InCred Money Review: Is InCred Money Safe?

InCred Money, operating under Alpha Fintech Private Limited, has emerged as a significant player in India's alternative investment space, offering users access to a range of instruments beyond traditional stocks and mutual funds. With over 1.5 lakh users and an Asset Under Management (AUM) exceeding ₹1,350 crore, it aims to democratize access to diverse investment opportunities. But for prospective users, the fundamental question remains: Is InCred Money safe, and what does it truly offer?

What is InCred Money?

InCred Money is an investment platform that facilitates intelligent investing in various asset classes. Unlike conventional brokerage platforms focused solely on listed equities, InCred Money specializes in alternative investments that can offer potentially higher returns, albeit with varying risk profiles. It's designed to provide a user-friendly interface for both seasoned investors and those new to these asset types.

Your Money on InCred Money: Is it Safe?

Image is generated through ChatGPT

Yes, your money is usually safe on InCred Money if you invest in low-risk and regulated products. For example, fixed deposits are placed with RBI-approved banks and are insured up to ₹5 lakh. Some market-linked debentures (MLDs) also protect your full investment amount and are rated by Crisil, a trusted rating agency. InCred Money is a legal and trusted platform registered with the RBI. However, the safety of your money depends on where you invest. Safer products = lower risk.

Trust and Regulation:

InCred Money states it is trusted by a significant user base and has a track record of 100% on-time payments. While InCred Financial Services Limited, the parent entity, holds a Certificate of Registration from the Reserve Bank of India (RBI) as an NBFC, it's crucial to understand that InCred Money and its representatives are explicitly stated to be not SEBI-registered research analysts or advisors. This means any information provided on the platform does not constitute investment advice.

RBI Regulation for FDs:

Bank Fixed Deposits (FDs) offered on InCred Money are RBI-regulated and insured by the DICGC (Deposit Insurance and Credit Guarantee Corporation), a wholly-owned subsidiary of the RBI, up to ₹5 lakh per bank, per depositor. This provides a significant layer of safety for funds invested in FDs.

Data Security:

InCred Money states it employs suitable physical, electronic, and managerial procedures to safeguard user information and prevent unauthorized access or disclosure. They restrict access to personal information between their servers and the internet, avoiding clear text transmission. However, like any online platform, they acknowledge that no method of transmission or storage is 100% secure.

Transparency & Risk Disclosure:

The platform provides information on the risks associated with various asset classes, particularly unlisted shares. For instance, it clearly states that unlisted shares have limited liquidity and are subject to market and price risk, often requiring longer lock-in periods.

Zero Defaults (Claimed):

InCred Money claims to have zero defaults to date on the instruments offered through its platform. This is a significant claim and, if consistently maintained, builds user confidence.

Potential User Concerns:

Customer Support Challenges:

Some user reviews have reported difficulties in connecting with customer support, with unresponsive phone numbers. Prompt and effective customer support is crucial for financial platforms.

Pricing of Unlisted Shares:

There have been user complaints about unlisted shares being sold at potentially higher prices on the platform compared to other brokers, and the risk that such shares might not list or list at a lower price than the purchase price.

Nature of Alternative Investments:

While InCred Money aims to make alternative investments accessible, it's vital for users to understand that instruments like unlisted shares, market-linked debentures (MLDs), and some bonds inherently carry higher risks than traditional FDs or publicly traded large-cap stocks. Due diligence and understanding the specific risks of each investment are paramount.

Login Requirements

To access InCred Money's services, users typically need to:

- Register: Sign up using their mobile number.

- OTP Verification: Verify their mobile number via a One-Time Password (OTP).

- KYC Completion: Complete their Know Your Customer (KYC) process, which usually involves providing:

- PAN Card details

- Address Proof

- Bank Account Details and proof (e.g., cancelled cheque)

- Other personal information as required by regulatory guidelines.

Features of InCred Money

InCred Money offers a diverse set of features aimed at simplifying alternative investments:

Diverse Investment Opportunities:

Pre-IPO / Unlisted Shares:

Invest in shares of companies before they go public.

Example: You could invest in a promising tech startup's unlisted shares through InCred Money, hoping for significant returns if it eventually lists on an exchange at a higher valuation (e.g., investing in "Imagine Marketing Ltd (Boat)" or "Tata Capital Ltd" unlisted shares).

Bonds:

Invest in debt securities issued by corporations, offering fixed periodic interest payments.

Example: Investing in a corporate bond through InCred Money that offers 10-12% p.a. fixed returns.

Market Linked Debentures (MLDs):

Hybrid investment options where returns are linked to the performance of an underlying market index (e.g., Nifty 50). They can be principal-protected or non-principal protected.

Example: Investing in an MLD where your returns are tied to the Nifty 50's performance, with a minimum assured return of, say, 14% and a maximum of 30%.

Fixed Deposits (FDs):

Offer a range of bank FDs with competitive interest rates (up to 9.10% as per recent reports), with a paperless investment process.

Example: Booking an FD from a bank via the InCred Money app to earn higher interest than traditional bank branches, with DICGC insurance up to ₹5 lakh.

Digital Gold:

(Recently added feature) Allowing investment in digital gold, powered by MMTC-PAMP.

Accessibility:

InCred Money aims to break down traditional barriers to entry for certain alternative investments. For instance, they allow users to invest in unlisted shares with very small minimums, sometimes as low as just "one share." It allows investors to start with smaller amounts and gradually build their exposure to alternative assets, making it less intimidating for newcomers.

Zero Fees/Brokerage:

InCred Money explicitly states that it charges "zero fees, charges, or brokerage for all instruments" on its platform. This is a significant claim that can enhance the net returns for investors, as transaction costs can otherwise eat into profits. A zero-fee structure aims to provide transparency, ensuring that the returns quoted are what the investor primarily receives, without hidden deductions.

Expert Guidance:

Given the often complex nature of alternative investments like MLDs and unlisted shares, the platform states it offers access to a "dedicated team of financial experts." This guidance simplifies the investment process, helps users understand the intricacies of different products, and provides information to aid in making informed investment decisions.

Referral Rewards:

InCred Money offers referral rewards, allowing existing users to earn benefits (e.g., vouchers or cashbacks) by referring new users to the platform. This strategy encourages word-of-mouth marketing and helps the platform expand its user base efficiently, leveraging its existing customer network.

Anytime Liquidity (for MLDs):

For Market Linked Debentures (MLDs), InCred Money offers a unique "Anytime Liquidity" feature, which allows investors to exit their investments before the stated maturity period. This addresses a common concern with debt instruments which are often illiquid.

Benefits of Using InCred Money

Diversification into Alternate Assets:

InCred Money offers investment avenues that standard brokerage platforms typically don’t provide, going beyond just stocks and mutual funds. This includes instruments like unlisted shares (Pre-IPO), corporate bonds, and Market Linked Debentures (MLDs). This diversification can help lower risk during periods of volatility in traditional asset classes and potentially enhance long-term returns.

Potentially Higher Returns:

Alternative investments often come with the potential for higher returns compared to conventional fixed-income options like bank FDs or even some traditional equity investments, especially in a low-interest-rate environment. Corporate bonds and MLDs offered on the platform can provide more attractive interest rates or returns compared to typical bank deposits.

Convenience:

The platform emphasizes a fully digital and paperless investment journey, making it easy to onboard and execute transactions from anywhere. By completing the Know Your Customer (KYC) process in just minutes, InCred Money significantly reduces the friction of getting started.

Expert Support (Claimed):

InCred Money states it provides access to a dedicated team of financial experts. This can be particularly beneficial for users who are new to complex alternative investments, as it offers a resource for understanding product details and making more informed decisions. The experts help simplify the nuances of these instruments, making them more approachable for the average investor.

DICGC Insurance for FDs:

RBI-regulated banks accept the Fixed Deposits booked through InCred Money, and the Deposit Insurance and Credit Guarantee Corporation (DICGC) insures them. This insurance covers deposits up to ₹5 lakh per bank per depositor, providing a crucial layer of capital protection and peace of mind against potential bank failures.

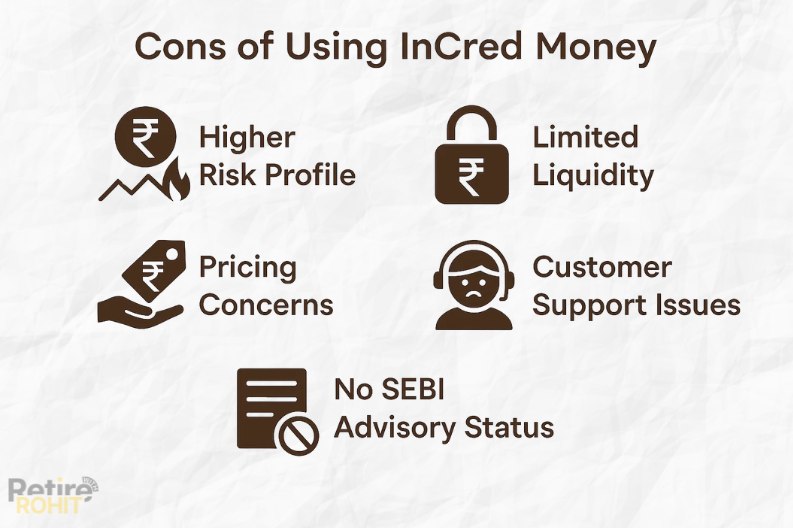

Cons of Using InCred Money

Image generated through ChatGPT.

Higher Risk Profile:

Many of the instruments offered, such as unlisted shares and Market Linked Debentures (MLDs), are inherently riskier than traditional, publicly traded securities like large-cap stocks or bank fixed deposits. These assets can experience greater price fluctuations and are more susceptible to market risks, economic conditions, and company-specific factors that are less transparent than for listed companies.

Limited Liquidity:

Specific platforms or brokers trade unlisted shares over-the-counter, unlike listed shares that trade on stock exchanges. This means there isn't a readily available, active market. Finding a buyer for unlisted shares quickly or at your desired price can be challenging. This can lead to holding periods much longer than anticipated, tying up your capital.

Pricing Concerns:

Given the absence of a regulated exchange for unlisted shares, there's less transparency in price discovery compared to listed securities. Some users and market observers have raised concerns that sellers on such platforms might significantly mark up the prices of unlisted shares beyond their intrinsic value or the prices available through other channels. This can reduce the potential for capital appreciation even if the company performs well.

Customer Support Issues:

Several user reviews have indicated difficulties in reaching InCred Money's customer support through phone or email, with reports of delayed or no responses. For financial investments—especially those involving higher risks and less transparency—responsive and effective customer support plays a critical role. It helps address queries, resolve issues, and provide necessary information in a timely manner.

No SEBI Advisory Status:

Users must remember that InCred Money is not a SEBI-registered advisor. Investment decisions should be based on independent research and understanding of the associated risks, or consulting with a qualified, independent financial advisor.

Conclusion

InCred Money offers Indian investors access to alternative investments like unlisted shares and corporate bonds, alongside RBI-regulated FDs, touting a paperless process and zero defaults. While providing diversification and potentially higher returns, users must acknowledge the inherent higher risks of alternative assets. Also, that InCred Money is not a SEBI-registered advisor. Despite efficiency efforts, customer support and unlisted share pricing have raised user concerns.

Ultimately, InCred Money can be a valuable tool for experienced investors seeking diversification and potentially higher returns. New or less experienced investors should thoroughly research, understand their risk profiles, and consider consulting an independent financial advisor.

Check Other Post Posts

-

Leave Encashment: A Comprehensive Guide

Leave Encashment: A Comprehensive GuideJanuary 25, 2024

-

How To Withdraw Funds From Fyers?

February 7, 2025

-