Why UBS Issued a Sell Call & Lowered IDFC First Bank’s Target Price?

IDFC First Bank's stock has been weak for the past few days. This happened after UBS, a very big research and investment firm from Switzerland, downgraded the stock to "Sell." Because UBS is known across the world, many traders and funds reacted immediately and started selling. The bank's business is still strong. But the downgrade raised a big question. If the bank is doing well, why did UBS turn negative on the stock? To understand this, we must look at two things. First, what UBS thinks. Second, what the market was expecting. UBS is respected worldwide, and when it gives a strong opinion-especially a Sell call-the market moves fast. Even UBS agrees that the bank has strong fundamentals. CASA ratio is high, loan growth is steady, and NPAs are under control. Digital banking is also improving. So the business itself is fine. The main issue, according to UBS, is not the bank. The issue is the valuation and the speed at which profits are growing. UBS feels the stock price has already priced in all good future news, even before those things have actually happened.

Strong Fundamentals but an Overvalued Stock

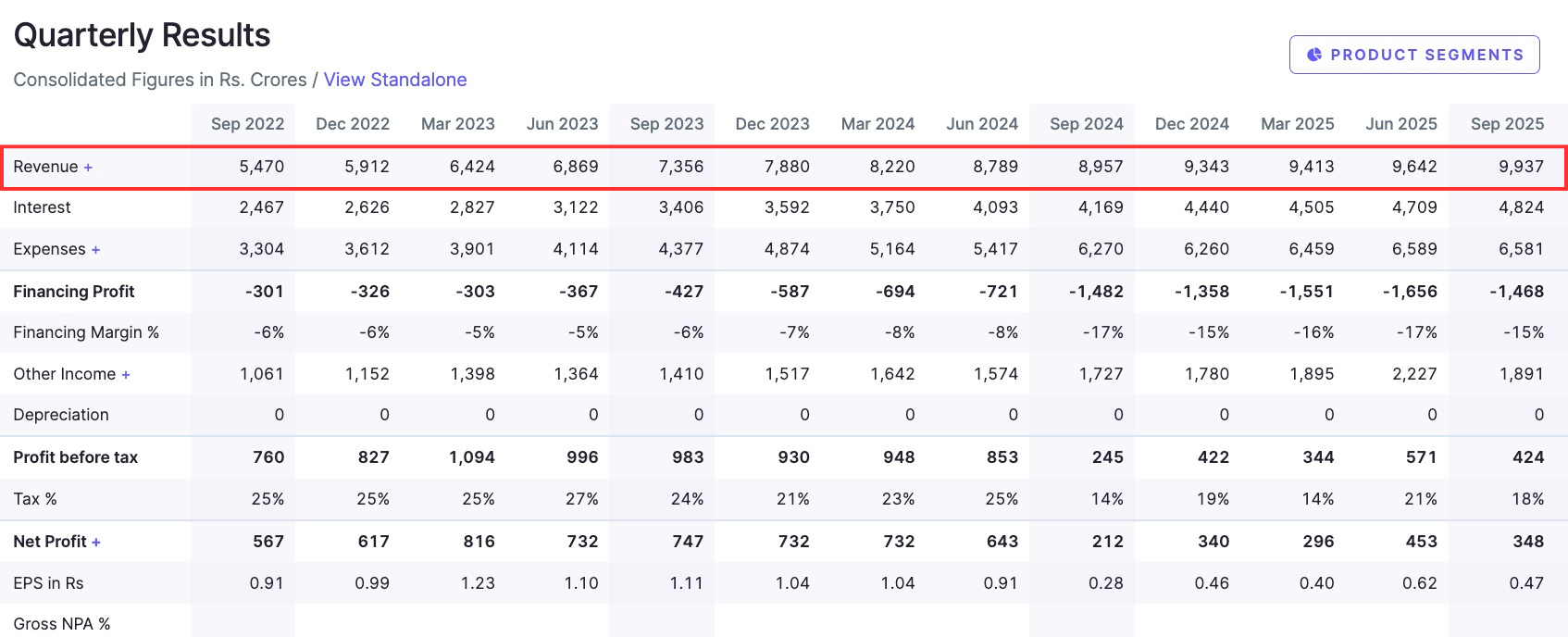

UBS said clearly that IDFC First Bank continues to perform well operationally. The bank is strong in retail deposits, its CASA base is solid, and customers are staying loyal. NPAs are under control, and loan growth is good. The bank's digital push is also working. Customer activity on its mobile app and online banking is rising. So the basic business model is stable. However, UBS believes the stock price has run ahead of the actual numbers. The stock moved up quickly because the market expected strong earnings growth in advance. But UBS feels this growth will take time. UBS cut the target price to ₹75 from ₹80. This means UBS thinks the current valuation is too high based on the bank's likely profit growth. The stock is not "bad," but it is "expensive" compared to what it is earning right now. This gap between price and real earnings potential is what concerns UBS. And this is why they issued a Sell call.

Profitability May Improve, But Not at the Expected Pace

UBS believes the bank will become more profitable. But the increase will be slow and steady, not fast. This goes against what many traders were expecting. UBS expects the net interest margin (NIM) to stay around 5.8%. It also expects the cost-to-income ratio to remain close to 67% for FY26-28. These numbers are healthy, but they are not high enough to justify a very high stock price. Return on Assets (ROA) is expected to reach only around 0.9% to 1% by FY27. This means the bank will be profitable, but not extremely profitable in the near future. So the growth will be moderate. The CEO of the bank has also said that major improvement in profits will start only after one year. This is because the bank is still paying high interest rates on fixed deposits taken earlier. Banks take time to benefit from falling deposit rates. This slow pace of margin recovery means earnings will rise, but not as quickly as the market hoped. UBS highlighted this difference between "market expectation" and "actual possible performance." That difference became a key reason for the downgrade.

Understanding the Deposit Cost and Credit Cost Impact

One of the biggest challenges for IDFC First Bank right now is high fixed deposit (FD) rates. When interest rates in the economy start falling, banks do not benefit immediately. Old high-rate deposits stay on the books for some time. UBS said it usually takes 12-18 months for a bank to fully benefit from lower deposit rates. Till then, margins remain under pressure. This means the bank cannot expand its NIM very quickly. UBS also pointed out something about the loan book. Around 13% of IDFC First Bank's loans are unsecured and SME loans. These loans normally carry slightly higher credit costs. UBS is not saying there is a high risk of default. It is only saying that these loan categories naturally create higher expenses. This slightly reduces the speed at which profits can grow. When margins are slow and credit costs are a bit high, the overall earnings increase becomes slower. These combined factors made UBS cautious about the next few quarters. Also Read - KPIT Tech Stock Analysis 2025: What Investors Should Know

Why Market Reacted Immediately?

The market fell sharply after the UBS report because UBS has huge influence. Global investors follow UBS closely. When UBS changes its rating, big funds and FIIs reconsider their positions. Domestic mutual funds and PMS managers also pay attention to such reports. Traders follow these signals even faster. So the result was quick selling in the stock. This selling was not because the bank suddenly became weak. It happened because the market sentiment turned negative. Sometimes sentiment drives stock movements more than fundamentals.

Short-Term vs Long-Term Investor View

Short-term investors should take the downgrade seriously. The next few quarters may not deliver the high growth that was expected. So the stock may stay range-bound or even face small corrections. Those looking for quick gains in 6-12 months may not get much upside. The stock may need time before it begins a strong uptrend again. But long-term investors can still stay calm. The bank's basic business is improving every year. Retail franchise is expanding, CASA is rising, and NPAs are stable. The bank's digital banking push is bringing more customers and transactions. Once deposit costs normalize and FDs reprice at lower rates, margins will naturally improve. This will support strong and steady profit growth in the long run. UBS's concerns are mostly about valuation and short-term expectations. UBS is not questioning the bank's long-term strength or its business model.

Watch Our 10 points Stock Analysis of IDFC First Bank!

Quick Snapshot of UBS's View vs Market Perception

Valuation UBS feels the stock is overvalued at current levels. The market felt it was fairly valued because of the strong growth story. Profit Growth UBS expects slow and steady growth. The market expected quick and strong growth. NIM Trend UBS expects margins to stay stable around 5.8%. The market expected sharp margin expansion. ROA Estimate UBS expects ROA of around 0.9%-1.0% by FY27. The market was expecting higher ROA. Deposit Cost Impact UBS believes margin recovery will take about one more year. Investors expected faster improvement. This gap shows why the market reacted so strongly to the UBS report.

Conclusion

The fall in IDFC First Bank's stock came mainly from UBS's opinion that the current stock price does not match the bank's near-term earnings potential. The bank's fundamentals are still strong, but profitability may grow slowly for the next few quarters. Full margin expansion may take another year to show. This difference between valuation and near-term performance is the main reason behind UBS's Sell call and lower target price. For short-term investors, this serves as a warning. But for long-term investors, the story is still positive. The bank has strong retail growth, stable asset quality, and improving digital operations. UBS is not doubting the bank's strength. It is only saying that the stock price is ahead of its short-term earnings. With patience, long-term investors may still see good results once deposit costs reduce and profitability rises steadily.

Check Other Post Posts

-

SBI Unipay: Login, Features, Benefits & Customer Support

SBI Unipay: Login, Features, Benefits & Customer SupportFebruary 12, 2025

-

How to Link Your Aadhaar with Your SBI Bank Account?

November 23, 2024

-

What is the Price Limit on the Groww?

January 23, 2025