Waaree Energies: Tariffs, Order Book & Future Outlook

Waaree Energies is one of the India's leading solar manufacturing companies which operates across the full value chain-from solar cells to finished modules. Alongside this, its subsidiary Waaree Renewables focuses purely on EPC (Engineering, Procurement, Construction), executing large scale solar projects. This Waaree Energies analysis gives a clear view of its business and future growth potential.

Waaree Energies holds a majority stake (around 75%) in Waaree Renewables. This means its consolidated financials already include EPC business performance. While US tariffs and industry oversupply are key risks, the company is actively mitigating them through supply chain diversification and US manufacturing expansion.

Does the Israel-US-Iran Conflict Impact Waaree Energies?

With ongoing geopolitical tensions like the US-Iran conflict, many investors worry about global exposure. However, instead of focusing on politics, it's more important to understand two things:

- Whether the Middle East is a key market for Waaree Energies

- Whether crude oil prices impact its business

Crude Oil Impact: Indirect but Manageable

Waaree Energies operated in solar energy, which means it is not directly dependent on crude oil. However, rising oil prices can still have an indirect impact.

When oil prices increase:

- Inflation rises, leading to potential interest rate hikes

- Higher rates make project financing and capex more expensive

- EPC projects and manufacturing expansion costs increase

Additionally, solar manufacturing uses materials like polymers, backsheets and adhesives which are oil based. This can lead to 5-10% increase in raw material costs, putting slight pressure on margins.

Another factor is logistics and freight costs. Since Waaree exports significantly to the US, higher fuel prices increase shipping and transportation expenses.

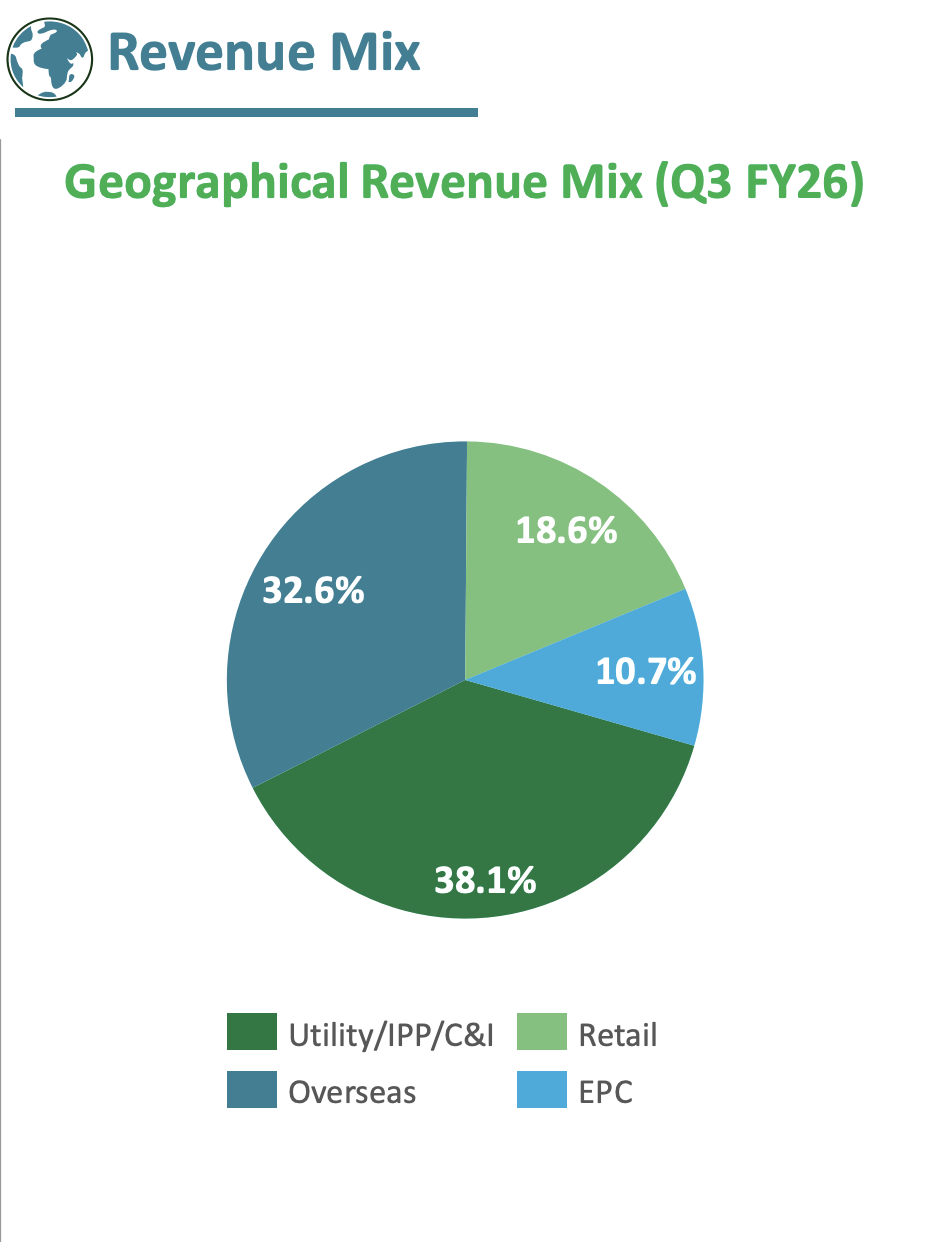

Geographic Revenue: No Direct War Exposure

A major positive for Waaree Energies is its lack of dependence on the Middle East.

- Revenue primarily comes from:

- India

- United States (US)

The US alone contributes a significant portion of overseas revenue (32%). Unlike companies with heavy Middle East exposure, Waaree's business is not directly affected by regional conflicts.

US Tariffs: The Biggest Challenge

In February 2026, the US government imposed 126% countervailing duties (CVD) on solar imports from India and other countries.

This is a major concern because:

- The US is Waaree's largest growth market

- Around 60% of its order book is linked to US demand

- High tariffs reduce price competitiveness

Additionally, ongoing investigations into dumping practices could lead to further tariff increases.

How Waaree Energies is Handling Tariffs?

Instead of being negatively impacted, the company is taking strategic steps:

1. Supply Chain Diversification

- Sourcing solar cells from low-duty jurisdictions (10%)

- Moving towards non-Chinese polysilicon (e.g., Oman)

2. Expanding US Manufacturing

- Current capacity: 2.6 GW

- Target: 4.2 GW by 2026

This allows the company to:

- Avoid heavy tariffs

- Benefit from US tax credits and incentives

This proactive approach highlights strong management execution and long-term focus.

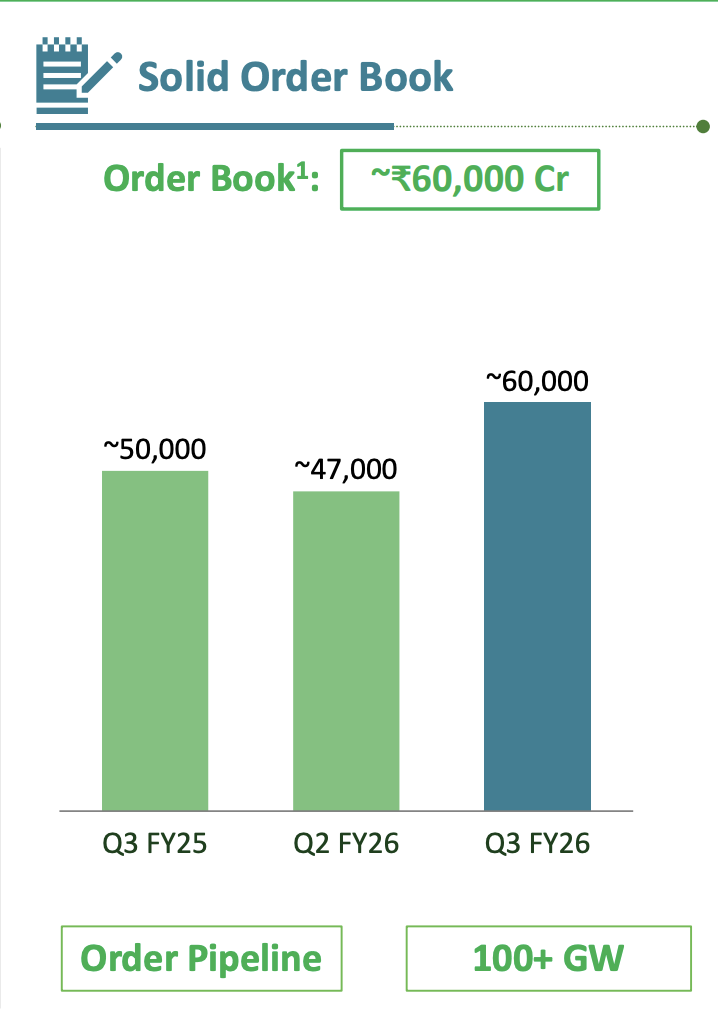

Strong Order Book: High Revenue Visibility

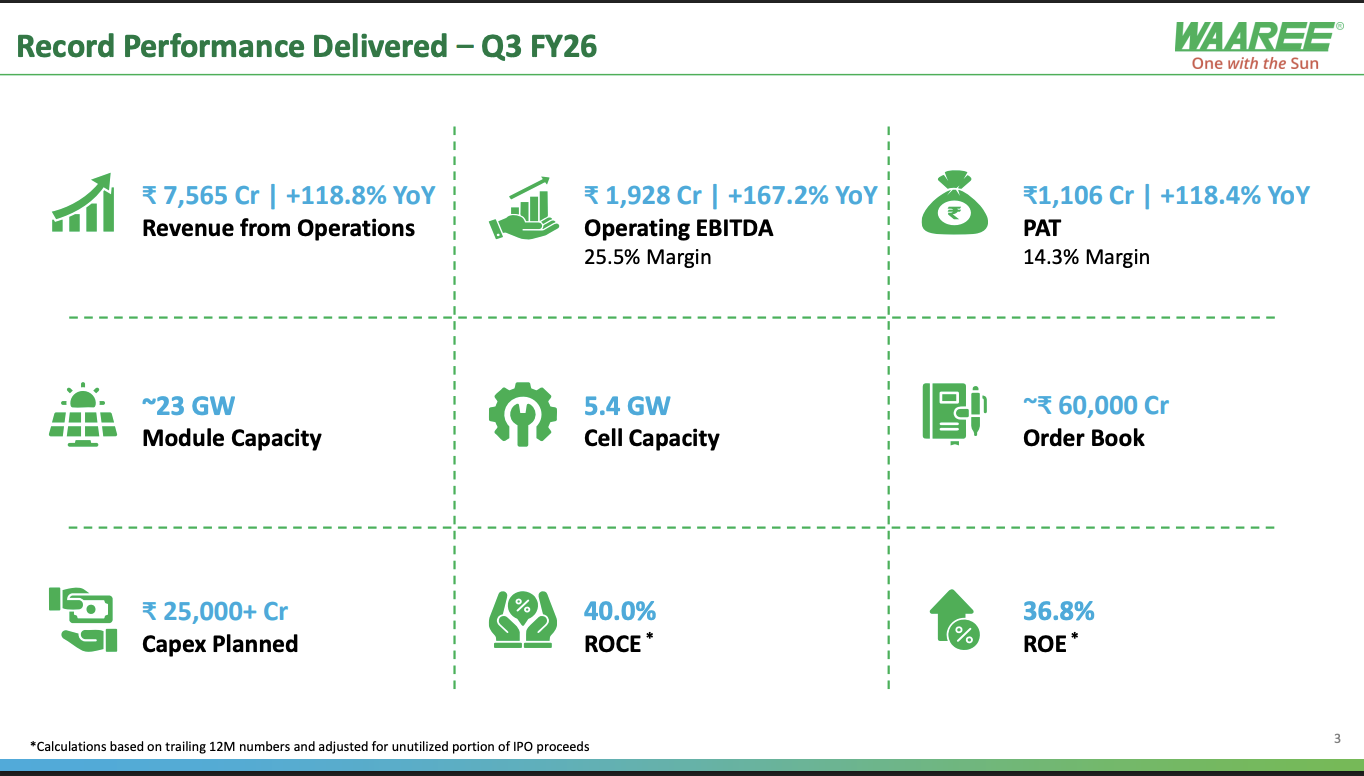

Waaree Energies has a ₹60,000 crore order book, nearly three times its annual revenue.

Key Insights:

- 35% domestic orders

- 65% overseas orders (mainly US)

- Significant growth from ₹47,000 crore to ₹60,000 crore

The company also has a 100 GW order pipeline, indicating strong future demand. This provides clear revenue visibility for the next 2-3 years.

Vertical Integration: Key to Margin Expansion

In the solar industry, backward integration plays a crucial role in maintaining margins.

Current Capacity:

- Modules: 23 GW

- Cells: 5.4 GW

- Wafers/Ingot: Not yet developed

Future Targets:

- Modules: 28.4 GW

- Cells: 15.4 GW

- Wafers/Ingot: 10 GW

This expansion will help:

- Reduce dependency on external suppliers

- Improve cost efficiency and margins

- Strengthen long-term competitiveness

BESS Entry: A Major Future Opportunity

Waaree Energies is entering the Battery Energy Storage Systems (BESS) segment with a ₹10,000 crore investment.

Highlights:

- The company has planned a battery storage capacity of 20 GWh, which indicates a large-scale entry into the energy storage segment.

- This project will include the manufacturing of battery cells, battery packs, and complete storage systems, allowing the company to participate across the entire BESS value chain.

- The implementation of this capacity will be done in phases, with full completion expected by FY 2028, ensuring a gradual and structured expansion.

As solar projects increasingly require energy storage, this creates strong synergy with its EPC business. This could become a major long-term growth driver.

Additional Growth Areas

1. Inverters & Transformers

- 4 GW inverter capacity

- Transformer expansion to 20,000 MVA

- UL certification enables exports to US & Canada

These segments may not drive massive revenue but can enhance margins and integration.

2. Green Hydrogen (Long-Term Opportunity)

- 1 GW electrolyser plant planned

- Supported by government incentives (PLI)

While promising, this segment is expected to contribute only in the long term.

Key Risk: Solar Sector Oversupply

- Strong export capabilities

- And robust backward integration to control costs

Waaree Energies appears to be relatively well-positioned on both fronts, but this remains a sector wide risk that should not be ignored.

Conclusion

Overall, Waaree Energies stands out with its strong order book, global presence, and expansion across the solar value chain. While risks like US tariffs and industry oversupply exist, the company's strategic execution, backward integration, and entry into BESS position it well for future growth.

Check Other Post Posts

-

How to Check Sarva Haryana Gramin Bank Balance?

How to Check Sarva Haryana Gramin Bank Balance?October 8, 2024

-

How to Check Bank of Baroda Balance?

February 14, 2025

-

UCO Bank Net Banking: Registration and Login Process

October 23, 2024