Impact of Previous Tax Hikes on ITC

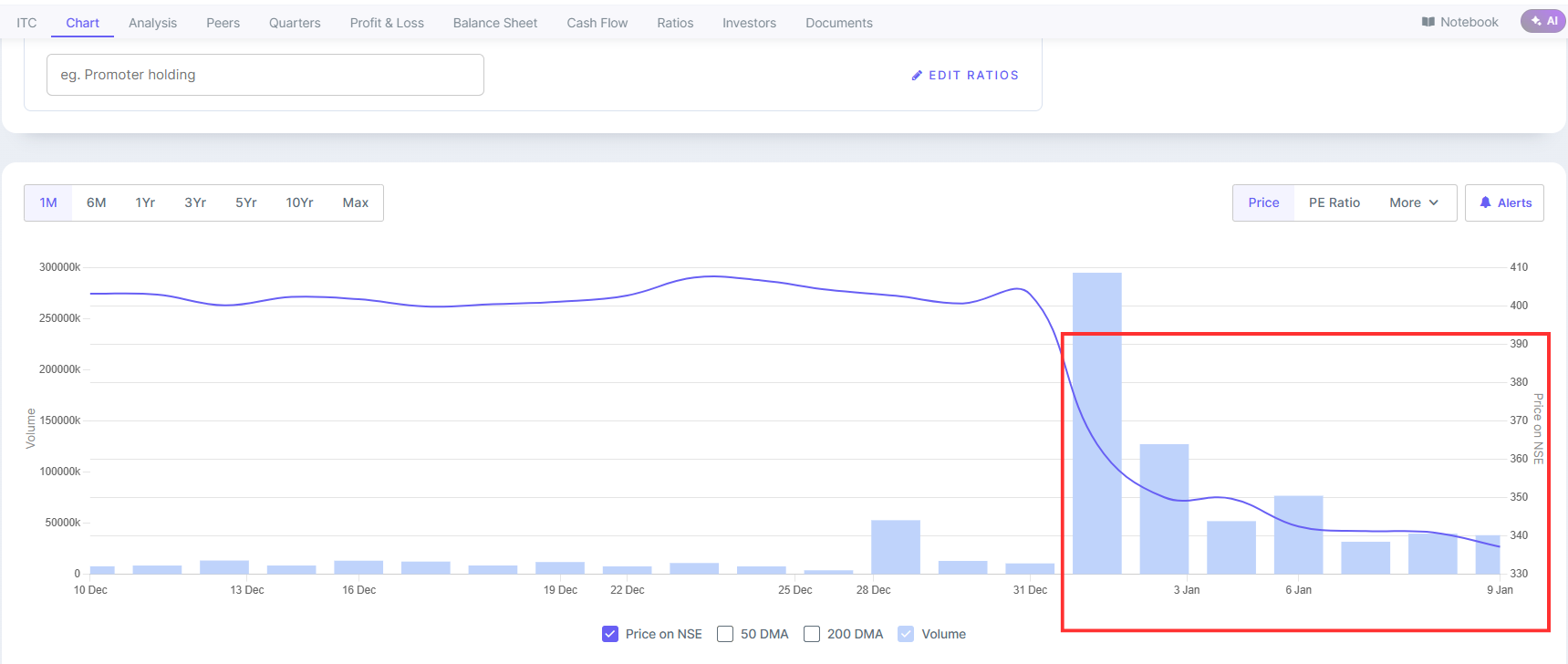

The government’s announcement to raise cigarette taxes from 1 February 2026 triggered an immediate and emotional reaction in the stock market. ITC, India’s largest cigarette manufacturer, saw its share price fall nearly 15% within four trading sessions, as investors revisited the impact of previous tax hikes on ITC and questioned whether history could repeat itself.

At first glance, the sell-off suggested that ITC's core business was under serious threat. However, market reactions to policy changes are often driven by fear rather than facts. To understand whether this correction is fundamentally justified, we need to examine how ITC has historically responded to similar tax hikes.

The New Cigarette Tax Explained

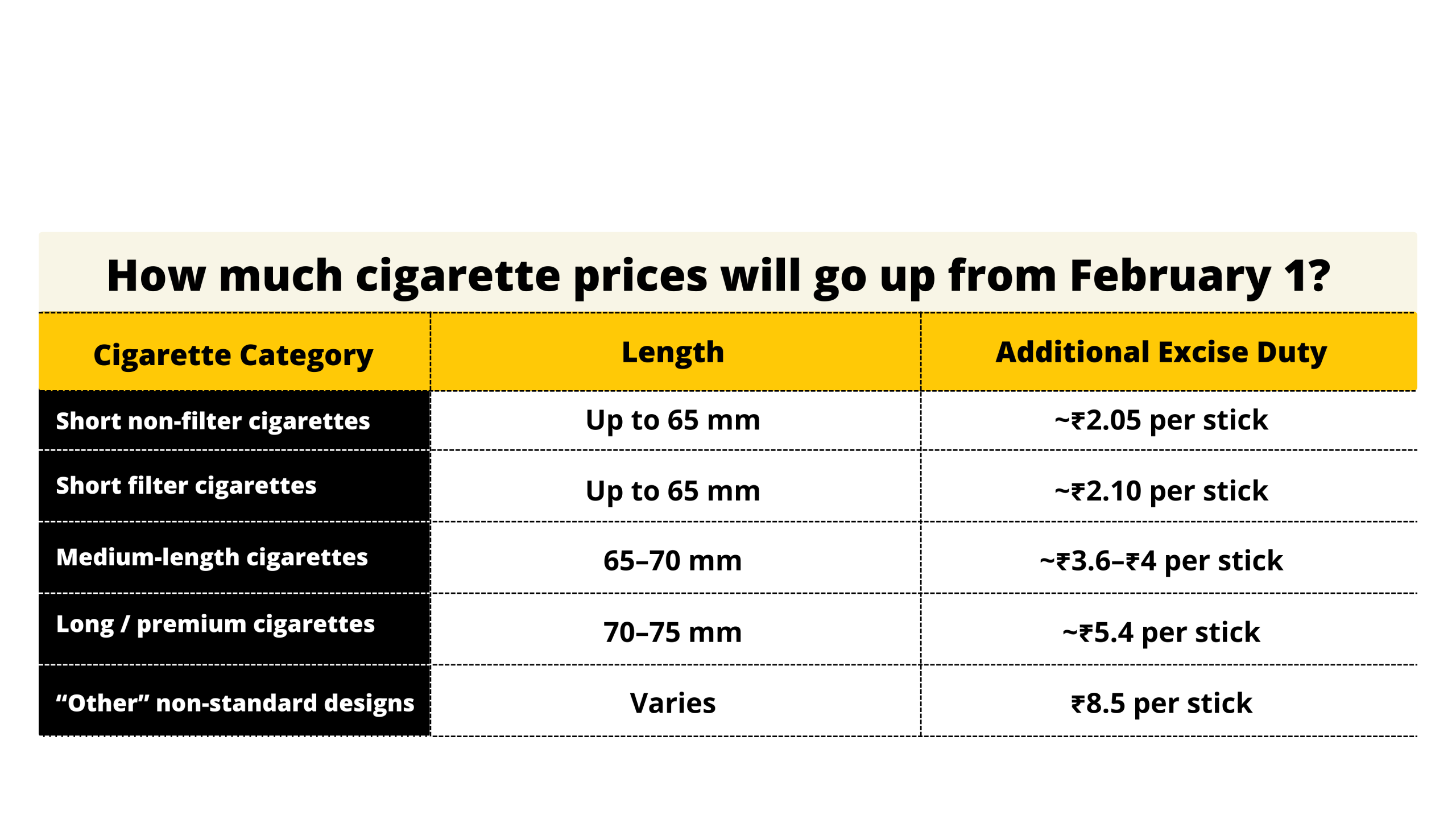

From February 2026, the government has changed the cigarette taxation structure by reintroducing excise duty in addition to GST. Earlier, cigarettes were taxed mainly through GST and compensation cess. Under the new framework, excise duty will be levied separately and will vary based on cigarette length and category, calculated on a per 1,000 cigarette basis.

This change is expected to increase the retail price of a single cigarette by ₹2-₹5. After the hike, nearly 50-55% of a ₹20 cigarette's price will go towards taxes.

Despite this increase, India's tobacco taxation remains below the World Health Organization's recommended level of 75%, indicating that high taxation is a structural feature of the industry rather than a one-off shock.

Will Higher Taxes Reduce Cigarette Consumption?

Concerns about falling demand naturally follow any tax increase. According to World Health Organization studies, nearly half of Indian smokers consume five or fewer cigarettes per day, while the average smoker consumes around 6.1 cigarettes daily.

The new tax increases daily spending by ₹10-₹40, translating into a monthly increase of ₹300-₹1,200. Informal surveys across social media platforms suggest that most smokers do not intend to quit, although a section may reduce consumption. This distinction matters because reduced consumption does not necessarily translate into a collapse in industry revenues.

What History Teaches Us: The 2015-2017 Tax Hikes

The most reliable way to judge the current situation is by looking at the past. Between 2015 and 2017, the government increased cigarette taxes repeatedly.

- In 2015, excise duty rose by 15-25%, pushing cigarette prices up by roughly 10%

- In 2016, another 10-15% increase was introduced

- In 2017, compensation cess was increased further

This resulted in cigarette prices rising consistently for five to six consecutive years.

An analysis of ITC's annual reports from 2015 to 2018 shows that cigarette revenues declined only marginally during this period. More importantly, profitability remained largely unaffected. While volumes softened slightly, the business did not face any structural damage. Consumers adjusted behavior, but demand did not disappear

Watch Our ITC Stock Analysis Video

ITC Then vs ITC Now: A Structural Shift

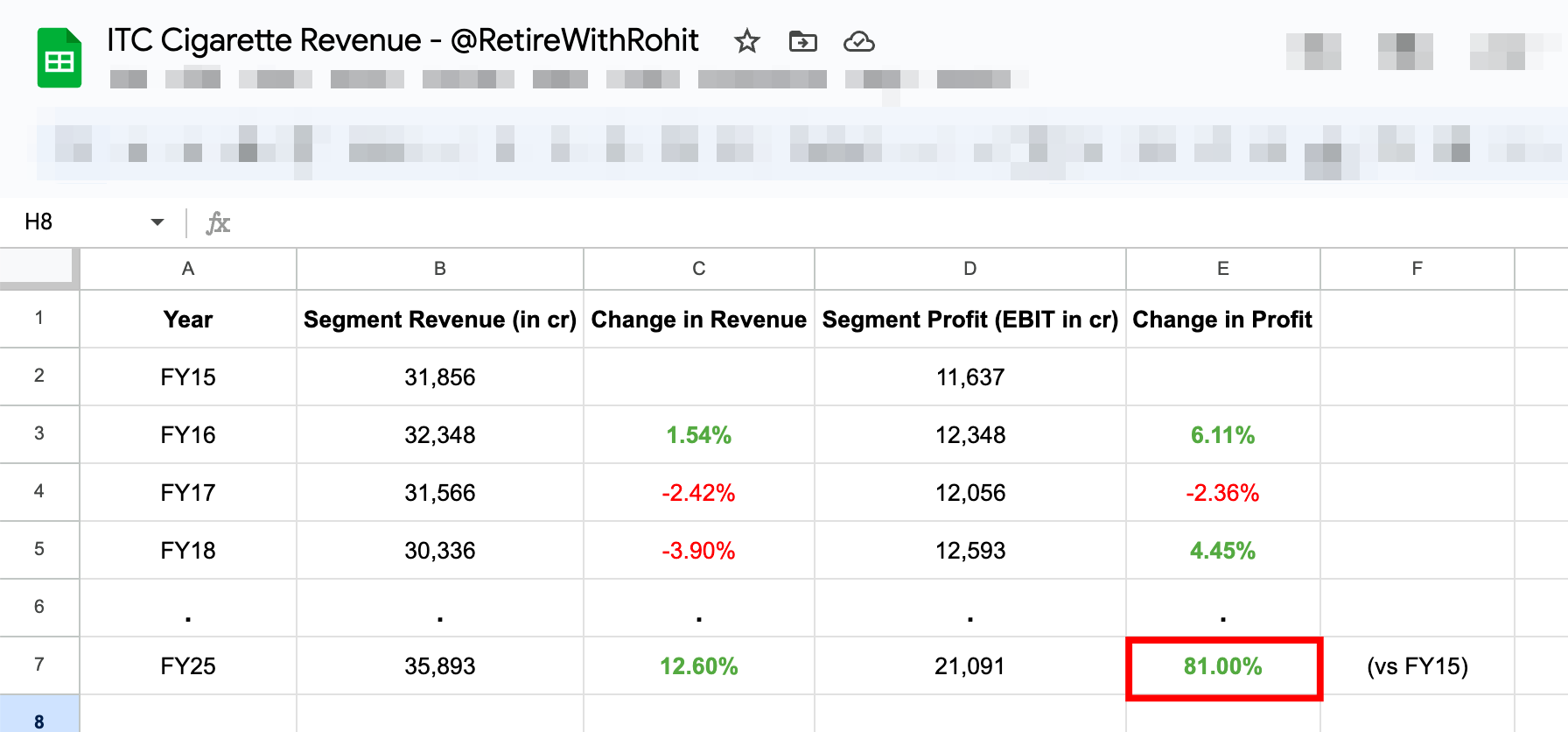

A key difference between then and now is ITC itself. In 2015, cigarettes contributed nearly 60% of ITC's total revenue. By 2025, that share had fallen to around 44%, even after the demerger of ITC Hotels.

Over the past decade, cigarette revenue grew from approximately ₹31,800 crore to ₹35,890 crore, indicating that cigarettes are no longer ITC's growth engine. Instead, they function as a high margin cash-generating business, supporting the company's expansion into other segments. Despite contributing 44% of revenue, cigarettes still account for roughly 81% of EBITDA, highlighting their role as a financial backbone rather than a growth driver.

The Role of Diversification in Reducing Risk

ITC's aggressive diversification strategy has significantly reduced its dependence on cigarettes. Its non-cigarette FMCG business has grown at a 10%+ CAGR over the last decade and now contributes around 27% of total revenue, up from 17% earlier.

While FMCG margins currently trail peers such as Nestlé and HUL, they offer considerable scope for improvement. Strategic acquisitions like 24 Mantra Organic have strengthened ITC's presence in the fast growing organic food market and added stable, recurring revenues. Other segments, such as agri and paper, provide stability even if they are not major growth drivers.

Balance Sheet Strength and Valuation Comfort

ITC's financial position provides a strong buffer against short-term disruptions. The company holds over ₹4,000 crore in cash, has negligible debt, and offers a dividend yield of more than 4%. Additionally, significant other income contributes meaningfully to net profits.

At current levels, ITC trades at a valuation last seen in 2022, suggesting that a large part of the near term risk has already been priced in by the market.

Conclusion: Panic vs Perspective

History clearly shows that cigarette tax hikes tend to cause short term panic rather than long term damage. Volumes may dip temporarily, and sentiment may turn negative, but ITC has repeatedly demonstrated its ability to absorb higher taxes and protect profitability.

What makes the current situation different is that ITC is now more diversified, financially stronger, and less dependent on cigarettes than ever before. While near term challenges remain, historical evidence suggests that the long-term impact of the tax hike may be far less severe than the market currently fears.

In investing, perspective often matters more than panic and ITC's history offers plenty of perspective.