Blinkit for Zomato: Boon or Curse?

Blinkit, Zomato's quick commerce arm, represents both a strategic boon and a significant financial challenge for its parent company. While it is a key driver of Zomato's growth and market expansion, it simultaneously puts immense pressure on its cash reserves and profit margins.

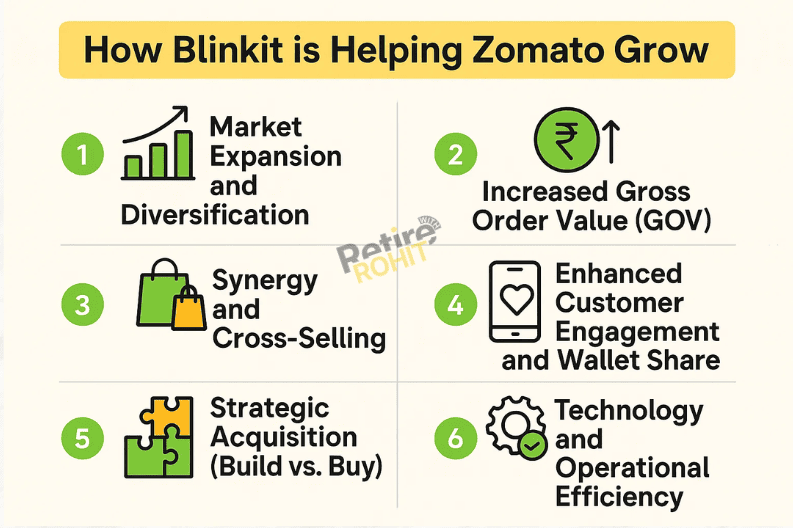

How Blinkit is Helping Zomato Grow

Image is generated through ChatGPT

Market Expansion and Diversification:

The acquisition of Blinkit allowed Zomato to expand beyond its core food delivery business and enter the rapidly growing quick commerce segment. This diversification increases Zomato's total addressable market, making it a more comprehensive lifestyle platform.

Increased Gross Order Value (GOV):

Blinkit has significantly contributed to Zomato's overall GOV. Blinkit's GOV has shown impressive growth, with some reports indicating it more than doubled, and in some key markets, it's fast catching up with Zomato's food delivery GOV.

Synergy and Cross-Selling:

While operated as separate apps, there is a clear synergy. Zomato can leverage its vast customer base for cross-selling, encouraging food delivery users to also use Blinkit for groceries and other essentials. The complementary peak delivery times between food and grocery orders also help optimize rider fleet utilization.

Enhanced Customer Engagement and Wallet Share:

Quick commerce, with its focus on "10-minute delivery," caters to spontaneous and impulse purchases, leading to higher order frequency compared to traditional food delivery. This enhances customer engagement and increases Zomato's share of the customer's overall spending.

Strategic Acquisition (Build vs. Buy):

Acquiring an established player like Blinkit (formerly Grofers) was a strategic move that saved Zomato significant time and capital that would have been required to build a similar quick commerce infrastructure, technology, and dark store network from scratch.

Technology and Operational Efficiency:

Blinkit brings a robust technology stack, an elaborate dark store network, and an in-depth understanding of supply chain networks, all of which contribute to efficient last-mile operations and improved unit economics as GOV per store increases.

Simultaneous Exhaustion of Cash Reserves and Impact on Profit Margins

Significant Cash Burn:

The quick commerce sector is highly capital-intensive. Blinkit requires substantial investments in setting up and expanding its dark store network, which involves real estate, inventory, and operational costs. Zomato has consistently infused capital into Blinkit, with significant investments including an additional INR 1,500 crore in February 2025, taking its total investment to INR 4,300 crore since the acquisition in August 2022.

Pressure on Profitability:

Increased spending on Blinkit has directly impacted Zomato's consolidated profit margins. In Q3 FY25, Zomato's profit dropped by 57% due to increased spending on Blinkit, and in Q4 FY25, its net profit saw a sharp 78% year-on-year decline, largely attributed to accelerated investments in Blinkit.

Widening Losses for Blinkit:

While Zomato aims for overall profitability, Blinkit itself continues to report significant adjusted EBITDA losses. In Q4 FY25, Blinkit's adjusted EBITDA losses increased to ₹178 crore, up from ₹103 crore in the previous quarter, as the company prioritized aggressive expansion.

Intense Competition and Discounting:

The quick commerce market is fiercely competitive, with players like Swiggy Instamart, Zepto, Flipkart Minutes, and Amazon Tez vying for market share. This leads to heavy discounting and promotional offers, further eroding profit margins, though Zomato's CEO Deepinder Goyal emphasizes Blinkit's focus on operational efficiency over deep discounting.

Rising Costs for Consumers:

To offset some losses and improve unit economics, quick commerce platforms, including Blinkit, have started introducing various charges like handling fees, delivery fees (often waived above a certain order value), small cart fees, rain fees, and surge fees. This can make quick commerce appear more expensive to consumers compared to traditional retail or even planned online grocery purchases, potentially impacting order frequency for smaller, impromptu purchases.

What is Likely to Happen Eventually?

The long-term trajectory for Blinkit and Zomato is focused on achieving profitability through scale and operational efficiency, rather than sustained heavy discounting.

Path to Profitability:

While the exact timeline is hard to commit to, Zomato expects Blinkit to "turn sharply" from loss-making to meaningfully profitable as a larger portion of its business comes from mature stores. Some analysts expect Blinkit to achieve profitability by FY2027, with the company aiming for adjusted EBITDA breakeven in less than three years from the acquisition.

Continued Expansion:

Zomato plans to aggressively expand Blinkit's dark store network, aiming for 2,000 dark stores by the end of 2026, up from around 1,007 earlier. This expansion is crucial for capturing more market share and achieving the necessary scale for profitability.

Focus on High-Margin Categories:

Blinkit is diversifying its product categories beyond traditional groceries to include electronics, beauty, pet care, and toys, which often carry higher margins, to improve overall profitability.

Operational Discipline:

Zomato's strategy for Blinkit emphasizes execution discipline and operational efficiency rather than deep discounting, aiming for sustainable growth by streamlining supply chains and delivery networks.

Potential Spin-off or Separate Listing:

There is a possibility that Blinkit could be listed separately or spun off in the future, depending on how the quick commerce market evolves.

Trends in Quick Commerce

Image generated through ChatGPT

Rapid Growth and Market Potential:

India's quick commerce market is expanding rapidly, with reports indicating a nearly 150% year-on-year growth in the first five months of 2025. It is projected to triple in size from 2024 to 2027, reaching INR 1.5-1.7 lakh crore.

Metro vs. Non-Metro Divide:

While quick commerce thrives in metros, non-metro cities lag due to lower demand, digital adoption, and entrenched local shopping habits. Scaling beyond metros requires hyper-local strategies and deeper understanding of demand and supply patterns.

Intensifying Competition:

The market remains highly competitive with established players like Blinkit, Instamart, and Zepto holding a dominant share (around 88%) and new entrants like Flipkart Minutes and Amazon Tez. This competition forces continuous innovation and investment.

Focus on Unit Economics:

Platforms are increasingly focusing on improving unit economics by raising minimum order values for free deliveries, implementing strategic discount policies, and exploring higher-value orders.

Convenience at a Cost:

While consumers value the convenience of quick delivery, they are becoming more sensitive to the various fees imposed. This is leading to behavioral shifts, with some consumers comparing prices and planning purchases more to avoid extra charges.

Employment Generation:

The quick commerce sector is a significant creator of employment opportunities, particularly for delivery personnel and micro-warehouse staff, contributing to the gig economy.

Is Quick Commerce Here to Stay and Grow?

Yes, quick commerce is here to stay and is expected to grow significantly in India.

The fundamental value proposition of instant gratification and convenience resonates strongly with urban consumers. As digital adoption increases and supply chain efficiencies improve, the market is poised for continued expansion, especially as platforms refine their strategies for tier-2 and tier-3 cities. While profitability remains a challenge in the near term, the sheer market size and consumer demand suggest a robust future for this segment.

How Much Benefit is Zomato Likely to Extract from Blinkit?

Zomato is positioned to extract substantial long-term benefits from Blinkit:

Dominance in a Growing Profit Pool:

By holding leadership positions in both food delivery and quick commerce, Zomato is uniquely positioned to dominate a growing profit pool in the broader online delivery ecosystem.

Increased Valuation:

Blinkit's valuation has seen an exponential surge, with Goldman Sachs valuing it at $13 billion by April 2024, which is notably more than Zomato's food delivery business. This surge in Blinkit's valuation has significantly contributed to Zomato's overall market capitalization and investor confidence.

Customer Lifetime Value:

Integrating Blinkit into its ecosystem helps Zomato capture a larger share of a customer's wallet and increase their lifetime value by becoming a one-stop solution for a wider range of immediate needs.

Operational Leverage:

As Blinkit's GOV per dark store increases, it achieves better operating leverage, driving down losses and moving towards profitability. This scale is crucial for long-term success.

Strategic Moat:

The extensive dark store network, efficient logistics, and established customer base built by Blinkit create a significant competitive moat, making it harder for new entrants to challenge their position.

In conclusion, while Blinkit initially puts a strain on Zomato's financials, it is a critical strategic asset that is enabling Zomato to capture a larger share of the burgeoning quick commerce market. The eventual success hinges on achieving sustainable profitability through scale, operational efficiency, and continued innovation in product categories and service models.