Apollo Micro Systems: Growth & Stock Outlook 2025

When it comes to investing in sectors that don’t go out of style, ‘defence’ is a renowned one. In today’s India, where geopolitical tensions never die down, the defence industry is not just necessary, it’s inevitable. The most recent ‘Operation Sindoor’ in May 2025 is a clear signal that India’s military readiness isn’t an occasional response, but a constant necessity.

And while the nation gears up, one company has been quietly cashing in. Its stock surged by 48% alone in 10 days, and counting. Meet Apollo Micro Systems Limited, the name that’s suddenly everywhere, but was never really nowhere.

What Makes Apollo Micro Systems Special?

Founded in 1985, Apollo Micro Systems is not a new kid looking to set its foot, it works for defence, aerospace, space, transportation, and even home and land security systems. It deals in software, intelligence and electronics used in defence & security devices, crafts & gadgets like control systems, sensors, guidance modules and embedded electronics.

A small-cap company that has set foot in the intelligence technology space has a focused, unique niche and works on it with regular clients. Here’s what sets it apart:

- Strategic Positioning in Defence Market: Unlike other defence sector industries that make tanks, aircraft and submarines, etc, Apollo Micro Systems makes the technology used in them.

- Unique Niche with High Entry Barriers: The Defence industry is not something anybody can enter. It requires- R&D department, long testing & certification cycles, supply chain discipline and classified access. And Apollo Micro Systems has done it slowly, taking years to build its name in the industry.

- Sticky Government Clients: The company doesn’t manufacture products that could lose clients over a 2% margin; it is based on performance, results and trust. It deals with DRDO, ISRO, Bharat Dynamics Limited, Indian Navy and many more long-term clients.

- Aligns with Make In India: Recently, the Indian government is aggressively pushing for defence self-reliance, and this company perfectly aligns with this whole concept and initiative.

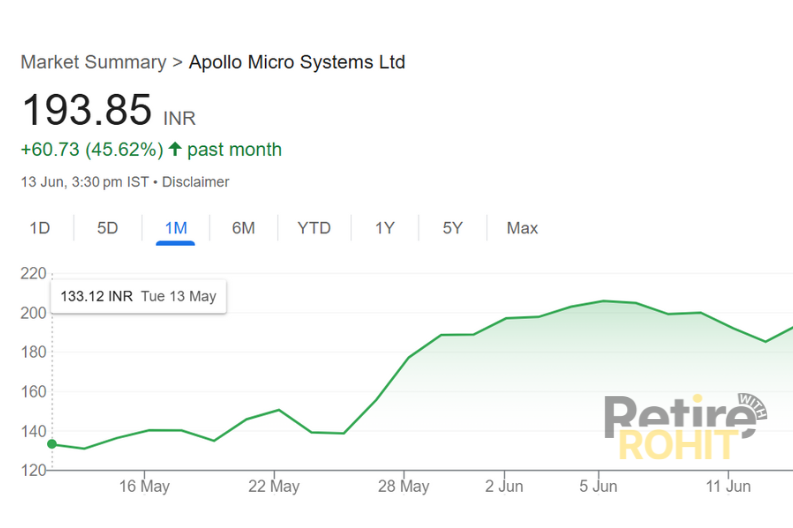

Image taken from Google Finance

Note: The above chart shows stock fluctuation of past 1 month, from 13 May to 13 June 2025.

Why Has This Stock Been Viral Recently?

A small-cap company that was not known to anyone just 5 years ago is now doing wonders on the stock market. Because of its massive growth rate, high returns and big acquisitions recently, the stock is creating a buzz.

- Strong performance: In FY25, the company reported the highest ever revenue of Rs. 562 crore, a 51% increase from the previous year. Its Net profit surged by 81% to Rs. 56 Crore. Just recently, it bagged a Rs. 113.81 Cr export order for avionic systems. The company’s great performance and financial growth have brought it into the spotlight.

- Expansion and Acquisition: Apollo Microsystem has been strategically expanding its business, diversifying it, from defence, aerospace, to transportation and home security systems, covering all. And on May 2, 2025, it acquired IDL Explosives Ltd. for 107 crores.

- High Returns: The stock is currently trading at 9.8 times its book value. It surged by 1400% in recent years and by 60% in May 2025 alone. The stock is offering very high returns, catching the eyes of many investors.

Returns in The Last Few Years

During the last decade, their sales grew by 19%, reporting a compounded profit growth of 23%. The company is strategically developing and expanding its areas. In FY25,

Highest ever revenue of Rs. 562.07 crores, representing a robust 51.24% year-on-year growth. Their revenue has been continuously increasing since 2021.

Net Profits surged by 81.18% to Rs. 56 crore, while OPM stayed steady at 23%.

After years of negative operating cash flow, it showed a slightly positive operating Cash flow of 12 crore, which is still less compared to net profits.

Debt-to-equity stands at 0.5; however, long-term borrowings jumped from 9 crore to 38 crore.

The Business Area and Moat

Apollo isn’t building the tanks or fighter jets, but the tech inside them. Think of Apollo as the brain behind the brawn. Here’s what that means:

- Embedded systems: Ever noticed how a microwave stops on its own when food’s done? It's because of a small chip inside, telling it what to do. Apollo makes those chips, not for microwaves, but for missiles, ships, and radars, so they can think and act on their own, just like that microwave.

- Avionics and control systems: Ever used Google Maps to reach a destination? Apollo builds similar tech, but for missiles and drones, helping them navigate and hit targets precisely, all on their own.

- Surveillance and tracking electronics: Apollo makes smart sensors that act like a security guard; they can spot movement, heat, or strange signals, and help the military keep an eye on what’s happening, even in the dark or bad weather.

- Ammunition components: they focus on adding electronics inside bombs or rockets that make sure they don’t explode too early or too late. Think of it like a timer on a microwave, but for defence weapons, where timings have to be perfect.

Their Moat Lies in:

- Specialised Certifications: You can’t just enter defence electronics with a soldering gun and ambition. You need years of credibility, certifications, and proven performance under mission-critical conditions.

- Customisation Capability: AMSL isn’t selling off-the-shelf gadgets. Each project is tailored, often in collaboration with agencies like DRDO.

- Localisation Push: India is quickly cutting down on defence imports, and that’s a big boost for Apollo, an edge most tech companies can only dream of.

Growth Areas

- Space and Aerospace: ISRO’s recent international missions and defence tie-ups are opening a high-value market for aerospace-grade electronics.

- Consumer Market: While defence is the core, many technologies, like surveillance systems or rugged embedded tech, can be adapted for use in railways, smart cities, and border infrastructure.

Vulnerabilities in the Business

- Valuation: At a current high PE, expectations are also sky-high. Any slowdown in earnings growth could bring the stock back to earth, fast.

- Dependence on Government Contracts: A change in defence budgets or a bureaucratic delay could hurt revenues. It’s not a free market, it’s government-driven.

- Execution Risk: Shifting from subcontractor to OEM (Original Equipment Manufacturer) is like going from manufacturing the micro parts to manufacturing the whole thing. It’s more rewarding, but the risks (and expectations) are far higher.

- Debt Load: The company has historically relied on short-term borrowings for working capital. While the recent fundraise helps, capital efficiency will be under the microscope going forward.

PE Ratio: Hype or Hope?

Apollo’s PE of 100+ is, by traditional metrics, extremely expensive. Most defence PSUs like Bharat Electronics or HAL trade at 30–50x. But here’s the thing, Apollo is in a different phase.

It’s growing faster, expanding into newer verticals, and getting a valuation not for what it is today, but what investors believe it could be three years from now. The market is betting on a story. But stories need results.

If the company misses a quarter or fails to bag a major contract, the valuation premium could vanish quickly. That makes it thrilling and dangerous.

Also check: HDFC Bank Stock Analysis, Asian Paints & Nestle India Update

Verdict: Overvalued or Undervalued?

Apollo Micro Systems Limited is currently overvalued on paper. But that’s not the whole story. It is priced like a future market leader in India's indigenous defence race. If it executes well, lands contracts, delivers on OEM ambitions, and scales smartly, then today’s price may seem cheap on retrospection.

However, if execution falters or growth stalls, the current valuation offers no margin of safety. This isn’t a buy-and-forget stock. It’s a “watch closely, research thoroughly, and invest with conviction” kind of play.

For long-term believers in India’s strategic manufacturing story, Apollo may just be one of the best small-cap opportunities out there. But tread with your eyes open. This one isn’t for the faint-hearted.

Check Other Post Posts

-

How to Apply for HDFC Bank Personal Loan?

How to Apply for HDFC Bank Personal Loan?November 11, 2024

-

Why MTF Is Only for Expert Short-Term Swing Traders

January 28, 2026

-

What is Beta in the Stock Market?

May 28, 2025