Gold vs Stocks: Why Gold Cannot Outperform Stocks Forever

Many investors today feel that gold only goes up and will continue to beat the stock market forever. In the debate of Gold vs Stocks, this belief raises important questions about how wealth is actually created. But if that ever became permanently true, it could actually signal a serious problem for the global economy.

This may sound surprising, but there's a strong financial logic behind it.

Gold Is Rising Fast - But That Doesn't Mean It Always Will

The current rise in gold prices looks powerful and unstoppable. However, just because gold is running up today does not mean it will crash tomorrow. What it does suggest is that when gold eventually corrects, it could go through a long period of flat or declining prices, similar to what happened after 2012.

The key point is simple: Gold and silver can never become "forever rising assets." If they did, the entire structure of capitalism and economic growth would be at risk.

Gold vs Stocks: Value Storage vs Value Creation

When you buy shares of a company, you are investing in a business that earns money. That company generates profits, pays dividends, reinvests earnings, and creates new economic value.

Gold, on the other hand, does none of that.

- It does not produce income.

- It does not innovate.

- It does not grow earnings.

Gold only stores existing value.

This leads to a crucial financial rule: Assets that do not create value cannot permanently outperform assets that do.

- Stocks are productive assets.

- Gold is a non-productive asset.

No economy - whether India, the US, or any other country - can escape this rule in the long run.

Watch Our Video on Gold vs Silver vs Stock Market

What Happens If Gold Always Beats Stocks?

Imagine a world where gold outperforms equities every decade.

- Why would anyone invest in companies?

- Why would anyone take business risks?

The result would be:

- No risk → No innovation

- No innovation → No jobs

- No jobs → No income

- No income → No taxes

- No taxes → No government spending

In short, the economic system would break down. That's why the financial system is built in a way where, over the long term, productive assets must outperform metals.

Gold Rises Because of Fear

Gold usually rises during times of uncertainty and fear:

- High inflation

- Weak currencies

- Wars or geopolitical tensions

- Falling trust in governments or financial systems

Right now, many of these conditions exist globally. But here's the twist: A rising gold price is often a panic signal - not a sign of economic strength.

When stock markets stabilize and confidence returns, gold usually calms down or moves sideways.

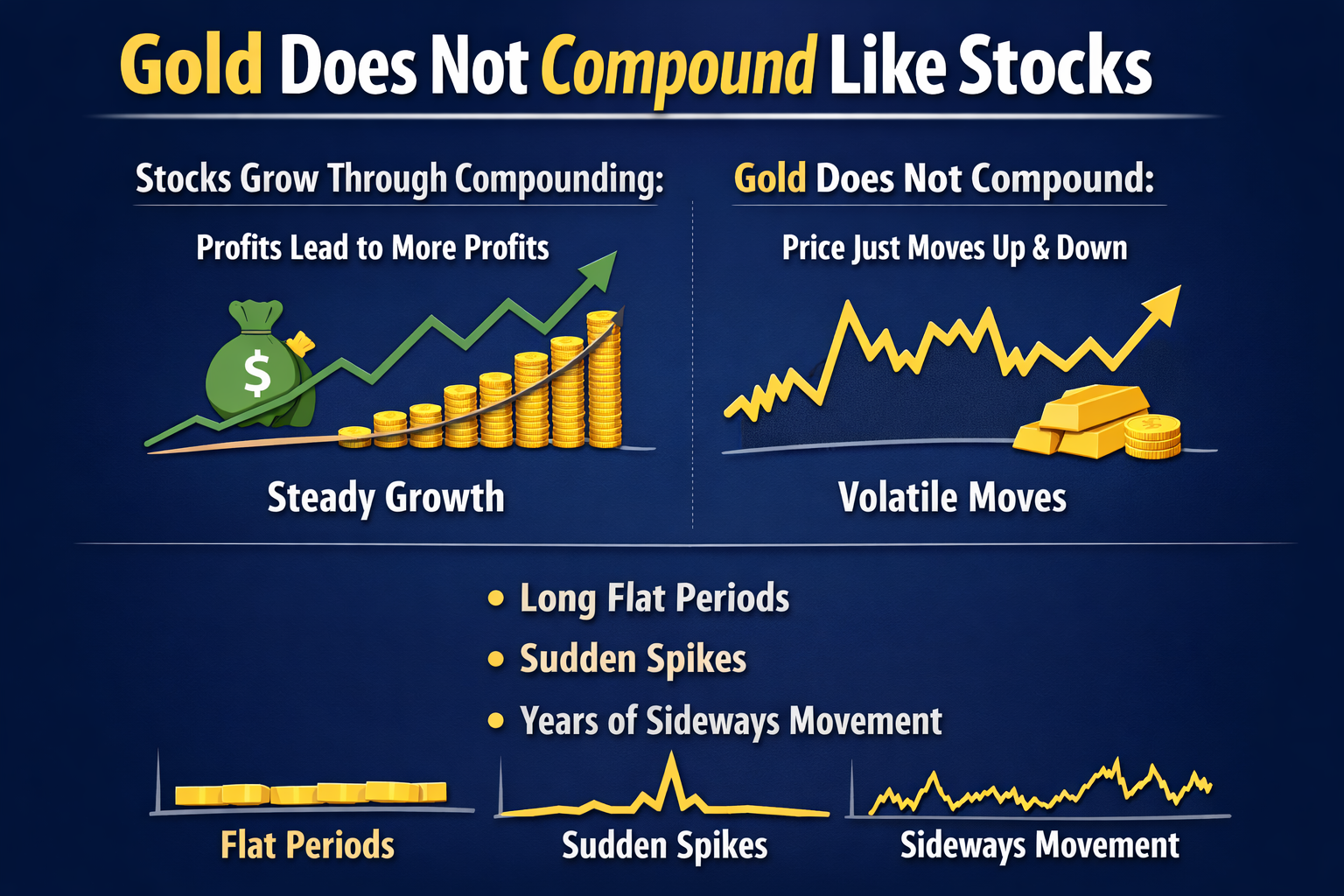

Gold Does Not Compound Like Stocks

- Stocks grow through compounding.

- Profits lead to more profits.

- Gold does not compound.

- Its price simply moves up and down.

That's why gold charts often show:

- Long flat periods

- Sudden spikes

- Years of sideways movement

For example, between 1980 and 2005, gold delivered almost zero real returns, while stocks created wealth and helped economies grow.

This cycle has repeated before and is likely to repeat again.

Why Central Banks Buy Gold

Yes, central banks have been buying gold. But not because it delivers the best returns.

They buy gold for:

- Currency diversification

- Reducing dependence on the US dollar

- Geopolitical insurance

Gold is a backup asset, not a growth engine. If gold ever became the main asset of central banks, monetary policy would lose effectiveness.

Even the US Federal Reserve holds gold as a small part of its assets, while the main drivers of the economy remain securities, loans, and liquidity tools - not gold.

Silver: More Volatile Than Gold

Silver is often called the "poor man's gold," but it is actually very different.

Silver has two roles:

- Precious metal

- Industrial commodity

Its demand changes quickly with economic conditions, and supply can also increase rapidly. This makes silver extremely volatile, with sharp price spikes and crashes.

Recent ETF flows have further distorted silver demand, temporarily tightening supply and pushing prices higher, only to risk sharp falls if those flows reverse.

Gold Protects Wealth - Stocks Multiply Wealth

Over 100 years of global data shows:

- Equities have delivered around 6-7% real returns

- Gold has delivered around 0-1% real returns

This means:

- Gold protects wealth from inflation

- Stocks grow wealth beyond inflation

Gold should be part of a portfolio - but as a hedge, not as the main long-term growth asset.

Conclusion

If gold were to outperform forever, innovation would slow, risk-taking would disappear, and global growth would suffer.

That's why gold's current rise cannot continue endlessly. Global uncertainty may keep gold strong for some time, but eventually, confidence and growth assets must take the lead again.

So hold gold and silver - but understand why you are holding them. And don't lose faith in equities, the real engines of long-term wealth creation.

Check Other Post Posts

-

How to Link Your Aadhaar with Your SBI Bank Account?

How to Link Your Aadhaar with Your SBI Bank Account?November 23, 2024

-

How to Do Intraday Trading On Groww App?

January 15, 2025

-

What is BO ID in Groww?

January 17, 2025