BSE Stock Analysis 2025: More Growth Ahead?

Imagine a stock that’s already doubled and then climbs another 75% within a year, while still being called undervalued by many investors. That stock is BSE (Bombay Stock Exchange). On 3rd October 2024, BSE was trading at ₹1400 which is its all time high after delivering 200% returns.

Everyone thought that ₹1400 was its peak but this stock kept on surprising everyone and has grown another 75%, though it’s currently down 20% from its peak. Let's dive deep into whether this exchange giant can justify its premium valuation and deliver exceptional returns through our detailed BSE stock analysis.

Growth Engine

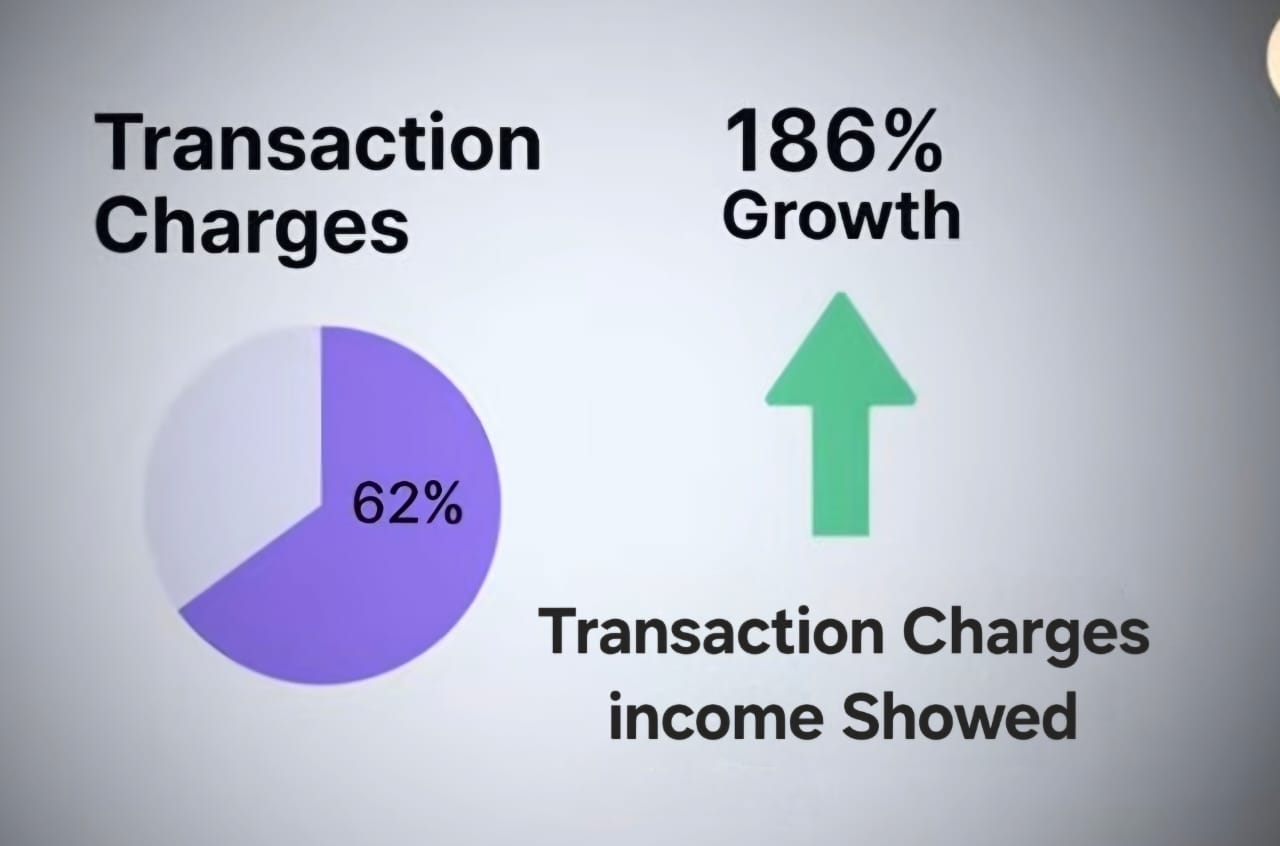

Our BSE stock analysis reveals that BSE isn’t just a stock exchange, it’s a diversified financial services company. BSE's revenue doubled in FY25 to ₹3,236 crore, primarily driven by a 186% surge in transaction charges, contributing 62% of revenue.

This growth is fueled by increased trading in equities, derivatives (F&O), and mutual funds, especially the popularity of Sensex option trading. With India's active stock market participation at just 5% (compared to 55% in the US), there's a 6x to 11x growth potential over the next 10-15 years, positioning BSE for sustained long-term growth.

India’s IPO Boom

A critical component of any thorough BSE stock analysis is understanding how the company profits from IPOs. BSE makes money from companies in two ways:

- One-time fees for IPO services and listing

- Recurring annual fees from all listed companies

For example, Nestle India pays ₹23 lakhs annually just to stay listed on BSE, while smaller companies like KPI Green Energy pay ₹3.26 lakhs yearly. This "Services to Corporate" income jumped 40% from ₹349 crores to ₹490 crores in just one year.

This revenue is recession-proof and companies rarely delist even during tough times. India's IPO activity has exploded from just 24 IPOs in 2015-16 to 78 IPOs last year. More companies going public means more listing fees and increased trading activity -which is a double win for BSE.

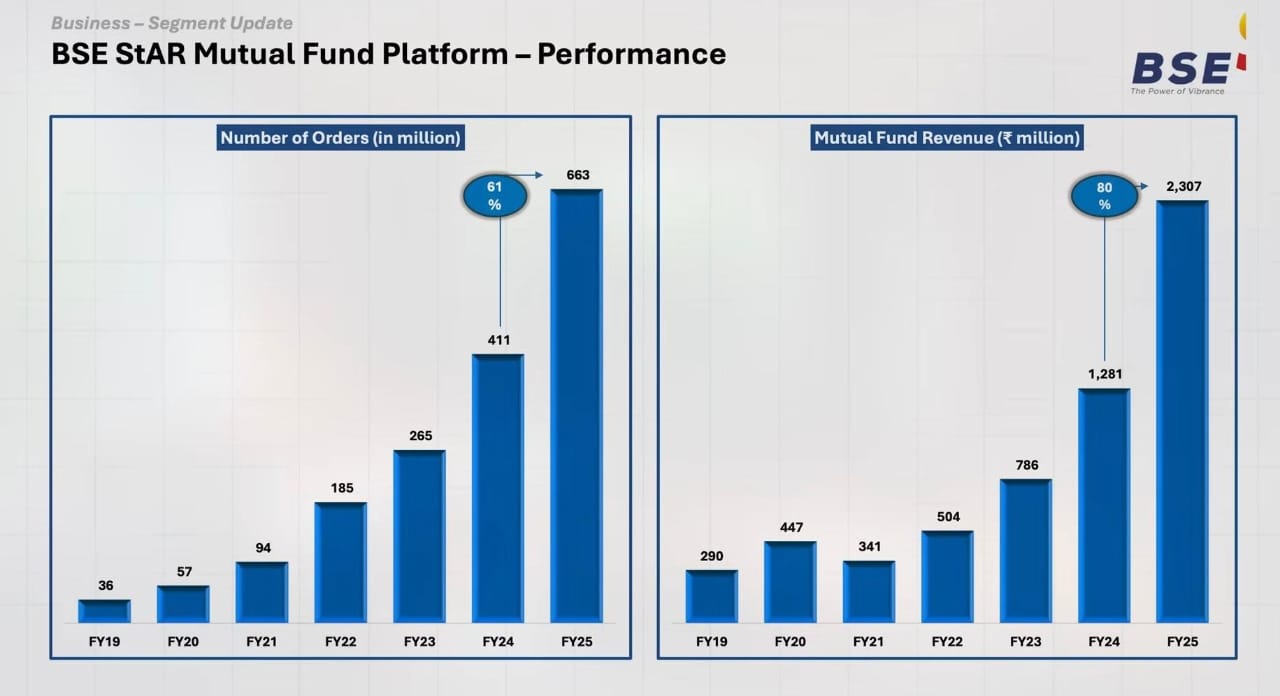

Mutual Fund Powerhouse

BSE Star MF (Mutual Fund) platform is quietly becoming a revenue powerhouse, contributing ₹230 crores (16 % of operating income) with 80% YoY growth.

The platform serves two Markets :

- Distributors and agents who sell mutual funds to clients

- Direct platforms like Groww that route mutual fund orders through BSE's backend

When you buy mutual funds on Groww, those orders actually flow through BSE's system. If BSE's platform goes down, Groww's mutual fund orders stop processing. That's the kind of critical infrastructure BSE has built.

Promoter Shareholding

Screenshot Taken from Screener

Don't panic seeing zero Promoter shareholding, its actually required by law. As a Market Infrastructure Institution (MII), BSE must be 100% publicly held without any promoter group. SEBI rules are strict :

- No single entity can own more than 5% (except government)

- Foreign entities can hold up to 15% with approval

- This ensures no single party controls critical market infrastructure

This isn’t a red flag, it’s regulatory compliance that ensures market integrity.

When Can BSE’s Growth Slow?

BSE’s core revenue comes from transaction charges on trading and mutual fund activity. But during market downturns—like recessions, wars, or pandemics—volumes drop, directly impacting earnings.

Its corporate services (like IPO and listing fees) provide some stability, especially annual listing fees, but this segment contributes just 16.7% of total revenue.

BSE also earns ~₹270 crore from investments and margin money interest, though this too is partly market-linked. It holds a 15% stake in CDSL, but dividend income is minimal.

BSE’s performance is tied to market activity. In downturns, profits may fall—but for long-term investors, that’s often the best time to enter.

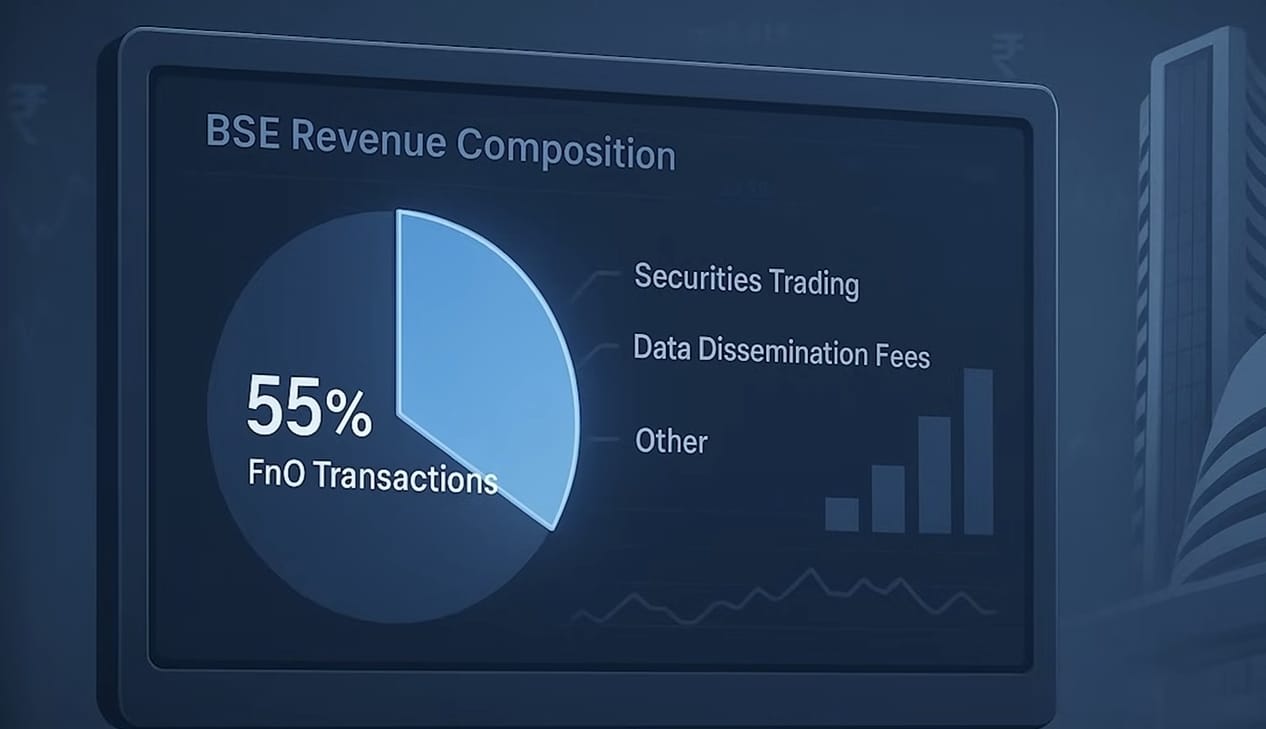

The F&O Opportunity And Risk

F&O trading is now BSE’s biggest money-maker. In the last quarter alone, 55% of BSE’s income came from derivatives trading. But SEBI is increasingly tightening regulations on FnO, due to high retail losses.

Recent changes include:

- Restricting weekly expiries to one index only

- Potential move from weekly to fortnightly expiries

- Frequent rule changes creating uncertainty

F&O regulations will continue evolving, creating volatility in BSE's stock price.

Valuation of BSE

Our detailed BSE stock analysis reveals that BSE trades at a sky-high PE ratio of 78, while NSE trades at 45. Both are overvalued by traditional metrics, but here's the context from our BSE stock analysis:

BSE's growth track record:

Screenshot taken from Screener

- 64% CAGR profit growth over 5 years

- 40% CAGR revenue growth

- 116% CAGR stock price growth

The stock price has grown twice as fast as profits, indicating inflated expectations. However, our BSE stock analysis shows that high-growth Indian stocks often stay overvalued for 5-6 years while fundamentals catch up.

If BSE's profit growth slows to 30% CAGR over the next 5 years while delivering 12% annual returns, the PE would normalize to 37. After 10 years of sustained growth, it could reach a reasonable PE of 17.

NSE vs BSE

NSE holds the title of the largest stock exchange in India, whereas BSE is recognised as the oldest one.

| Metric | NSE | BSE |

| Market Cap. | ₹5 Lakh Crore | ₹1 Lakh Crore |

| Annual revenue | ₹17,000 Crore | ₹3,000 Crore |

| PE Ratio | 45 | 78 |

| 5 yrs Profit CAGR | 45% | 60% |

| Valuation Outlook | Overvalued | Overvalued |

Technical Analysis

BSE’s short- to mid-term trend, starting from August 2023, shows strong upward momentum. It briefly moved above its trend channel but has now returned to it, turning past resistance into support.

If the stock continues in this range, it could reach ₹4,600 – ₹5,500 by 2030, implying 12–15% CAGR. This aligns well with the fundamental growth story.

While longer-term indicators like RSI or MACD aren't reliable due to limited history, price action suggests steady strength and consolidation.

Investment Strategy

Despite being overvalued, our comprehensive BSE stock analysis concludes that BSE (and NSE) represent a 10-year growth story tied to India's financial market evolution. The strategy emerging from our BSE stock analysis:

- Small, regular investments rather than lump sum.

- Wait for corrections to increase position sizes.

- Target 3% portfolio allocation combined with NSE.

- Think long-term dividend income - BSE has paid dividends for 10 consecutive years.

For those preferring diversification, our BSE stock analysis suggests considering the Capital Market Index ETF, which includes BSE and other companies benefiting from India's growing market participation.

Also Check : Suzlon Energy Stock Analysis 2025

Conclusion

This BSE stock analysis reveals that the stock is fundamentally strong, richly valued, but packed with long-term potential. Whether it delivers 4x returns in 5 years depends on market growth, investor participation, and regulatory stability. But for long-term investors, BSE could be a worthy pick in India’s financial evolution story.

Check Other Post Posts

-

-

Bull Market vs Bear Market: Key Differences

May 2, 2025

-

SBI Securities Charges and Fees 2025

April 24, 2025