Dixon Technologies: India’s EMS Giant and Its Next Growth Story

Dixon Technologies is the largest EMS player in India. Understanding the Dixon Technologies Business Model helps explain how the company manufactures electronics for global brands rather than selling products under its own brand name. EMS stands for Electronics Manufacturing Services, where companies produce devices for major brands while those brands handle marketing and sales. Dixon manufactures and assembles products in India for companies such as Samsung, Xiaomi, Motorola, boAt, and Philips.

Currently, mobile phones contribute the largest share of Dixon's revenue. However, the company also operates across several other segments, including LED TVs, washing machines, refrigerators, smartwatches, telecom equipment, and IT hardware, making it a diversified electronics manufacturing partner.

Business Model

Dixon operates under two key business models: EMS and ODM.

- In the EMS model, the client provides the product design, and Dixon manufactures or assembles the final product.

- In the ODM model, Dixon designs and manufactures the product itself, which other companies later sell under their own brand names. Currently, ODM contributes only around 7% of total revenue. The company mainly produces products like washing machines and refrigerators under this model. However, expanding the ODM segment is important because ODM offers higher profit margins compared to standard contract manufacturing.

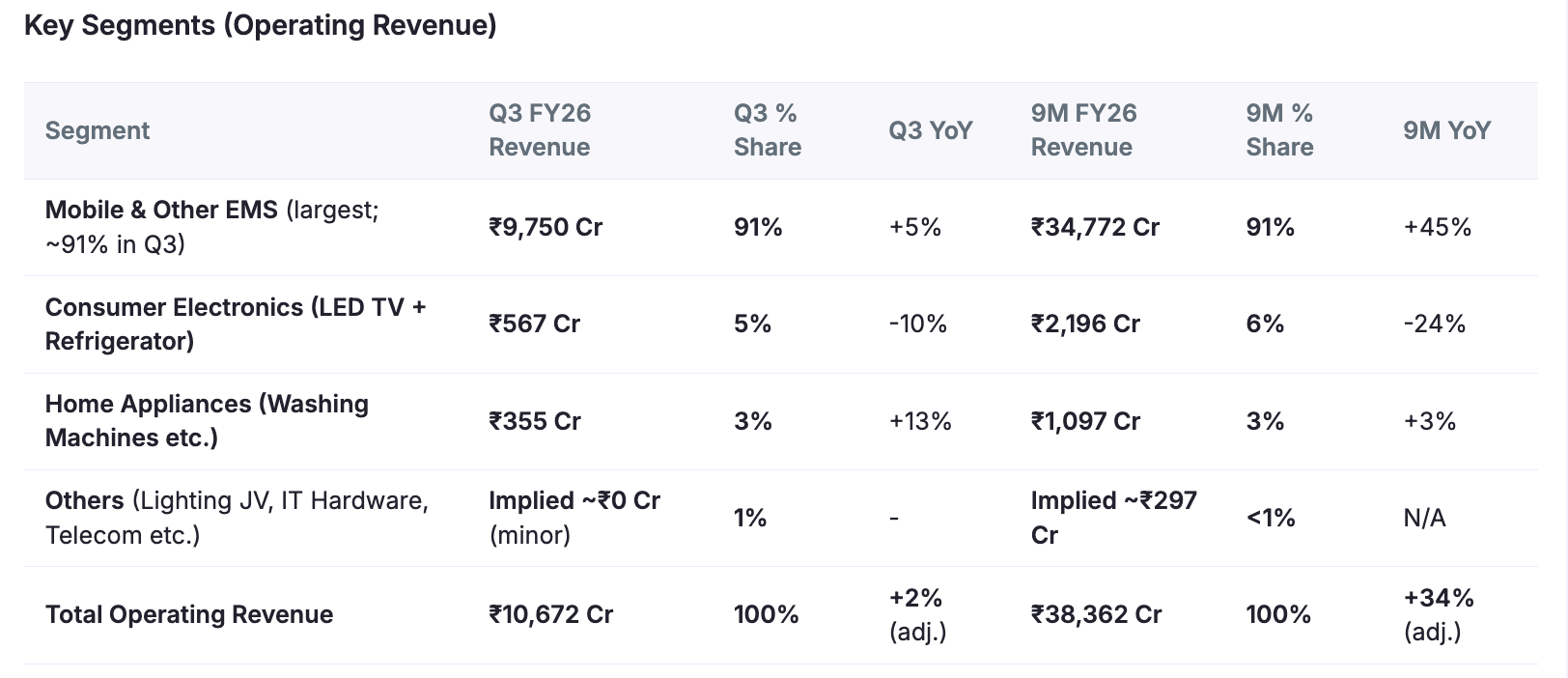

Segment-wise Revenue Contribution

The Mobile & Other EMS segment remains the dominant contributor, accounting for approximately 91% of total operating revenue, highlighting the company's strong positioning in the electronics manufacturing services (EMS) ecosystem. This segment has also recorded solid year-on-year growth, reflecting rising demand for outsourced electronics manufacturing.

In comparison, the Consumer Electronics segment, which includes LED TVs and refrigerators, contributes a relatively smaller share of revenue and has experienced a decline in year-on-year performance, indicating weaker demand or lower production volumes during the period. Meanwhile, the Home Appliances segment, including products such as washing machines, shows moderate growth, suggesting gradual expansion in this vertical.

Overall, the revenue mix indicates that the company's growth is primarily driven by the EMS segment, while other segments provide diversification but remain comparatively smaller contributors to the total operating revenue.

Historical Tailwinds That Boosted Dixon's Growth

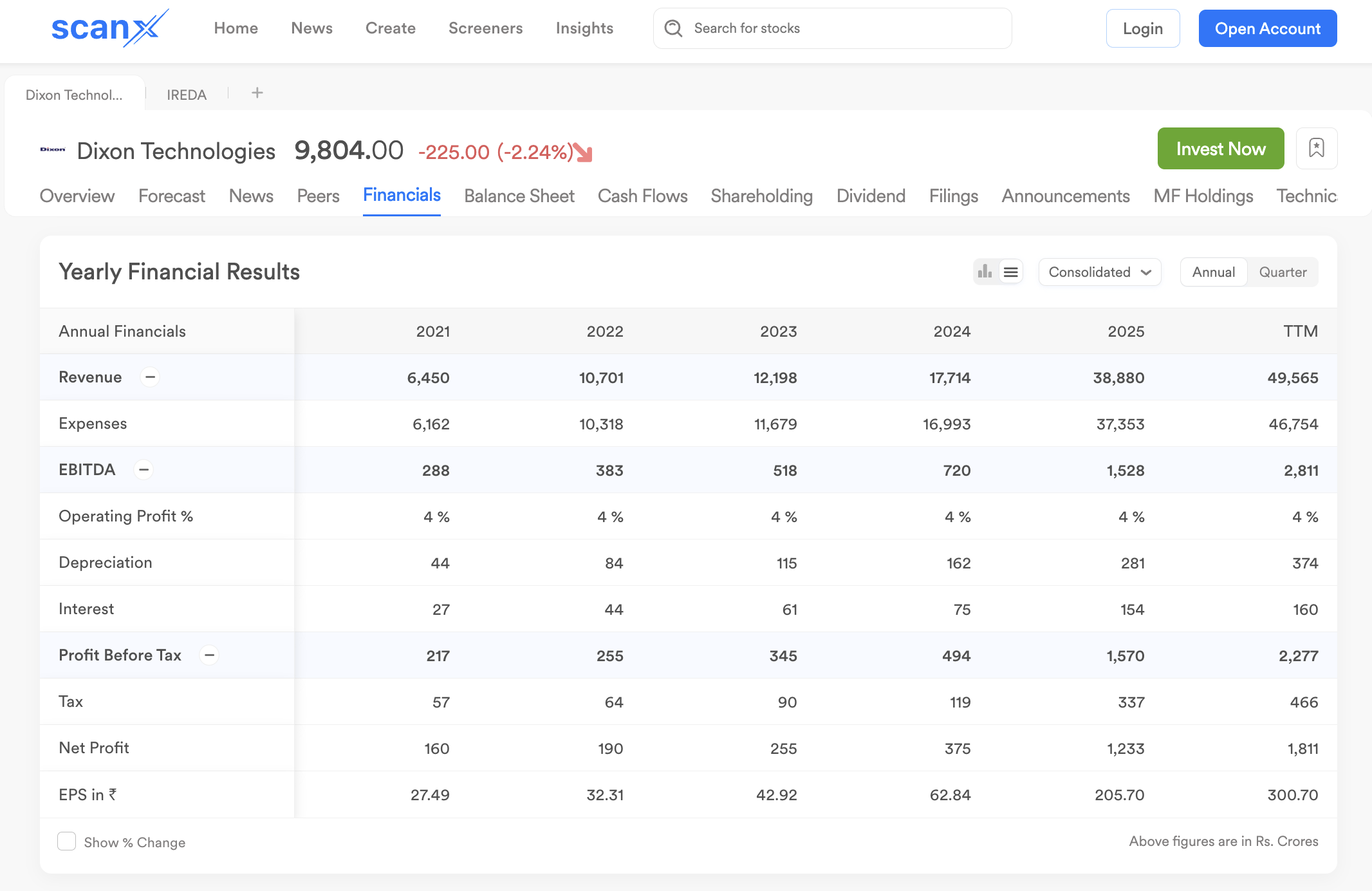

The years 2023 and 2024 were a golden period for Dixon Technologies. During this time, the stock price increased almost five times. One of the biggest reasons was the strong push for Make in India manufacturing. The government also introduced PLI schemes (Production Linked Incentives), which provided financial benefits to companies producing electronics domestically.

This supportive environment allowed Dixon to grow its revenue from about ₹10,000 crore to nearly ₹50,000 crore.

However, the industry landscape is changing now. Many new players have entered the EMS sector, increasing competition. Some major competitors include Tata Technologies, Karbonn, DBG Technology, Kaynes Technology, and PG Electroplast. Because of rising competition, Dixon may still grow, but achieving the 40-50% CAGR growth seen over the past five years will be difficult.

Increasing revenue from ₹10,000 crore to ₹50,000 crore means the business expanded five times. But growing from ₹50,000 crore to ₹1 lakh crore represents only two times growth, even though the absolute increase is larger.

Operational Strength and Financial Health

One of Dixon's biggest strengths is its negative working capital cycle. Currently, the company operates at around negative 7 days. This means Dixon receives payment from customers before paying suppliers. In simple terms, the company collects cash earlier than it needs to spend it, which improves liquidity.

Despite strong growth, profit margins remain a challenge for Dixon. Around 90% of revenue comes from the mobile EMS business, where the company acts as a contract manufacturer.

In this model, Dixon receives orders from smartphone brands, procures components like screens, chips, cameras, and casings, and assembles the final device. Margins in this business are extremely thin. The mobile EMS margin is roughly 3.5%, and about 0.5% of this comes from PLI incentives. Because of this, the company's EBITDA margin has remained around 4% for several years.

Another concern is that the PLI scheme is currently valid only until March 2026. If it is not extended, Dixon's operating profit could fall significantly, which might lead to negative stock market reactions.

Watch Our Video on Dixon Technologies

Moving Up the Value Chain

To address these challenges, Dixon's management has started moving up the value chain. Instead of focusing only on assembly, the company is now trying to manufacture high-value components used in smartphones.

One major initiative is the partnership with Q Tech to manufacture camera modules in India. The market for camera modules in India is estimated at around $350-$400 million, most of which is currently imported from China and Taiwan.

Dixon plans to supply camera modules to major Android brands like Samsung, Vivo, Oppo, and Motorola. The current production capacity is around 4 crore modules annually, with plans to expand it to 19-20 crore modules.

Another major step is a joint venture with HKC for display manufacturing. The facility being built in Noida will initially produce 2.5 crore smartphone displays and around 20 lakh displays for notebooks and automobiles.

Trial production is expected to begin by FY27. These initiatives can significantly improve margins and reduce dependence on imported components.

New Growth Engines for the Future

Since smartphone growth is slowing globally, Dixon is exploring new growth segments. One promising area is IT hardware and AI PCs. The company expects this segment to generate around ₹1,500 crore revenue this year, with a target of ₹3,500-₹4,000 crore next year.

Dixon has already started manufacturing laptops and desktops for global brands like HP and Asus. The company also plans to participate in the data center ecosystem by entering server manufacturing, which is a key component of modern digital infrastructure.

Dixon has partnered with Inventec in a 60:40 joint venture. This facility will produce SSD storage and memory modules, with production expected to begin around FY27. These products typically carry higher margins, which could improve overall profitability.

Management's Growth Vision

Dixon's management has set an ambitious goal: achieving ₹1 lakh crore revenue within the next four years. Rising demand for AI infrastructure and data centers is pushing up the prices of memory and RAM. This could increase the cost of entry-level smartphones, potentially affecting demand.

For Dixon, these cost increases are mostly pass-through costs, meaning they do not directly impact margins. However, if demand slows, revenue growth could still be affected.

Conclusion

Dixon Technologies remains a key player in India's electronics manufacturing ecosystem. While the company may not repeat the explosive growth of the past decade, its focus on component manufacturing, IT hardware, and new technology segments could unlock the next phase of growth.

For investors, the real opportunity lies not just in the existing EMS business but in Dixon's strategy to climb the value chain and diversify its revenue streams.