The promoter, Walmart, plans to sell around 9% stake, while still retaining majority ownership (~63%). Early investors such as Microsoft and Tiger Global are expected to exit fully.

This creates a potential overhang risk. Since Walmart will continue to hold a large stake, future stake sales after the lock-in period could pressure the stock price. Investors should factor this into their expectations.

Do Pure OFS IPOs Perform Well?

Historical data paints a mixed picture.

Between 2023 and 2025, most pure OFS IPOs struggled in the short term, with a higher probability of negative or muted returns shortly after listing. However, some companies did recover in the medium term, provided the underlying business executed well.

The key takeaway is simple: A good business does not guarantee a fairly priced IPO. Better entry opportunities can emerge post-listing.

Structural Dependency on Banks for UPI

PhonePe does not have a banking licence. To operate UPI, it depends on sponsor banks such as Axis Bank, ICICI Bank, and Yes Bank.

This creates a structural risk. If a sponsor bank faces:

- Technical outages

- Compliance issues

- Regulatory restrictions

PhonePe's core UPI service can be disrupted, even if PhonePe itself has done nothing wrong. This dependency is inherent to the model, not a temporary issue.

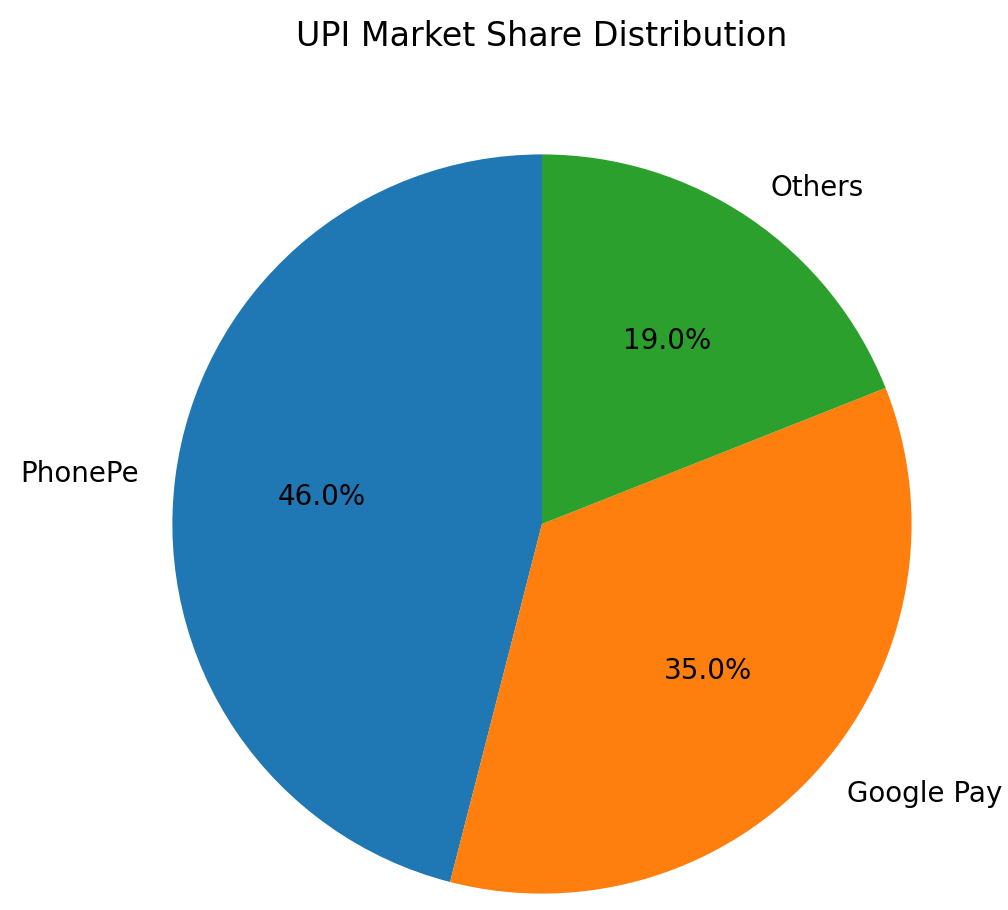

NPCI's 30% Market Share Proposal

The National Payments Corporation of India (NPCI) has proposed a rule limiting any single UPI app to 30% of total transactions.

Current reality:

- PhonePe: 45-47% share

- Google Pay: 35%

- Others combined: 20%

If strictly enforced, this rule would cap PhonePe's natural growth, restrict new user additions, and indirectly impact monetisation of financial products. While implementation has been deferred multiple times (latest timeline around December 2026), it remains a regulatory overhang investors cannot ignore.

Lending and Insurance: The Real Growth Engine

PhonePe's biggest long-term opportunity lies in lending and insurance distribution.

Think of PhonePe as a busy highway. UPI traffic is free, but financial products are the toll booths.

- FY23: Lending & insurance contributed ~1% of revenue

- FY25: Contribution rose to ~8%, making it one of the fastest-growing segments

With access to user spending behaviour, merchant data, and transaction history, PhonePe is well-positioned to distribute high-margin financial products. However, execution risk remains high. Failure to scale these businesses would significantly weaken the growth story.

Valuation Through the P/S Lens

PhonePe generated ₹7,100+ crore revenue in FY25 and turned operating cash-flow positive. However, it remains net-loss making, largely due to ESOP-related non-cash expenses.

As a result, valuation must be judged using the Price-to-Sales (P/S) ratio.

At an estimated valuation of ₹1.25 lakh crore, PhonePe would list at approximately 17× P/S, which is aggressive when compared to peers:

- Paytm: 10×

- Policybazaar: 11×

- Pine Labs: 11×

- MobiKwik: 1.5×

This valuation assumes strong success beyond UPI, particularly in lending and insurance.

Indus Appstore: High Expectations, Low Visibility

PhonePe's Indus Appstore, positioned as an alternative to Google Play Store, carries ₹684 crore of goodwill on the balance sheet. In FY25, revenue from new platforms (including Indus) was only ₹29 crore, less than 0.5% of total revenue. This makes it a long-term, high-risk bet with minimal current monetisation.

Conclusion

PhonePe is a powerful brand and UPI market leader, but its IPO is not a low-risk opportunity.

The company's future depends on:

- Regulatory stability in UPI

- Successful scaling of lending and insurance

- Justifying an aggressive valuation

Blindly applying based on brand recognition alone could be risky. Understanding valuation, execution capability, and regulatory exposure is essential before making any decision.