KPIT Tech Stock Analysis 2025: What Investors Should Know

In a world where cars are becoming smarter, faster, and more connected, one company is quietly powering this transformation from behind the scenes which is KPIT Technologies. Specializing in automotive software, KPIT is helping global carmakers shift towards electric, autonomous and software driven vehicles.

This KPIT Tech stock analysis breaks down a company's business, risks, growth potential, financial strength, and valuation in a simple yet insightful 10-point format. Let’s decode what makes KPIT a rising star in the auto-tech space.

Business Model

KPIT Tech is a software engineering company focused entirely on the automobile industry. It develops advanced software for modern vehicle features like touchscreen controls, lighting, ADAS (driver assistance), and autonomous driving systems.

Its expertise includes cloud services, vehicle connectivity, and VehicleOS - a dedicated car operating system that earns recurring revenue through licensing. With clients like Honda, BMW, and Renault, KPIT is a trusted name in automotive software.

Risk Assessment

While KPIT Tech derives 100% of its revenue from the automobile sector, this KPIT Technologies stock analysis shows that the risk is not as straightforward. The company operates on long-term contracts, offering regular updates and maintenance rather than one time services. Its revenue is more linked to clients’ R&D budgets than actual vehicle sales.

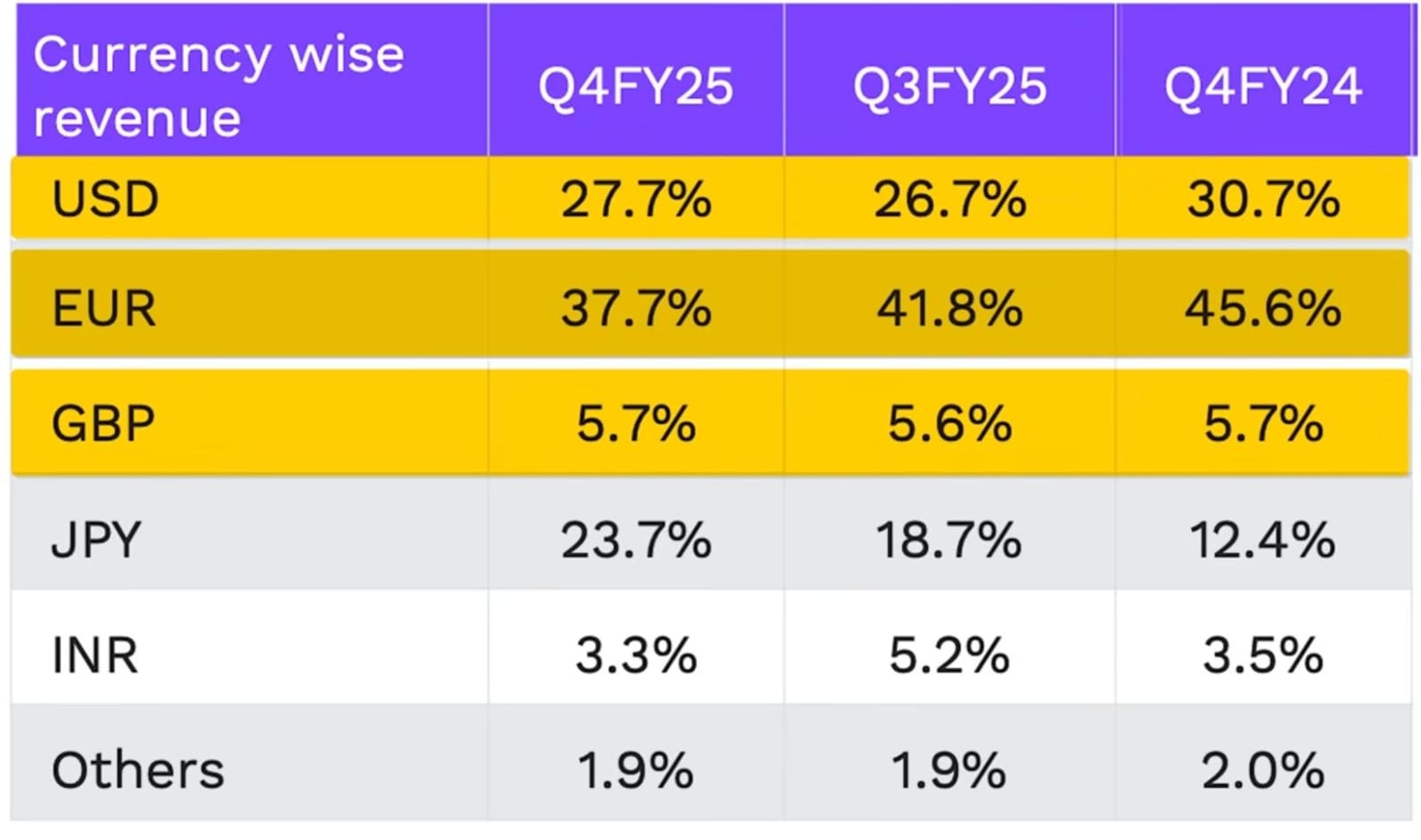

Additionally, KPIT has reduced its geographic concentration risk. Earlier heavily dependent on North America and Europe, the company has now expanded its client base in Japan, creating a more balanced and stable global presence.

Future Growth Prospects

KPIT is likely to see slower revenue growth in Q1 FY26 due to tariff issues, but the long-term picture looks positive. The company has grown for 19 straight quarters and management expects strong momentum by FY26 end. Its key growth drivers are :

- India, China and the US : India gives just 3-4%of revenue which is a big room to grow, while in China, KPIT is helping both Western and Chinese automakers.

- Off-Highway Vehicles : KPIT is entering segments like tractors, cranes and excavators which are small but fast growing.

- New Clients : Many high value clients are added recently from whom the revenue will be shown up by year end.

- Europe Opportunity : European carmakers need tech upgrades to compete with Chinese EVs from which KPIT will likely get benefits.

Valuation Analysis

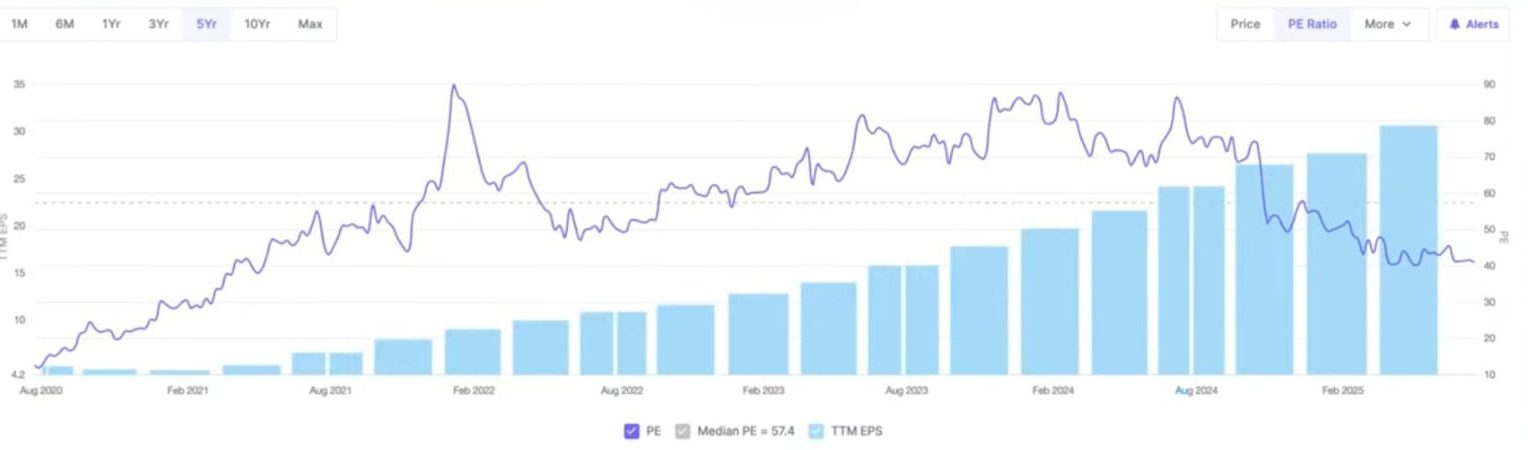

Evaluating KPIT’s stock requires more than just understanding its business, it’s equally important to assess whether the stock is fairly valued. One way to do this is by looking at its PE (Price-to-Earning) ratio in relation to its growth :

- At the time of its 2019 IPO, KPIT’s PE ratio was 27 (considered fair).

- Currently, the PE stands around 41, having previously touched a high of 90.

- The 43–45 PE range has historically acted as a resistance, with the stock rebounding upward multiple times.

Is it Overvalued ?

- KPIT has maintained strong growth: over 40% profit growth and 20%+ revenue growth.

- At a PE of 41, the stock appears fairly valued, given its consistent performance.

- It would seem overvalued only if growth slows sharply, which management guidance and past performance suggest is unlikely.

Based on current data we have read just now, KPIT does not appear overvalued.

Financial Health

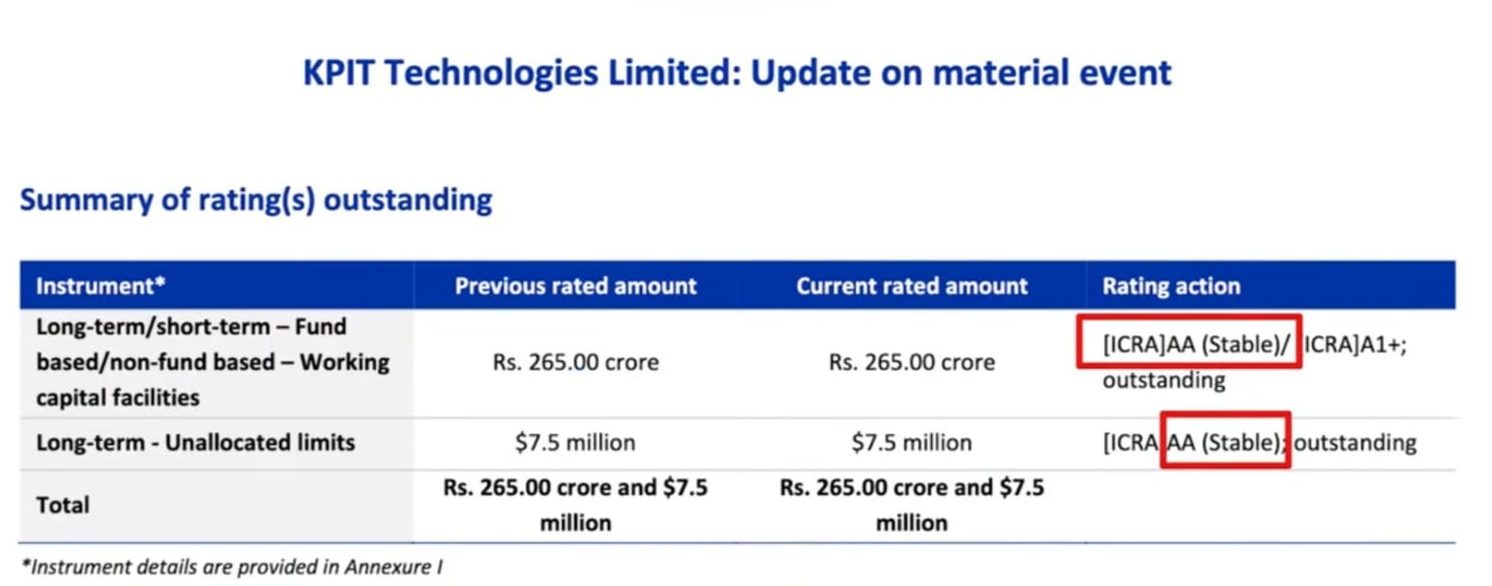

KPIT Tech has maintained an excellent financial health with a low debt-to-equity ratio of 0.12 and impressive interest coverage ratio of over 27. This means the company can manage its debt easily and has enough room to borrow for future growth if needed. ICRA has assigned the company an AA Stable credit rating, reflecting its robust financial position.

The shareholding pattern shows institutional confidence, with domestic institutional investors increasing their stake from 9% to compensate for reduced FII holdings which was 15%, indicating long-term confidence in the company's prospects.

Screenshot taken from Screener

A noteworthy detail is that MIT holds a 3% stake in the company, adding further credibility. Overall, KPIT’s financials remain strong and well-balanced.

Technical Analysis

Screenshot taken from Trading View

After a strong rally from June 2022 to October 2024, KPIT Technologies broke its upward trend and entered a correction. But now, that downtrend appears to be over. The stock is trading sideways, showing signs of stability almost like it's pausing before its next move.

Interestingly, the earlier resistance level is now acting as support. This shift often indicates a change in momentum and suggests that the worst might be behind.

On the indicator front, RSI has reversed from the 35 level, pointing to renewed strength. MACD is close to a buy signal and just needs a positive trigger. While the stock may not rally instantly, chances of a sharp fall look very low.

Golden Cross

In KPIT Tech Stock Analysis we will now see that KPIT is close to forming a Golden Cross which is a bullish technical signal where the 50-day moving average moves above the 200-day moving average.

This pattern usually suggests the start of a long-term uptrend. The gap between the two averages is narrowing, and once the crossover happens, it could confirm that the downtrend is over.

Interestingly, this has happened only twice before in KPIT- in Sep 2020 and Sep 2022 and both times, the stock rallied afterward. If history repeats, a third crossover may happen around Sep 2025.

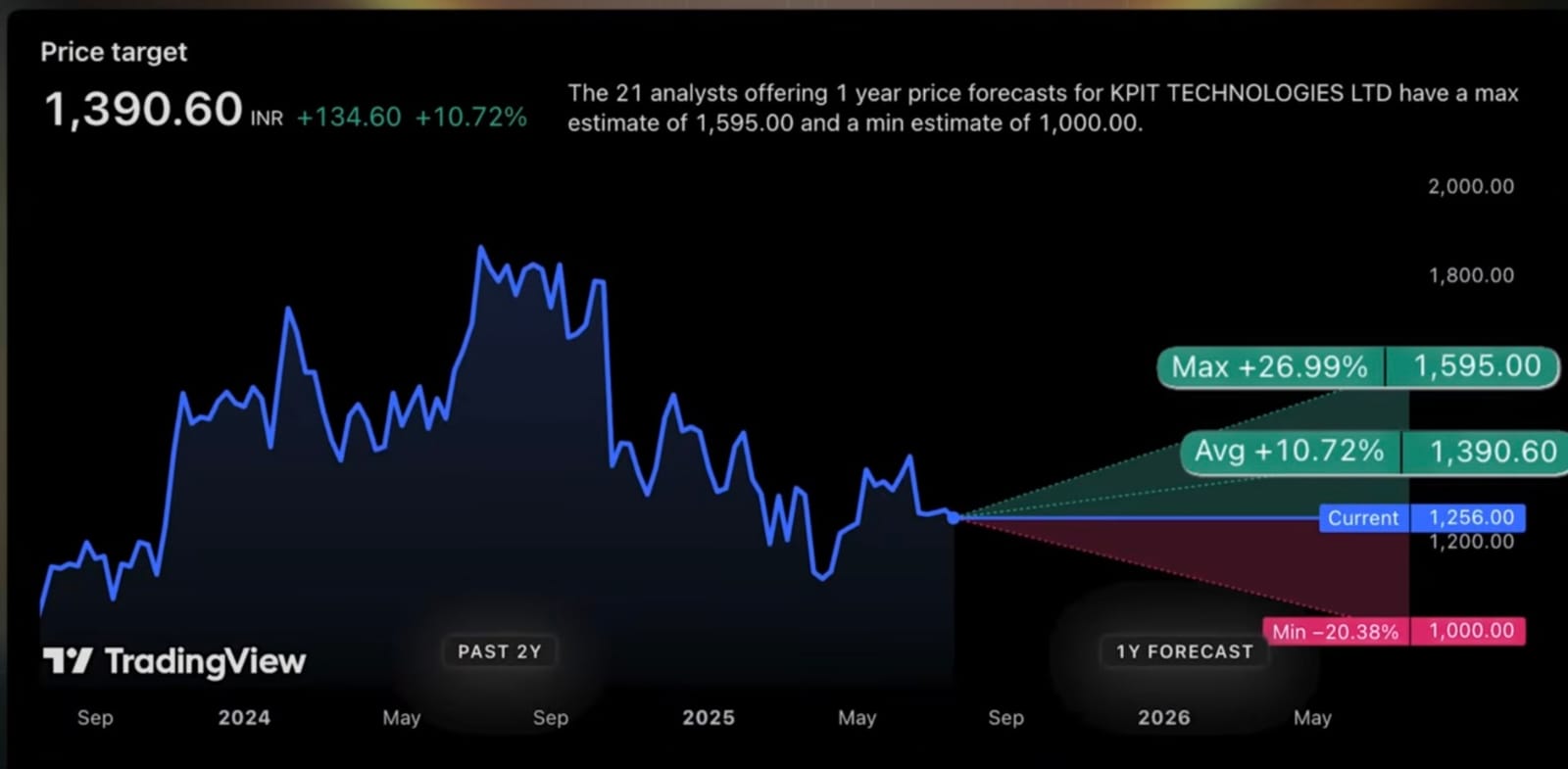

Analyst Ratings

KPIT Technologies has received positive reviews from top analysts in recent months:

- JPMorgan gave a 42% upside target (Dec 2024).

- Nirmal Bang issued a Buy on KPIT and Hold on Tata Elxsi.

- PL Capital also gave a fresh Buy call.

Overall, 50% of analysts rate it as a “Strong Buy”, with a 10–26% upside expected. Only one analyst sees a possible downside to ₹1000, but details are unclear. The sentiment across the board is largely bullish.

Dividend History

KPIT Technologies has maintained a 30% average dividend payout over the last 7 years, with a 0.67% yield. This is a healthy level for a mid-cap stock which is high enough to reward investors, but not so high that it signals a lack of growth opportunities.

The consistency reflects a stable and shareholder focused policy, making it attractive for long-term and retirement-focused investors. However, pure growth investors can skip this factor.

Myth Buster

Many investors still get confused between KPIT Technologies and the KP Group, which includes companies like KPI Green Energy and KP Energy. But this is a common misconception. Here's the truth:

- KPIT Tech is not related to KP Group in any way.

- KP Group is focused on the renewable energy sector, while KPIT Tech is a standalone software company that works mainly in the automobile sector.

- The similarity in names is purely coincidental, they are completely different businesses.

So if you had this confusion, now you know the facts.

Also Check - BSE Stock Analysis 2025

Conclusion

KPIT Technologies is quietly driving the future of connected, autonomous, and electric vehicles. With solid financial health, global partnerships, and entry into new growth areas like off-highway vehicles and China, it’s well-positioned for the long term.

While valuations are not cheap, consistent execution and strong earnings growth justify investor’s confidence. For those betting on the future of auto-tech, KPIT is a name worth watching.

Check Other Post Posts

-

WazirX Review: Is WazirX Legal in India or Not?

WazirX Review: Is WazirX Legal in India or Not?February 7, 2025

-

How Much Does Coindcx Charge for Withdrawal?

January 30, 2025

-

How to Set a Stop Loss on the Dhan?

April 3, 2025